Does Berkshire Hathaway (NYSE:BRK.A) Deserve A Spot On Your Watchlist?

Does Berkshire Hathaway (NYSE:BRK.A) Deserve A Spot On Your Watchlist?

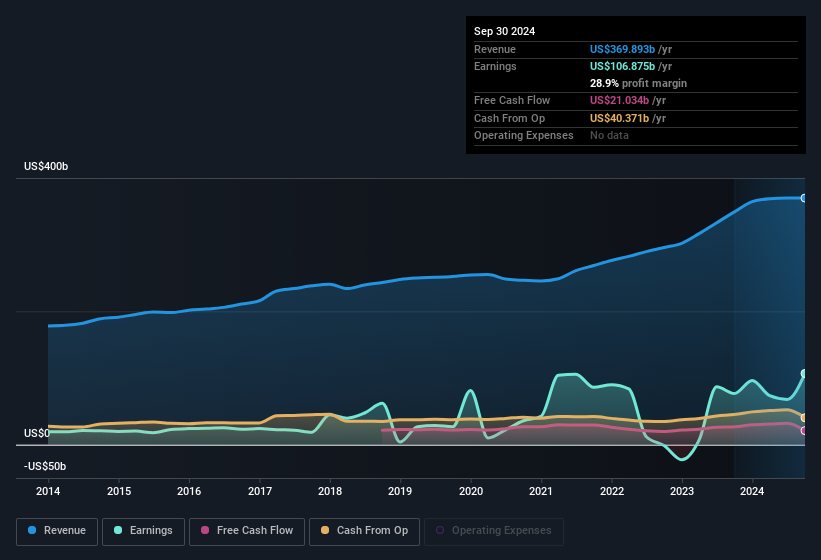

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Our analysis has highlighted that Berkshire Hathaway's revenue

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Our analysis has highlighted that Berkshire Hathaway's revenue It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

许多投资者,尤其是那些缺乏经验的投资者,通常会购买那些讲述精彩故事的公司股票,即使这些公司是亏损的。不幸的是,这些高风险投资往往很少有可能从中获益,许多投资者会为此付出代价。亏损的公司始终在争分夺秒地追求财务可持续性,因此投资这些公司的投资者可能承担了比他们应承担的风险更大的风险。

In contrast to all that, many investors prefer to focus on companies like Berkshire Hathaway (NYSE:BRK.A), which has not only revenues, but also profits. While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

与所有板块相比,许多投资者更愿意关注像伯克希尔哈撒韦(纽交所:BRk.A)这样的公司,该公司不仅有营业收入,还有利润。虽然这并不一定表明它被低估,但该业务的盈利能力足以令人欣赏——尤其是在其不断增长的情况下。

How Quickly Is Berkshire Hathaway Increasing Earnings Per Share?

伯克希尔哈撒韦的每股收益增长速度有多快?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That makes EPS growth an attractive quality for any company. Berkshire Hathaway managed to grow EPS by 9.7% per year, over three years. That's a pretty good rate, if the company can sustain it.

如果一家公司能保持每股收益(EPS)足够长时间的增长,其股价最终应该会跟随上升。这使得EPS增长成为任何公司的吸引力特质。伯克希尔哈撒韦在三年内成功地将EPS增长了9.7%。如果公司能够维持这个增长率,那就是一个相当不错的水平。

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Our analysis has highlighted that Berkshire Hathaway's revenue from operations did not account for all of their revenue in the previous 12 months, so our analysis of its margins might not accurately reflect the underlying business. The music to the ears of Berkshire Hathaway shareholders is that EBIT margins have grown from 28% to 37% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

仔细考虑营业收入的增长和息税前利润(EBIT)利润率可以帮助我们了解近期利润增长的可持续性。我们的分析显示,伯克希尔哈撒韦过去12个月的运营收入并未占其所有收入,因此我们对其利润率的分析可能无法准确反映其基本业务。伯克希尔哈撒韦股东耳边的美好消息是,过去12个月EBIT利润率从28%增长到37%,营业收入也呈上升趋势。这两个指标都是潜在增长的良好衡量标准。

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

你可以在下面的图表中查看公司的营收和盈利增长趋势。如需了解更详细信息,请单击图像。

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Berkshire Hathaway?

