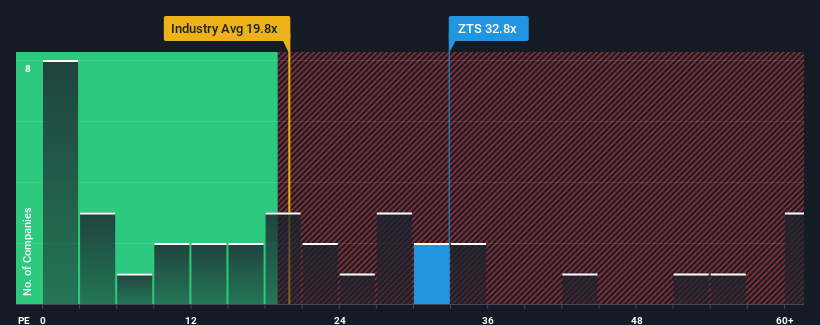

With a price-to-earnings (or "P/E") ratio of 32.8x Zoetis Inc. (NYSE:ZTS) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 19x and even P/E's lower than 11x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Zoetis as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:ZTS Price to Earnings Ratio vs Industry November 28th 2024 Keen to find out how analysts think Zoetis' future stacks up against the industry? In that case, our free report is a great place to start.

How Is Zoetis' Growth Trending?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Zoetis' to be considered reasonable.

Retrospectively, the last year delivered a decent 8.1% gain to the company's bottom line. EPS has also lifted 29% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Turning to the outlook, the next three years should generate growth of 12% per year as estimated by the analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 11% each year, which is not materially different.

In light of this, it's curious that Zoetis' P/E sits above the majority of other companies. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Zoetis' P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Zoetis currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Before you settle on your opinion, we've discovered 1 warning sign for Zoetis that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a decent 8.1% gain to the company's bottom line. EPS has also lifted 29% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Retrospectively, the last year delivered a decent 8.1% gain to the company's bottom line. EPS has also lifted 29% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

回顧過去一年,公司淨利潤增長了8.1%。每股收益也在三年前的基礎上總體提升了29%,這部分得益於過去12個月的增長。因此,可以公平地說,最近的盈利增長對於公司而言是相當可觀的。

回顧過去一年,公司淨利潤增長了8.1%。每股收益也在三年前的基礎上總體提升了29%,這部分得益於過去12個月的增長。因此,可以公平地說,最近的盈利增長對於公司而言是相當可觀的。