To the annoyance of some shareholders, ImmunoPrecise Antibodies Ltd. (NASDAQ:IPA) shares are down a considerable 30% in the last month, which continues a horrid run for the company. For any long-term shareholders, the last month ends a year to forget by locking in a 71% share price decline.

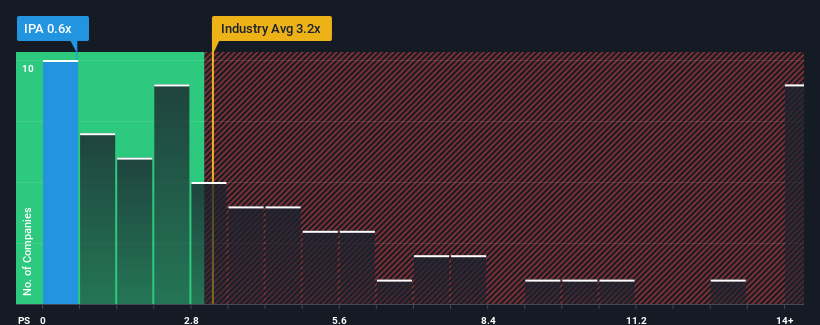

Following the heavy fall in price, ImmunoPrecise Antibodies' price-to-sales (or "P/S") ratio of 0.6x might make it look like a strong buy right now compared to the wider Life Sciences industry in the United States, where around half of the companies have P/S ratios above 3.2x and even P/S above 6x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

NasdaqGM:IPA Price to Sales Ratio vs Industry November 23rd 2024

What Does ImmunoPrecise Antibodies' Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, ImmunoPrecise Antibodies has been doing relatively well. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on ImmunoPrecise Antibodies will help you uncover what's on the horizon.

How Is ImmunoPrecise Antibodies' Revenue Growth Trending?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like ImmunoPrecise Antibodies' to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 11% last year. The latest three year period has also seen a 29% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 22% per year during the coming three years according to the dual analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 7.1% each year, which is noticeably less attractive.

In light of this, it's peculiar that ImmunoPrecise Antibodies' P/S sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Key Takeaway

Having almost fallen off a cliff, ImmunoPrecise Antibodies' share price has pulled its P/S way down as well. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

A look at ImmunoPrecise Antibodies' revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. The reason for this depressed P/S could potentially be found in the risks the market is pricing in. It appears the market could be anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for ImmunoPrecise Antibodies (1 is potentially serious) you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should far underperform the industry for P/S ratios like ImmunoPrecise Antibodies' to be considered reasonable.

There's an inherent assumption that a company should far underperform the industry for P/S ratios like ImmunoPrecise Antibodies' to be considered reasonable.

一種固有的假設是,像免疫精密抗體這樣的市銷率遠低於行業的公司才被認爲是合理的。

一種固有的假設是,像免疫精密抗體這樣的市銷率遠低於行業的公司才被認爲是合理的。