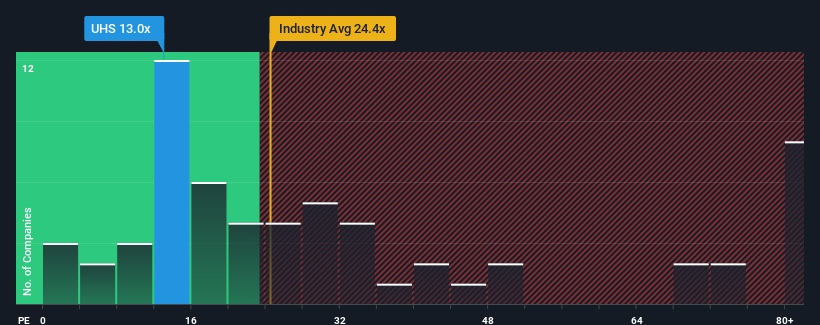

With a price-to-earnings (or "P/E") ratio of 13x Universal Health Services, Inc. (NYSE:UHS) may be sending bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 19x and even P/E's higher than 35x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Universal Health Services certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

NYSE:UHS Price to Earnings Ratio vs Industry November 17th 2024 Want the full picture on analyst estimates for the company? Then our free report on Universal Health Services will help you uncover what's on the horizon.

How Is Universal Health Services' Growth Trending?

Universal Health Services' P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 59% last year. As a result, it also grew EPS by 23% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 14% as estimated by the analysts watching the company. With the market predicted to deliver 15% growth , the company is positioned for a comparable earnings result.

With this information, we find it odd that Universal Health Services is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Universal Health Services currently trades on a lower than expected P/E since its forecast growth is in line with the wider market. When we see an average earnings outlook with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

Having said that, be aware Universal Health Services is showing 1 warning sign in our investment analysis, you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

以13倍的市盈率(或「P/E」)來看,universal health services (NYSE:UHS) 目前可能正在發出積極信號,因爲在美國,將近一半的公司市盈率大於19倍,即使市盈率高於35倍也並不飛凡。儘管如此,我們需要深入挖掘,以確定降低市盈率的合理依據。

universal health services 最近的表現確實不錯,因爲其盈利增長超過大多數其他公司。許多人可能預期盈利表現將大幅下降,這導致市盈率受壓。如果你喜歡這家公司,你可能希望情況不是這樣,這樣你就有機會在市場不看好時買入一些股票。

NYSE:UHS 市盈率與行業板塊 2024年11月17日 想要獲取有關該公司分析師預測的全面信息嗎?那麼我們的免費報告關於universal health services 將幫助您揭示未來的走勢。

universal health services的增長趨勢如何?

universal health services的市盈率對於一個只預期實現有限增長且重要的是表現比市場差的公司來說是典型的。

Taking a look back first, we see that the company grew earnings per share by an impressive 59% last year. As a result, it also grew EPS by 23% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Taking a look back first, we see that the company grew earnings per share by an impressive 59% last year. As a result, it also grew EPS by 23% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

首先回顧一下,我們可以看到該公司去年每股收益增長了驚人的59%。結果,在過去三年內,每股收益也增長了23%。因此,我們可以開始確認該公司在那段時間內實際上在增長收益方面做得很好。

首先回顧一下,我們可以看到該公司去年每股收益增長了驚人的59%。結果,在過去三年內,每股收益也增長了23%。因此,我們可以開始確認該公司在那段時間內實際上在增長收益方面做得很好。