虽然我们生活在当下,但毫无疑问未来在投资决策过程中最为重要。那么为何不查看这个互动图表,描绘出伯克希尔哈撒韦的未来每股收益预估呢?

Are Berkshire Hathaway Insiders Aligned With All Shareholders?

伯克希尔哈撒韦的内部人士是否与所有股东的利益一致?

Since Berkshire Hathaway has a market capitalisation of US$1.0t, we wouldn't expect insiders to hold a large percentage of shares. But we are reassured by the fact they have invested in the company. We note that their impressive stake in the company is worth US$152b. Coming in at 15% of the business, that holding gives insiders a lot of influence, and plenty of reason to generate value for shareholders. So there is opportunity here to invest in a company whose management have tangible incentives to deliver.

由于伯克希尔哈撒韦的市值为1万亿美元,我们不期望内部人士持有大量股份。但是,我们对他们投资于公司的事实感到放心。我们注意到,他们在公司的可观持股价值达1520亿美元。这占到业务的15%,这一持股让内部人士有很大的影响力,也有很多理由为股东创造价值。因此,这里有机会投资于这样一家公司,其管理层有切实的激励来实现业绩。

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. Well, based on the CEO pay, you'd argue that they are indeed. Our analysis has discovered that the median total compensation for the CEOs of companies like Berkshire Hathaway, with market caps over US$8.0b, is about US$13m.

虽然看到内部人士通过大量投资对公司的强烈信念总是好事,但股东也必须询问管理层的薪酬政策是否合理。根据CEO的薪酬,你可能会认为它们确实合理。我们的分析发现,市值超过80亿美元的公司,例如伯克希尔哈撒韦,CEO的中位数总薪酬约为1300万美元。

The Berkshire Hathaway CEO received total compensation of just US$414k in the year to December 2023. First impressions seem to indicate a compensation policy that is favourable to shareholders. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

伯克希尔哈撒韦的CEO在截至2023年12月的一年里,获得的总薪酬仅为41.4万美元。初步印象表明,这一薪酬政策对股东是有利的。CEO薪酬水平不是投资者最重要的指标,但当薪酬适中时,这确实支持了CEO与普通股东之间的更好一致性。一般来说,可以认为合理的薪酬水平证明了良好的决策能力。

Does Berkshire Hathaway Deserve A Spot On Your Watchlist?

伯克希尔哈撒韦值得在你的自选中占有一席之地吗?

One positive for Berkshire Hathaway is that it is growing EPS. That's nice to see. The fact that EPS is growing is a genuine positive for Berkshire Hathaway, but the pleasant picture gets better than that. Boasting both modest CEO pay and considerable insider ownership, you'd argue this one is worthy of the watchlist, at least. It's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Berkshire Hathaway (at least 1 which shouldn't be ignored) , and understanding these should be part of your investment process.

伯克希尔哈撒韦的一个积极因素是每股收益正在增长。这是非常令人欣慰的。每股收益的增长对伯克希尔哈撒韦来说是一个真正的积极因素,但令人愉快的局面还不止于此。拥有适度的CEO薪酬和可观的内部持股,你可以说这个值得至少列入自选中。仍然有必要考虑投资风险这一始终存在的阴影。我们指出了伯克希尔哈撒韦的2个警示信号(至少有1个不应被忽视),理解这些信号应该是你投资过程的一部分。

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a tailored list of companies which have demonstrated growth backed by significant insider holdings.

总是有可能买入未增长收益并且内部人员不买入股票的股票表现良好。但是对于那些认为这些重要指数的人,我们鼓励您查看具有这些功能的公司。您可以访问定制列表,其中列出了已经展示出增长并得到内幕人员认可的公司。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

请注意,本文讨论的内部交易是指在相关司法管辖区中报告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。