Here's Why We Think Itron (NASDAQ:ITRI) Might Deserve Your Attention Today

Here's Why We Think Itron (NASDAQ:ITRI) Might Deserve Your Attention Today

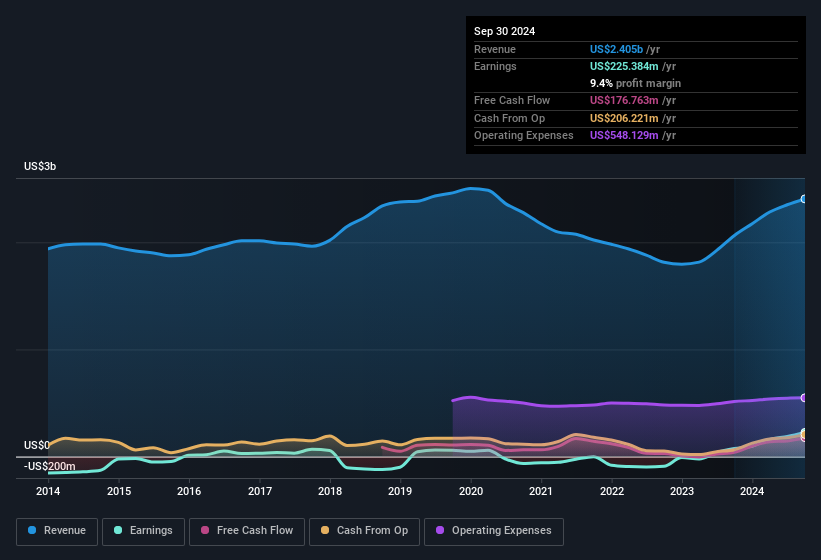

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Itron shareholders can take confidence from the fact that EBIT margins are up from 6.0% to 11%, and revenue is growing. That's great to see, on both counts.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Itron shareholders can take confidence from the fact that EBIT margins are up from 6.0% to 11%, and revenue is growing. That's great to see, on both counts. The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

公司能够扭转命运的投资的激动人心,是某些投机者的一个重要诱因,因此即使是那些没有营收、没有利润和当季表现不佳的公司也能够找到投资者。但现实情况是,当一个公司连续多年亏损,其投资者通常会承担他们的这些亏损。亏损公司总是在时间的竞赛中争取金融可持续性,因此这些公司的投资者可能承担了比他们应该承担的更多风险。

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Itron (NASDAQ:ITRI). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Itron with the means to add long-term value to shareholders.

尽管处于科技股蓝天投资的时代,许多投资者仍然采用更传统的策略;购买像伊管(纳斯达克:ITRI)这样的盈利公司的股票。即使该公司在市场上被公认为合理估值,投资者仍然会同意,稳定的盈利能够持续为伊管提供为股东增加长期价值的手段。

How Fast Is Itron Growing Its Earnings Per Share?

伊管的每股收益增长速度有多快?

Strong earnings per share (EPS) results are an indicator of a company achieving solid profits, which investors look upon favourably and so the share price tends to reflect great EPS performance. Which is why EPS growth is looked upon so favourably. Commendations have to be given in seeing that Itron grew its EPS from US$1.65 to US$5.00, in one short year. Even though that growth rate may not be repeated, that looks like a breakout improvement. Could this be a sign that the business has reached an inflection point?

强劲的每股收益(EPS)结果是公司实现稳固利润的指标,投资者对此持积极态度,因此股价往往反映出优秀的EPS表现。这就是为什么EPS增长被如此看重。值得称赞的是,伊管在短短一年内将其每股收益从1.65美元增长至5.00美元。尽管这种增长率可能不会再现,但这看起来是一次突破性改善。这是否意味着业务已经达到拐点?

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Itron shareholders can take confidence from the fact that EBIT margins are up from 6.0% to 11%, and revenue is growing. That's great to see, on both counts.

查看息税前利润(EBIT)利润率和营业收入增长通常是有帮助的,以便进一步了解公司的增长质量。伊管的股东可以放心,因为EBIT利润率从6.0%上升到11%,营业收入也在增长。这两方面的表现都很不错。

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

下面的图表显示了公司的营业收入和收益是如何随时间变化的。要查看实际数字,请单击图表。

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. While crystal balls don't exist, you can check our visualization of consensus analyst forecasts for Itron's future EPS 100% free.

作为投资者,关键在于找到未来将表现良好的公司,而不仅仅是过去。尽管水晶球并不存在,但您可以查看我们对伊管未来每股收益的共识分析师预测的可视化,100%免费。

Are Itron Insiders Aligned With All Shareholders?

伊管内部人是否与所有股东保持一致?

Since Itron has a market capitalisation of US$5.2b, we wouldn't expect insiders to hold a large percentage of shares. But we do take comfort from the fact that they are investors in the company. Given insiders own a significant chunk of shares, currently valued at US$61m, they have plenty of motivation to push the business to succeed. That's certainly enough to let shareholders know that management will be very focussed on long term growth.

由于伊管的市场资本为52亿美金,我们并不期望内部人持有大量股份。但我们确实从他们是公司的投资者这一事实中得到安慰。考虑到内部人拥有一大部分股份,目前估值为6100万美元,他们有足够的动力推动业务成功。这肯定足以让股东知道管理层将非常关注长期增长。

It's good to see that insiders are invested in the company, but are remuneration levels reasonable? Our quick analysis into CEO remuneration would seem to indicate they are. For companies with market capitalisations between US$4.0b and US$12b, like Itron, the median CEO pay is around US$8.0m.

看到内部人投资于公司是好事,但薪酬水平合理吗?我们对CEO薪酬的快速分析似乎表明是合理的。对于市场资本在40亿到120亿美金之间的公司,如伊管,CEO的中位数薪酬约为800万美元。

Itron offered total compensation worth US$6.2m to its CEO in the year to December 2023. That is actually below the median for CEO's of similarly sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of a culture of integrity, in a broader sense.

伊管在截至2023年12月的一年中向其CEO提供了620万美元的总补偿。这实际上低于同等规模公司的CEO薪酬中位数。CEO薪酬水平并不是投资者最重要的指标,但当薪酬适中时,这确实支持了CEO与普通股东之间的更好对齐。这在更广泛的意义上也可能是诚信文化的标志。

Is Itron Worth Keeping An Eye On?

伊管值得关注吗?

Itron's earnings per share have been soaring, with growth rates sky high. The sweetener is that insiders have a mountain of stock, and the CEO remuneration is quite reasonable. The sharp increase in earnings could signal good business momentum. Itron is certainly doing some things right and is well worth investigating. If you think Itron might suit your style as an investor, you could go straight to its annual report, or you could first check our discounted cash flow (DCF) valuation for the company.

伊管的每股收益一直在飙升,增长率非常高。 令人欣慰的是,内部人士持有大量股票,而CEO的薪酬相当合理。 收益的急剧增长可能预示着良好的业务势头。 伊管显然做对了一些事情,值得深入调查。 如果你认为伊管适合你的投资风格,可以直接查看它的年度报告,或者先查看我们对该公司的折现现金流(DCF)估值。

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a tailored list of companies which have demonstrated growth backed by significant insider holdings.

总是有可能买入未增长收益并且内部人员不买入股票的股票表现良好。但是对于那些认为这些重要指数的人,我们鼓励您查看具有这些功能的公司。您可以访问定制列表,其中列出了已经展示出增长并得到内幕人员认可的公司。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

请注意,本文讨论的内部交易是指在相关司法管辖区中报告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。