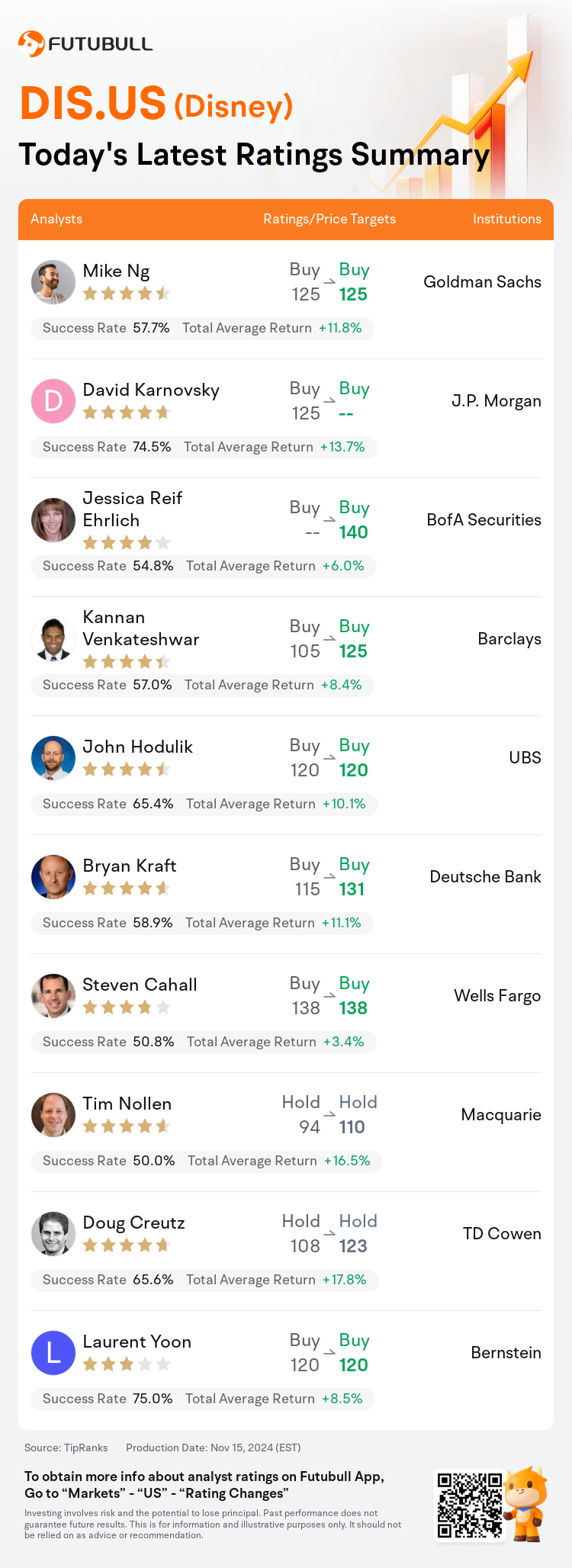

On Nov 15, major Wall Street analysts update their ratings for $Disney (DIS.US)$, with price targets ranging from $110 to $140.

Goldman Sachs analyst Mike Ng maintains with a buy rating, and maintains the target price at $125.

J.P. Morgan analyst David Karnovsky maintains with a buy rating.

BofA Securities analyst Jessica Reif Ehrlich maintains with a buy rating, and sets the target price at $140.

BofA Securities analyst Jessica Reif Ehrlich maintains with a buy rating, and sets the target price at $140.

Barclays analyst Kannan Venkateshwar maintains with a buy rating, and adjusts the target price from $105 to $125.

UBS analyst John Hodulik maintains with a buy rating, and maintains the target price at $120.

Furthermore, according to the comprehensive report, the opinions of $Disney (DIS.US)$'s main analysts recently are as follows:

Disney delivered a 'mixed' fiscal Q4 performance, with revenues surpassing estimates and operating income slightly falling short of expectations. Significantly, the optimistic investor response post-earnings is believed to be in reaction to the anticipated high single digit adjusted EPS growth for FY25, which exceeds prior forecasts, coupled with the expectation of double digit EPS growth in FY26 and FY27.

The company's guidance for fiscal 2025 surpasses expectations, while projections for 2026-2027 suggest sustained robust growth across all three operating segments. Following the earnings announcement, estimates for Disney have been revised upwards.

The company's outlook may reflect a certain level of prudence across various segments, likely aiding in meeting its declared objectives. The recent guidance issued by the company is expected to alleviate some immediate worries regarding the recent underperformance in the parks segment. When discounting the effects of cruise ship launch expenses and hurricane impacts, the inherent growth appears to be around 9%, surpassing the mid-single-digit trends observed over a longer period.

The company's recent earnings outperformance is noteworthy, and it has provided not only guidance for FY25 but also profit projections for individual divisions in FY26. Moreover, the company anticipates double-digit growth in earnings per share for both FY26 and FY27. A significant shift in the company's fundamentals can be seen in the creative execution within the studio division, where there has been more than a 50% increase in global box office revenue per franchise film over the past two years, nearing the levels seen in 2018, with potential for further growth. This cinematic success is expected to drive enhanced sales in consumer products, elevated interest in theme parks, and ultimately, contribute to increased streaming service engagement and demand.

Disney's FQ4 EBIT figures were slightly below expectations according to an analyst, although they aligned with the general market consensus. Interestingly, the company provided a three-year forecast for their earnings per share.

