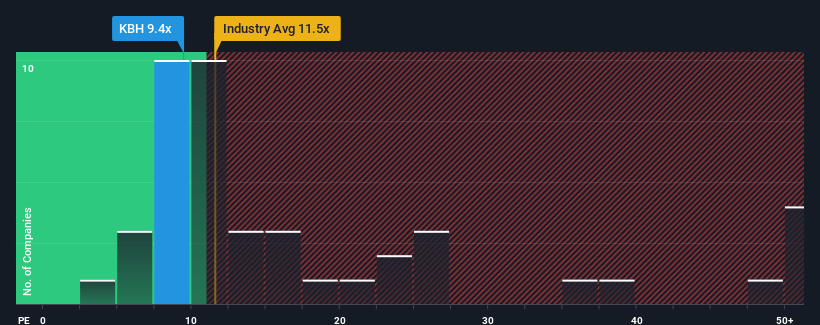

With a price-to-earnings (or "P/E") ratio of 9.4x KB Home (NYSE:KBH) may be sending very bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 20x and even P/E's higher than 35x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

KB Home's earnings growth of late has been pretty similar to most other companies. One possibility is that the P/E is low because investors think this modest earnings performance may begin to slide. If not, then existing shareholders have reason to be optimistic about the future direction of the share price.

NYSE:KBH Price to Earnings Ratio vs Industry November 15th 2024 Keen to find out how analysts think KB Home's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like KB Home's to be considered reasonable.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Still, the latest three year period has seen an excellent 54% overall rise in EPS, in spite of its uninspiring short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 12% as estimated by the eleven analysts watching the company. With the market predicted to deliver 15% growth , the company is positioned for a weaker earnings result.

In light of this, it's understandable that KB Home's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From KB Home's P/E?

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of KB Home's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for KB Home with six simple checks.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

以Kb Home (紐交所:KBH) 的市盈率爲9.4倍,目前可能正在發出非常積極的信號,考慮到美國近一半公司的市盈率大於20倍,甚至出現高達35倍以上的市盈率並不罕見。儘管如此,僅憑市盈率不明智,因爲可能有解釋爲何如此有限。

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Still, the latest three year period has seen an excellent 54% overall rise in EPS, in spite of its uninspiring short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Still, the latest three year period has seen an excellent 54% overall rise in EPS, in spite of its uninspiring short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

如果我們回顧過去一年的收益情況,公司發佈的結果幾乎與一年前沒有太大偏差。然而,在最近的三年中,每股收益整體增長了出色的54%,儘管其短期表現乏善可陳。因此,我們可以確認公司在這段時間內做了出色的收益增長。

如果我們回顧過去一年的收益情況,公司發佈的結果幾乎與一年前沒有太大偏差。然而,在最近的三年中,每股收益整體增長了出色的54%,儘管其短期表現乏善可陳。因此,我們可以確認公司在這段時間內做了出色的收益增長。