Do These 3 Checks Before Buying Matthews International Corporation (NASDAQ:MATW) For Its Upcoming Dividend

Do These 3 Checks Before Buying Matthews International Corporation (NASDAQ:MATW) For Its Upcoming Dividend

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends. Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Matthews International Corporation (NASDAQ:MATW) is about to go ex-dividend in just 3 days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Thus, you can purchase Matthews International's shares before the 2nd of December in order to receive the dividend, which the company will pay on the 16th of December.

一些投資者依賴分紅來增加財富,如果你是那些分紅偵探之一,你可能會對馬修國際公司(納斯達克:MATW)在短短3天后將要除息感到好奇。除息日期是在公司記錄日期的前一個工作日,記錄日期是公司確定哪些股東有權獲得分紅的日期。了解除息日期很重要,因爲股票的任何交易都需要在記錄日期之前或當天結算。因此,你可以在12月2日之前購買馬修國際的股票,以便獲得公司將在12月16日支付的分紅。

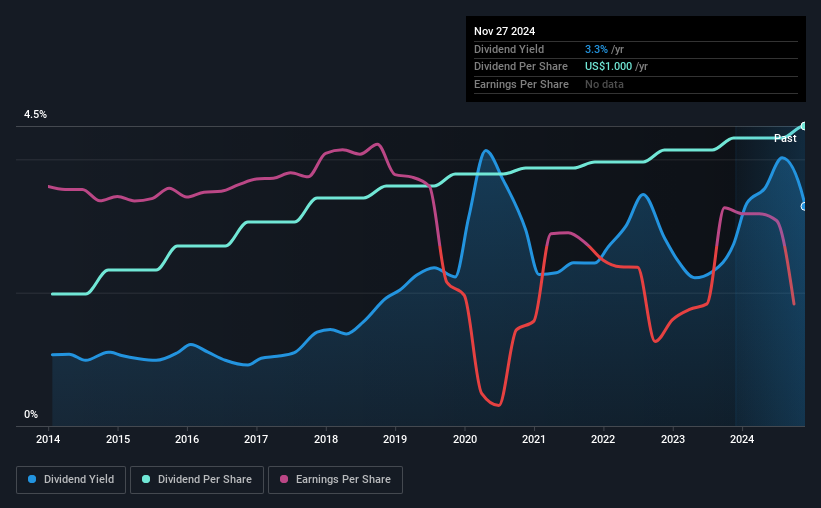

The company's upcoming dividend is US$0.25 a share, following on from the last 12 months, when the company distributed a total of US$1.00 per share to shareholders. Calculating the last year's worth of payments shows that Matthews International has a trailing yield of 3.3% on the current share price of US$30.35. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Matthews International can afford its dividend, and if the dividend could grow.

該公司即將支付的分紅爲每股0.25美元,繼過去12個月,該公司向股東分配了每股1.00美元的總額。計算去年的支付情況顯示,馬修國際目前的股價30.35美元,相對於過去12個月的分紅,具有3.3%的收益率。分紅是長揸者投資回報的重要組成部分,但前提是分紅能夠持續支付。因此,我們需要調查馬修國際是否能夠承擔其分紅,以及分紅是否能增長。

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Matthews International reported a loss after tax last year, which means it's paying a dividend despite being unprofitable. While this might be a one-off event, this is unlikely to be sustainable in the long term. With the recent loss, it's important to check if the business generated enough cash to pay its dividend. If Matthews International didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. The company paid out 92% of its free cash flow over the last year, which we think is outside the ideal range for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want to look more closely here.

如果一家公司支付的分紅超過其收入,那麼分紅可能會變得不可持續,這絕非理想的情況。馬修國際去年報告了稅後虧損,這意味着儘管處於虧損狀態,它仍在支付分紅。雖然這可能是一次性的事件,但從長期來看,這種情況不太可能持續。考慮到最近的虧損,檢查該企業是否產生了足夠的現金來支付其分紅非常重要。如果馬修國際沒有產生足夠的現金來支付分紅,那麼它必須是從銀行現金中支付或借貸,這兩者在長期內都不可持續。該公司在過去一年中支付了92%的自由現金流,我們認爲這超出了大多數企業的理想區間。現金流通常比收益更加波動,所以這可能是一個暫時的影響,但我們通常希望在這裏更仔細地觀察。

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

點擊此處查看公司的支付比率以及未來分紅的分析師預期。

Have Earnings And Dividends Been Growing?

收益和股息一直在增長嗎?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. Matthews International was unprofitable last year, but at least the general trend suggests its earnings have been improving over the past five years. Even so, an unprofitable company whose business does not quickly recover is usually not a good candidate for dividend investors.

通常,具有強勁增長前景的公司是最好的分紅派息者,因爲當每股收益改善時,增加分紅派息變得更容易。 如果收益下降到一定程度,公司可能被迫削減分紅派息。 馬修國際去年沒有盈利,但至少整體趨勢表明其收益在過去五年中有所改善。 即便如此,一個沒有盈利且業務恢復緩慢的公司通常不是分紅投資者的良好選擇。

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Matthews International has delivered 8.6% dividend growth per year on average over the past 10 years. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

許多投資者會通過評估分紅派息隨時間變化的程度來評估公司的分紅表現。 馬修國際在過去10年中平均每年實現8.6%的分紅增長。 看到公司在收益增長的同時提高分紅派息令人鼓舞,這表明公司至少有一定的興趣來回報股東。

Get our latest analysis on Matthews International's balance sheet health here.

在此獲取關於馬修國際資產負債表健康狀況的最新分析。

Final Takeaway

最後的結論

Is Matthews International worth buying for its dividend? We're a bit uncomfortable with it paying a dividend while being loss-making, especially given that the dividend was not well covered by free cash flow. It's not that we think Matthews International is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

馬修國際的分紅是否值得買入?我們對其在虧損情況下派發分紅有些不安,尤其是考慮到分紅未能很好地由自由現金流覆蓋。我們並不認爲馬修國際是一家糟糕的公司,但這些特徵通常不會導致出色的分紅表現。

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Matthews International. To help with this, we've discovered 2 warning signs for Matthews International (1 doesn't sit too well with us!) that you ought to be aware of before buying the shares.

儘管如此,如果你在看這隻股票時不太關注分紅,你仍然應該了解與馬修國際相關的風險。爲了幫助你,我們發現了馬修國際的兩個警告信號(其中一個讓我們不太安心!),在買入股票之前你應該了解這些風險。

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

一般來說,我們不建議僅僅購買第一個股息股票。下面是一個經過策劃的有趣的、股息表現良好的股票清單。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。