Here are the latest investment ratings and price targets for $Disney (DIS.US)$ from 10 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

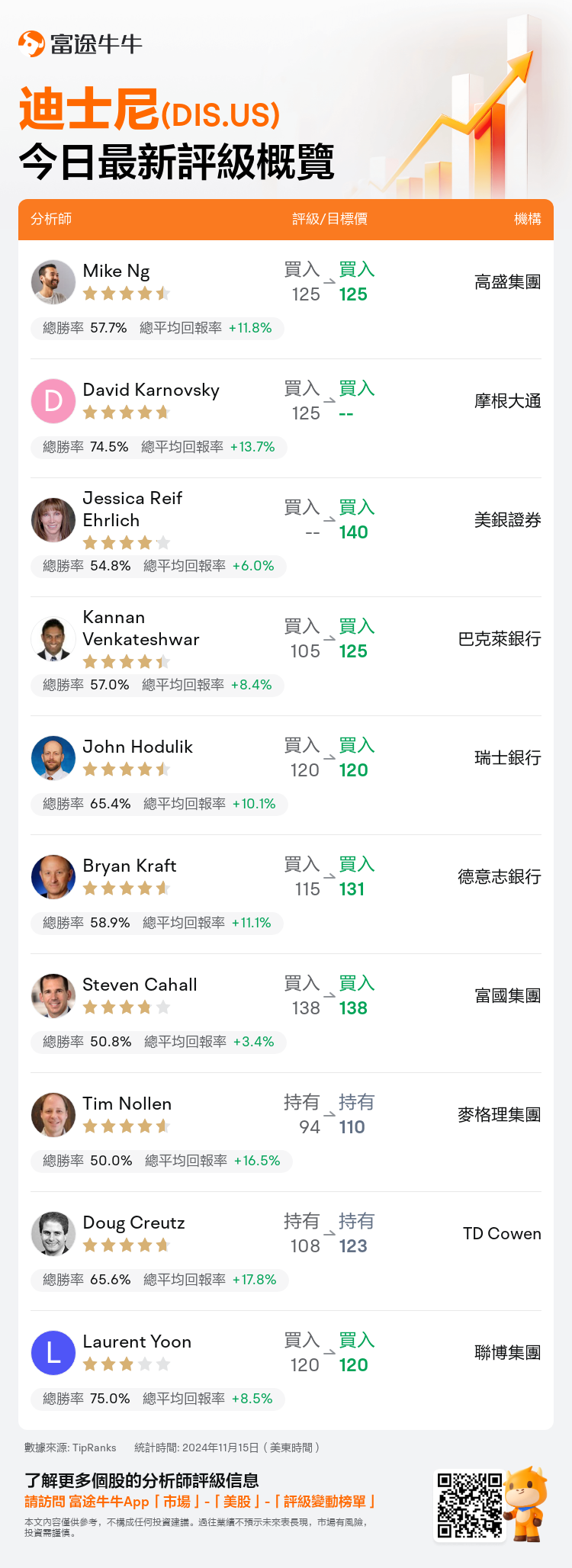

美東時間11月15日,多家華爾街大行更新了$迪士尼 (DIS.US)$的評級,目標價介於110美元至140美元。

高盛集團分析師Mike Ng維持買入評級,維持目標價125美元。

摩根大通分析師David Karnovsky維持買入評級。

美銀證券分析師Jessica Reif Ehrlich維持買入評級,目標價140美元。

美銀證券分析師Jessica Reif Ehrlich維持買入評級,目標價140美元。

巴克萊銀行分析師Kannan Venkateshwar維持買入評級,並將目標價從105美元上調至125美元。

瑞士銀行分析師John Hodulik維持買入評級,維持目標價120美元。

此外,綜合報道,$迪士尼 (DIS.US)$近期主要分析師觀點如下:

迪士尼在第四季度交出了「融合」表現,營業收入超出預期,而營業收入略低於預期。值得注意的是,投資者對收益後的樂觀回應被認爲是對FY25預期調整後的每股收益增長高位一位數增長的反應,超過了先前的預測,再加上對FY26和FY27的每股收益增長預期。

公司對2025財年的指引超出預期,而2026-2027年的預測表明,所有三個業務部門均有持續強勁增長。在收益公告後,對迪士尼的估值已經上調。

公司的前景可能體現了在各個部門中的一定謹慎度,有助於實現其宣佈的目標。公司最近發佈的指引預計將緩解有關主題公園業績不佳的一些直接擔憂。在剔除遊輪推出費用和颶風影響後,固有增長似乎約爲9%,超過了較長時期內觀察到的中單位數趨勢。

公司最近的收益表現突出,不僅提供了FY25的指引,還提供了FY26各個部門的利潤預測。此外,公司預計FY26和FY27的每股收益會有兩位數增長。公司基本面的顯著變化可以在工作室部門的創意執行中看到,過去兩年各系列電影的全球票房收入每部電影已增長了超過50%,接近2018年的水平,並有進一步增長的潛力。這種影視成功預計將推動消費產品銷量增加,主題公園的興趣增強,並最終有助於增加流媒體服務的參與度和需求。

根據一位分析師的說法,迪士尼的FQ4 EBIt數據略低於預期,儘管與市場普遍共識一致。有趣的是,公司提供了未來三年的每股收益預測。

以下爲今日10位分析師對$迪士尼 (DIS.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。