Does Gorman-Rupp (NYSE:GRC) Deserve A Spot On Your Watchlist?

Does Gorman-Rupp (NYSE:GRC) Deserve A Spot On Your Watchlist?

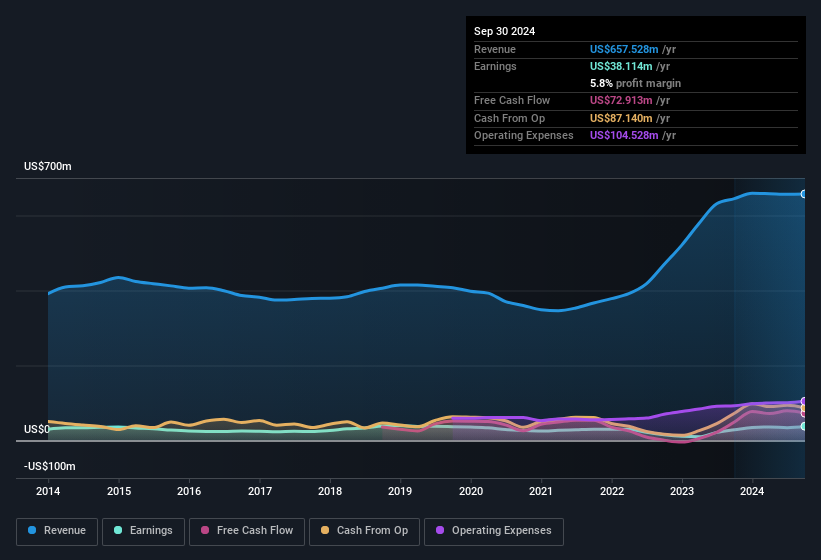

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. It was a year of stability for Gorman-Rupp as both revenue and EBIT margins remained have been flat over the past year. That's not a major concern but nor does it point to the long term growth we like to see.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. It was a year of stability for Gorman-Rupp as both revenue and EBIT margins remained have been flat over the past year. That's not a major concern but nor does it point to the long term growth we like to see. It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

許多投資者,尤其是那些缺乏經驗的投資者,會在公司具有良好故事的情況下買入股票,即使這些公司虧損。但正如彼得·林奇在《華爾街上的贏家》一書中所說,「長期賭博幾乎從來沒有成功過」。雖然一家資金充裕的公司可能會連續數年虧損,但最終它還是需要賺錢,否則投資者將會離開,公司也會逐漸消亡。

In contrast to all that, many investors prefer to focus on companies like Gorman-Rupp (NYSE:GRC), which has not only revenues, but also profits. Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

與所有這些相比,許多投資者更傾向於關注像gorman-rupp(紐交所:GRC)這樣的公司,該公司不僅有營業收入,還有利潤。現在這並不是說該公司提供了最佳的投資機會,但盈利能力是業務成功的關鍵組成部分。

How Fast Is Gorman-Rupp Growing?

gorman-rupp的增長速度有多快?

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. We can see that in the last three years Gorman-Rupp grew its EPS by 8.0% per year. That's a pretty good rate, if the company can sustain it.

如果你相信市場即使有一點效率,那麼從長遠來看,你會期望一個公司的股價跟隨其每股收益(每股收益)的結果。因此,有很多投資者喜歡買入那些每股收益增長的公司的股票。我們可以看到,在過去三年中,gorman-rupp每年的每股收益增長了8.0%。如果公司能夠保持這一增長速度,那是一個相當不錯的比例。

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. It was a year of stability for Gorman-Rupp as both revenue and EBIT margins remained have been flat over the past year. That's not a major concern but nor does it point to the long term growth we like to see.

