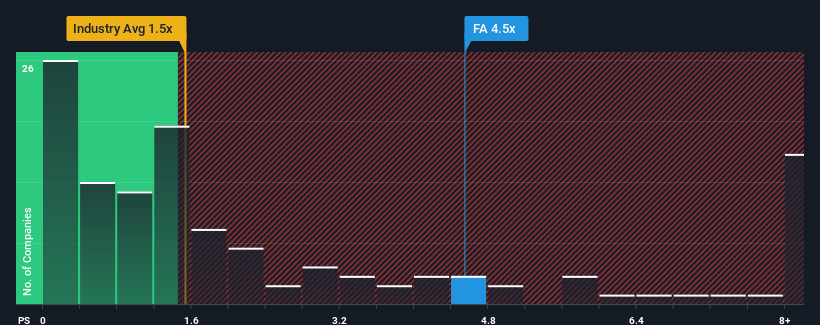

When close to half the companies in the Professional Services industry in the United States have price-to-sales ratios (or "P/S") below 1.5x, you may consider First Advantage Corporation (NASDAQ:FA) as a stock to avoid entirely with its 4.5x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

NasdaqGS:FA Price to Sales Ratio vs Industry November 26th 2024

How First Advantage Has Been Performing

While the industry has experienced revenue growth lately, First Advantage's revenue has gone into reverse gear, which is not great. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think First Advantage's future stacks up against the industry? In that case, our free report is a great place to start.

How Is First Advantage's Revenue Growth Trending?

In order to justify its P/S ratio, First Advantage would need to produce outstanding growth that's well in excess of the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 2.3%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 15% overall rise in revenue. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

Looking ahead now, revenue is anticipated to climb by 87% during the coming year according to the five analysts following the company. That's shaping up to be materially higher than the 8.3% growth forecast for the broader industry.

In light of this, it's understandable that First Advantage's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What Does First Advantage's P/S Mean For Investors?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of First Advantage's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 3 warning signs for First Advantage you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 2.3%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 15% overall rise in revenue. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 2.3%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 15% overall rise in revenue. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

回顧過去一年的財務狀況,我們看到公司的營業收入下降了2.3%。這使得最近三年的時期變得困難,儘管總體營業收入增長了15%。儘管走過了坎坷,但最近公司的營收增長基本上還是令人尊敬的。

回顧過去一年的財務狀況,我們看到公司的營業收入下降了2.3%。這使得最近三年的時期變得困難,儘管總體營業收入增長了15%。儘管走過了坎坷,但最近公司的營收增長基本上還是令人尊敬的。