Despite an already strong run, TSS, Inc. (NASDAQ:TSSI) shares have been powering on, with a gain of 51% in the last thirty days. The last 30 days were the cherry on top of the stock's 2,224% gain in the last year, which is nothing short of spectacular.

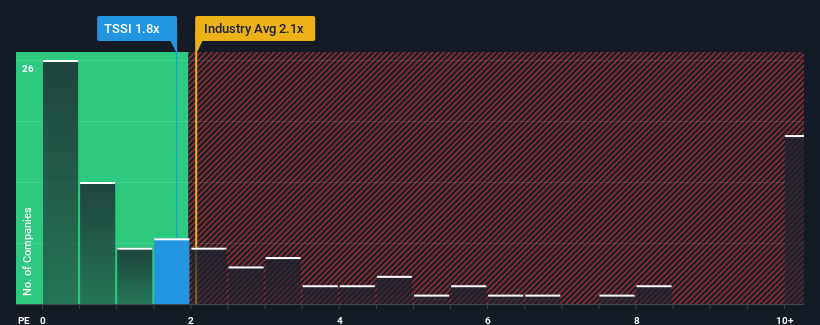

Even after such a large jump in price, you could still be forgiven for feeling indifferent about TSS' P/S ratio of 1.8x, since the median price-to-sales (or "P/S") ratio for the IT industry in the United States is also close to 2.1x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

NasdaqCM:TSSI Price to Sales Ratio vs Industry November 18th 2024

How Has TSS Performed Recently?

TSS certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on TSS will help you shine a light on its historical performance.

How Is TSS' Revenue Growth Trending?

TSS' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered an exceptional 199% gain to the company's top line. This great performance means it was also able to deliver immense revenue growth over the last three years. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 11%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we find it interesting that TSS is trading at a fairly similar P/S compared to the industry. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

TSS' stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that TSS currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with TSS, and understanding these should be part of your investment process.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

TSS' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

TSS' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

TSS的市銷率對於一家預計只能提供適度增長並且重要的與行業表現一致的公司來說會是典型的。

TSS的市銷率對於一家預計只能提供適度增長並且重要的與行業表現一致的公司來說會是典型的。