核實一個公司增長的一個方法是查看其營業收入和利息及稅前利潤(EBIT)利潤率的變化。對gorman-rupp來說,這是一個穩定的一年,因爲過去一年營業收入和EBIT利潤率都保持平穩。這並不是一個主要的擔憂,但它也沒有指向我們希望看到的長期增長。

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

在下面的圖表中,您可以看到公司的盈利和營業收入隨時間的增長情況。要查看實際數字,請單擊圖表。

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Gorman-Rupp's forecast profits?

投資與生活一樣,未來比過去更重要。那麼爲什麼不查看一下gorman-rupp預測利潤的這個免費的互動可視化呢?

Are Gorman-Rupp Insiders Aligned With All Shareholders?

gorman-rupp內部人員與所有股東的利益是否一致?

It's a necessity that company leaders act in the best interest of shareholders and so insider investment always comes as a reassurance to the market. So it is good to see that Gorman-Rupp insiders have a significant amount of capital invested in the stock. We note that their impressive stake in the company is worth US$235m. Coming in at 21% of the business, that holding gives insiders a lot of influence, and plenty of reason to generate value for shareholders. So there is opportunity here to invest in a company whose management have tangible incentives to deliver.

公司領導以股東的最佳利益行事是必要的,因此內部投資始終給市場帶來信心。因此,看到gorman-rupp內部人員在股票上投資了大量資金是件好事。我們注意到他們在公司的可觀股份價值達23500萬美元。佔業務的21%,這個持股給予內部人員很大的影響力,以及爲股東創造價值的充分理由。所以這裏有機會投資於一家管理層有實際動力去實現的公司。

It means a lot to see insiders invested in the business, but shareholders may be wondering if remuneration policies are in their best interest. A brief analysis of the CEO compensation suggests they are. Our analysis has discovered that the median total compensation for the CEOs of companies like Gorman-Rupp with market caps between US$400m and US$1.6b is about US$3.2m.

看到內部人員在業務上投資意義重大,但股東可能會想知道薪酬政策是否符合他們的最佳利益。對CEO薪酬的簡要分析表明它們是合理的。我們的分析發現,市場資本在40000萬到16億之間的公司如gorman-rupp的CEO的中位數總薪酬約爲320萬美元。

Gorman-Rupp's CEO took home a total compensation package worth US$1.7m in the year leading up to December 2023. That seems pretty reasonable, especially given it's below the median for similar sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

gorman-rupp的CEO在2023年12月前一年獲得了總價值170萬美元的薪酬包。這看起來相當合理,特別是考慮到這一數字低於類似規模公司的中位數。CEO薪酬並不是考慮公司時最重要的方面,但當其合理時,給予了一點信心,顯示領導層關心股東利益。一般來說,可以認爲合理的薪酬水平證明了良好的決策。

Does Gorman-Rupp Deserve A Spot On Your Watchlist?

Gorman-Rupp值得在你的自選中佔有一席之地嗎?

One positive for Gorman-Rupp is that it is growing EPS. That's nice to see. The growth of EPS may be the eye-catching headline for Gorman-Rupp, but there's more to bring joy for shareholders. With a meaningful level of insider ownership, and reasonable CEO pay, a reasonable mind might conclude that this is one stock worth watching. Even so, be aware that Gorman-Rupp is showing 1 warning sign in our investment analysis , you should know about...

Gorman-Rupp的一個積極因素是其每股收益正在增長。這很好。每股收益的增長可能是Gorman-Rupp引人注目的頭條,但還有更多因素讓股東感到愉悅。考慮到內部持股比例適中,以及CEO薪酬合理,一個理智的人可能會得出結論,這是一隻值得關注的股票。即便如此,請注意,Gorman-Rupp在我們的投資分析中顯示出1個警告信號,你應該了解...

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in the US with promising growth potential and insider confidence.

儘管不增長收益且沒有內部人士購買的股票可能會有回報,但對於重視這些關鍵指標的投資者來說,以下是在美國具有潛在增長和內部人士信心的經過慎重篩選的公司列表。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文討論的內部交易是指在相關司法管轄區中報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。