DocuSign (NASDAQ:DOCU) Is Experiencing Growth In Returns On Capital

DocuSign (NASDAQ:DOCU) Is Experiencing Growth In Returns On Capital

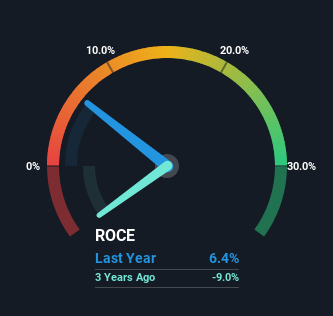

0.064 = US$137m ÷ (US$3.8b - US$1.6b)

0.064 = US$137m ÷ (US$3.8b - US$1.6b) If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in DocuSign's (NASDAQ:DOCU) returns on capital, so let's have a look.

如果我们想要找到一个能够长期增值的股票,我们应该关注哪些潜在趋势呢?首先,我们希望看到资本使用回报率(ROCE)在增加,其次是不断扩大的资本使用基础。这向我们表明它是一个复合机器,能够持续地将其收益重新投资到业务中,并产生更高的回报。说到这一点,我们注意到DocuSign(纳斯达克: docusign)的资本回报率有了一些很大的变化,让我们来看看。

What Is Return On Capital Employed (ROCE)?

我们对 Enphase Energy 的资本雇用回报率的看法:正如我们上面看到的,Enphase Energy 的资本回报率没有提高,但它正在重新投资于业务。投资者必须认为未来会有更好的前景,因为股票表现良好,使持股五年以上的股东获得了 690% 的收益。最终,如果基本趋势持续存在,我们不会对它成为一只多头股持有期很久很有信心。

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on DocuSign is:

对于那些不确定ROCE是什么的人,它衡量了公司可以从业务中使用的资本产生多少税前利润。DocuSign的这个计算公式是:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

资本利用率 = 利息和税前利润(EBIT) ÷ (总资产 - 流动负债)

0.064 = US$137m ÷ (US$3.8b - US$1.6b) (Based on the trailing twelve months to July 2024).

0.064 = 13700万美元 ÷ (38亿美元 - 16亿美元)(基于2024年7月至2024年7月的过去十二个月)。

So, DocuSign has an ROCE of 6.4%. Ultimately, that's a low return and it under-performs the Software industry average of 9.1%.

因此,DocuSign的ROCE为6.4%。最终,这是一个较低的回报,低于软件行业平均水平9.1%。

In the above chart we have measured DocuSign's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for DocuSign .

在上面的图表中,我们衡量了docusign之前的资本回报率与其之前的业绩,但未来可能更为重要。如果您感兴趣,可以查看分析师对docusign的预测,详情请参阅我们的免费docusign分析师报告。

So How Is DocuSign's ROCE Trending?

那么docusign的资本回报率趋势如何?

The fact that DocuSign is now generating some pre-tax profits from its prior investments is very encouraging. About five years ago the company was generating losses but things have turned around because it's now earning 6.4% on its capital. And unsurprisingly, like most companies trying to break into the black, DocuSign is utilizing 81% more capital than it was five years ago. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

事实上,docusign现在从先前的投资中获得一些税前利润是非常令人鼓舞的。大约五年前,这家公司还在亏损,但情况已经好转,因为现在资本回报率已经达到6.4%。并且并不奇怪,像大多数试图扭亏为盈的公司一样,docusign现在比五年前多利用了81%的资本。这可以告诉我们公司有很多能够产生更高回报率的再投资机会。

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Effectively this means that suppliers or short-term creditors are now funding 43% of the business, which is more than it was five years ago. And with current liabilities at those levels, that's pretty high.

值得一提的是,公司目前负债有明显增加,因此我们将部分资本回报率增长归因于此。实际上,这意味着供应商或短期债权人现在资助了公司43%的业务,这比五年前高了许多。而且目前的负债水平已经相当高。

The Key Takeaway

重要提示

To the delight of most shareholders, DocuSign has now broken into profitability. Since the stock has only returned 19% to shareholders over the last five years, the promising fundamentals may not be recognized yet by investors. So with that in mind, we think the stock deserves further research.

令大多数股东高兴的是,docusign现在已经实现盈利。由于股票在过去五年中仅为股东带来了19%的回报,这些有前途的基本面可能尚未被投资者认可。基于这一点,我们认为这支股票值得进一步研究。

If you want to continue researching DocuSign, you might be interested to know about the 1 warning sign that our analysis has discovered.

如果您想继续研究docusign,您可能会对我们分析发现的一个警告标志感兴趣。

While DocuSign isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

虽然docusign没有获得最高回报,请查看这个免费的公司列表,这些公司在资产负债表上获得高回报,并且拥有坚实的资产。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。