Avarga Limited (SGX:U09) shares have continued their recent momentum with a 26% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 40%.

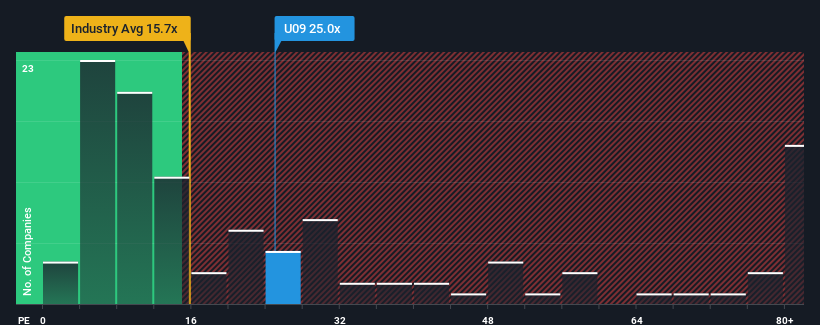

After such a large jump in price, Avarga may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 25x, since almost half of all companies in Singapore have P/E ratios under 11x and even P/E's lower than 7x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For instance, Avarga's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

SGX:U09 Price to Earnings Ratio vs Industry November 15th 2024 Although there are no analyst estimates available for Avarga, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Avarga would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 64%. This means it has also seen a slide in earnings over the longer-term as EPS is down 92% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

In contrast to the company, the rest of the market is expected to grow by 7.5% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's alarming that Avarga's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

What We Can Learn From Avarga's P/E?

Avarga's P/E is flying high just like its stock has during the last month. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Avarga currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Avarga (at least 1 which doesn't sit too well with us), and understanding these should be part of your investment process.

If you're unsure about the strength of Avarga's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In order to justify its P/E ratio, Avarga would need to produce outstanding growth well in excess of the market.

In order to justify its P/E ratio, Avarga would need to produce outstanding growth well in excess of the market.

为了证明其市盈率,合众控股需要产生远超市场的突出增长。

为了证明其市盈率,合众控股需要产生远超市场的突出增长。