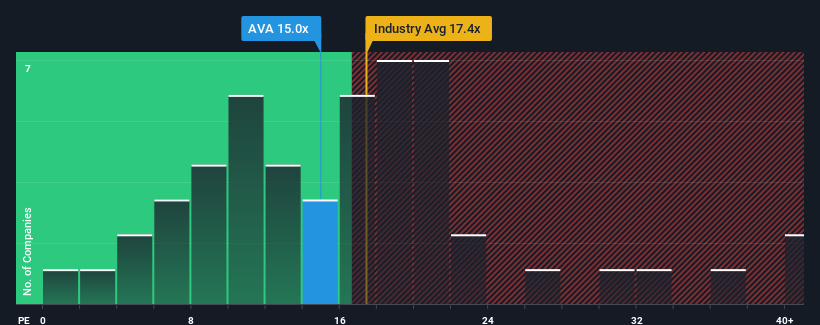

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 20x, you may consider Avista Corporation (NYSE:AVA) as an attractive investment with its 15x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

With earnings growth that's superior to most other companies of late, Avista has been doing relatively well. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

NYSE:AVA Price to Earnings Ratio vs Industry November 15th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Avista.

Is There Any Growth For Avista?

The only time you'd be truly comfortable seeing a P/E as low as Avista's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 15% last year. The latest three year period has also seen a 11% overall rise in EPS, aided extensively by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 3.8% each year over the next three years. That's shaping up to be materially lower than the 11% per annum growth forecast for the broader market.

With this information, we can see why Avista is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Avista's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 3 warning signs for Avista (1 is concerning!) that you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company grew earnings per share by an impressive 15% last year. The latest three year period has also seen a 11% overall rise in EPS, aided extensively by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Taking a look back first, we see that the company grew earnings per share by an impressive 15% last year. The latest three year period has also seen a 11% overall rise in EPS, aided extensively by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

回顧一下,我們看到該公司的每股收益去年增長了令人印象深刻的15%。最近三年的整體每股收益也上升了11%,得益於其短期表現。因此,可以公平地說,公司的盈利增長近期是相當可觀的。

回顧一下,我們看到該公司的每股收益去年增長了令人印象深刻的15%。最近三年的整體每股收益也上升了11%,得益於其短期表現。因此,可以公平地說,公司的盈利增長近期是相當可觀的。