Despite an already strong run, Climb Global Solutions, Inc. (NASDAQ:CLMB) shares have been powering on, with a gain of 29% in the last thirty days. The annual gain comes to 190% following the latest surge, making investors sit up and take notice.

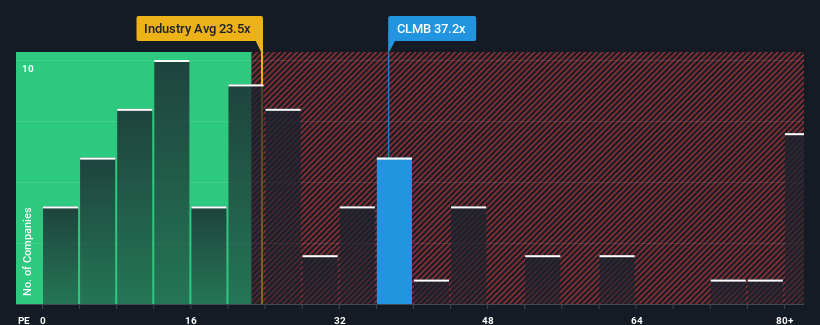

Since its price has surged higher, Climb Global Solutions' price-to-earnings (or "P/E") ratio of 37.2x might make it look like a strong sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 19x and even P/E's below 11x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Climb Global Solutions certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

NasdaqGM:CLMB Price to Earnings Ratio vs Industry November 22nd 2024 Want the full picture on analyst estimates for the company? Then our free report on Climb Global Solutions will help you uncover what's on the horizon.

How Is Climb Global Solutions' Growth Trending?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Climb Global Solutions' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 40% gain to the company's bottom line. Pleasingly, EPS has also lifted 94% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 9.8% during the coming year according to the sole analyst following the company. Meanwhile, the rest of the market is forecast to expand by 15%, which is noticeably more attractive.

With this information, we find it concerning that Climb Global Solutions is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Shares in Climb Global Solutions have built up some good momentum lately, which has really inflated its P/E. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Climb Global Solutions' analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Climb Global Solutions with six simple checks on some of these key factors.

You might be able to find a better investment than Climb Global Solutions. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

儘管已經有強勁的運行,Climb Global Solutions, Inc. (納斯達克:CLMB)的股票仍在繼續上升,在過去三十天內上漲了29%。最新的漲幅使年度收益達到了190%,引起了投資者的注意。

由於其價格已經飆升,Climb Global Solutions的市盈率(或稱爲"P/E")爲37.2倍,相較於美國市場,可能看起來是一個強烈的賣出信號,而在美國,約一半的公司市盈率低於19倍,甚至市盈率低於11倍的案例也相當普遍。然而,市盈率較高可能是有原因的,是否合理還需要進一步調查來判斷。

Climb Global Solutions最近確實表現出色,盈利增長超過了其他大多數公司。市盈率可能較高是因爲投資者認爲這種強勁的盈利表現將會持續。如果沒有,那麼現有股東可能會對股價的可持續性感到有些緊張。

納斯達克GM:CLMB 市盈率與行業比較 2024年11月22日 想要了解分析師對該公司的估計的完整信息嗎?那麼我們的Climb Global Solutions免費報告將幫助您發現未來的趨勢。

Climb Global Solutions的增長趨勢如何?

存在一種固有假設,即公司應大幅超越市場,才能使像Climb Global Solutions這樣的市盈率被認爲是合理的。

There's an inherent assumption that a company should far outperform the market for P/E ratios like Climb Global Solutions' to be considered reasonable.

There's an inherent assumption that a company should far outperform the market for P/E ratios like Climb Global Solutions' to be considered reasonable.

存在一種固有假設,即公司應大幅超越市場,才能使像Climb Global Solutions這樣的市盈率被認爲是合理的。

存在一種固有假設,即公司應大幅超越市場,才能使像Climb Global Solutions這樣的市盈率被認爲是合理的。