Despite an already strong run, Ranger Energy Services, Inc. (NYSE:RNGR) shares have been powering on, with a gain of 25% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 50% in the last year.

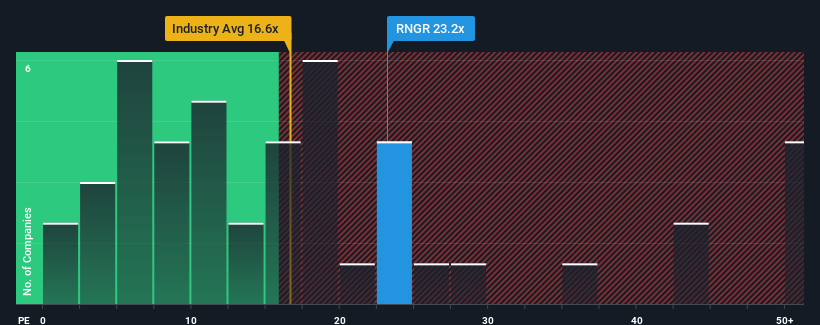

Since its price has surged higher, given around half the companies in the United States have price-to-earnings ratios (or "P/E's") below 19x, you may consider Ranger Energy Services as a stock to potentially avoid with its 23.2x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

As an illustration, earnings have deteriorated at Ranger Energy Services over the last year, which is not ideal at all. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:RNGR Price to Earnings Ratio vs Industry November 15th 2024 We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Ranger Energy Services' earnings, revenue and cash flow.

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Ranger Energy Services' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 46% decrease to the company's bottom line. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Comparing that to the market, which is predicted to deliver 15% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we find it concerning that Ranger Energy Services is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Final Word

Ranger Energy Services' P/E is getting right up there since its shares have risen strongly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Ranger Energy Services revealed its three-year earnings trends aren't impacting its high P/E anywhere near as much as we would have predicted, given they look worse than current market expectations. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Plus, you should also learn about these 2 warning signs we've spotted with Ranger Energy Services.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

儘管已經有了一波強勁的運行,ranger energy services, inc. (紐交所:RNGR) 的股票仍在繼續上漲,過去三十天增長了25%。回顧更久的時間,看到該股票在過去一年上漲了50%令人鼓舞。

由於其股價已經大幅上漲,考慮到美國大約一半的公司市盈率(或"P/E")低於19倍,你可能會認爲ranger energy services是一隻潛在需要回避的股票,因爲其P/E比率爲23.2倍。然而,P/E可能高是有原因的,仍需進一步調查以判斷其是否合理。

舉例來說,過去一年ranger energy services的盈利能力有所惡化,這絕對不是理想的情況。一個可能性是P/E高是因爲投資者認爲該公司在不久的將來仍會足夠出色以超越大盤。如果真是這樣那就太好了,否則你花了不小的代價卻沒有特別的理由。

紐交所:RNGR 市盈率與行業比較 2024年11月15日 我們沒有分析師預測,但你可以通過查看我們提供的關於ranger energy services的盈利、營業收入和現金流的免費報告,看看最近的趨勢如何爲公司的未來鋪路。

增長是否匹配高市盈率?

公司應該超越市場的這一內在假設,使得像ranger energy services這樣的市盈率才能被認爲是合理的。

根據這些信息,我們發現ranger energy services的市盈率高於市場,這讓人感到擔憂。顯然,許多投資者對該公司的看法比近期的狀況更加看好,並且不願意以任何價格賣出他們的股票。只有最勇敢的人才會認爲這些價格是可持續的,因爲近期收益趨勢的延續可能會對股票價格造成重大壓力。

最終結論

由於其股票強勁上漲,ranger energy services的市盈率已經達到了很高的水平。有人認爲在某些行業內,市盈率是一項較差的價值衡量標準,但它可以是一個強有力的業務情緒指標。

我們對ranger energy services的調查顯示,其三年的盈利趨勢並沒有像我們預測的那樣影響其高市盈率,儘管它們看起來比當前市場預期差。當我們看到盈利疲軟且增長速度慢於市場時,我們懷疑股價面臨下跌風險,從而導致高市盈率降低。如果最近的中期盈利趨勢持續下去,將會使股東的投資面臨重大風險,潛在投資者也可能因支付過高的溢價而遭受損失。

There's an inherent assumption that a company should outperform the market for P/E ratios like Ranger Energy Services' to be considered reasonable.

There's an inherent assumption that a company should outperform the market for P/E ratios like Ranger Energy Services' to be considered reasonable.

公司應該超越市場的這一內在假設,使得像ranger energy services這樣的市盈率才能被認爲是合理的。

公司應該超越市場的這一內在假設,使得像ranger energy services這樣的市盈率才能被認爲是合理的。