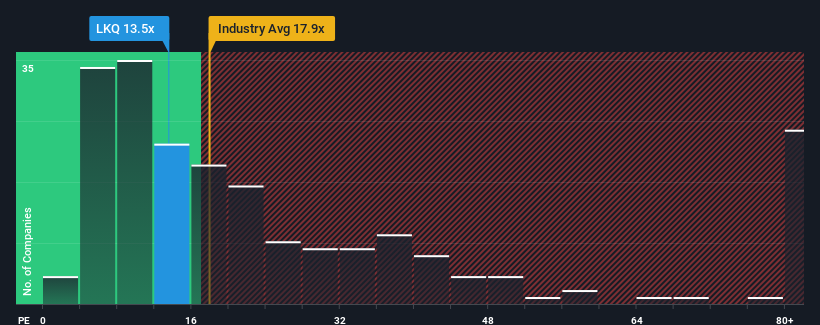

LKQ Corporation's (NASDAQ:LKQ) price-to-earnings (or "P/E") ratio of 13.5x might make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 19x and even P/E's above 35x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

LKQ hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

NasdaqGS:LKQ Price to Earnings Ratio vs Industry November 21st 2024 Keen to find out how analysts think LKQ's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Growth For LKQ?

LKQ's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Retrospectively, the last year delivered a frustrating 24% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 20% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 16% as estimated by the ten analysts watching the company. With the market predicted to deliver 15% growth , the company is positioned for a comparable earnings result.

With this information, we find it odd that LKQ is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Bottom Line On LKQ's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of LKQ's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

You should always think about risks. Case in point, we've spotted 2 warning signs for LKQ you should be aware of.

If you're unsure about the strength of LKQ's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 24% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 20% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Retrospectively, the last year delivered a frustrating 24% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 20% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

回顾过去一年,该公司的底线降低了令人沮丧的24%。 这意味着过去三年的每股收益总体下降了20%,长期来看也有收益下滑。 因此,可以说公司最近的盈利增长令人不满。

回顾过去一年,该公司的底线降低了令人沮丧的24%。 这意味着过去三年的每股收益总体下降了20%,长期来看也有收益下滑。 因此,可以说公司最近的盈利增长令人不满。