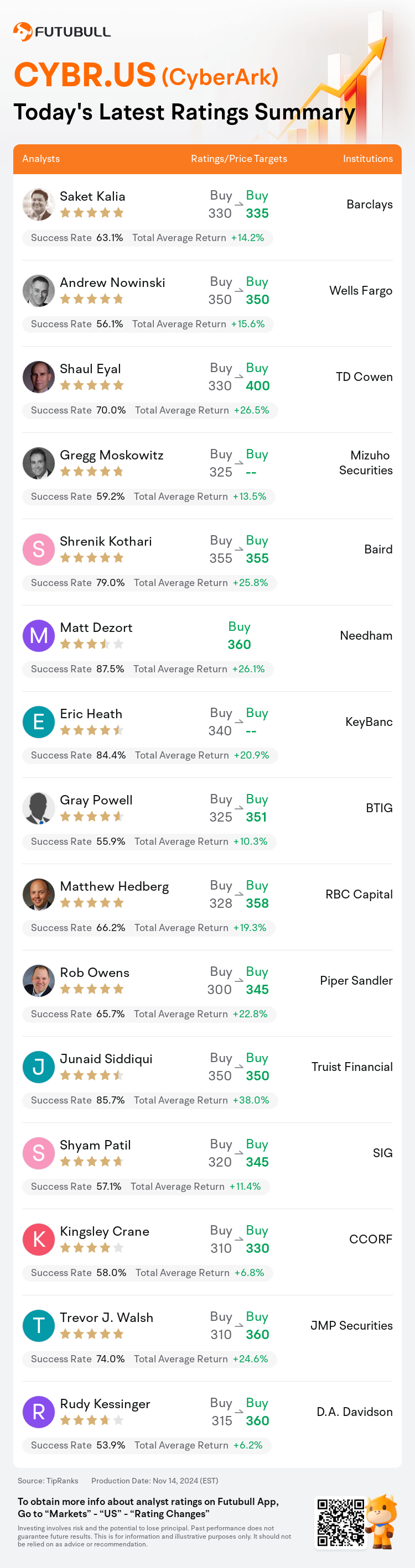

On Nov 14, major Wall Street analysts update their ratings for $CyberArk (CYBR.US)$, with price targets ranging from $330 to $400.

Barclays analyst Saket Kalia maintains with a buy rating, and adjusts the target price from $330 to $335.

Wells Fargo analyst Andrew Nowinski maintains with a buy rating, and maintains the target price at $350.

TD Cowen analyst Shaul Eyal maintains with a buy rating, and adjusts the target price from $330 to $400.

TD Cowen analyst Shaul Eyal maintains with a buy rating, and adjusts the target price from $330 to $400.

Mizuho Securities analyst Gregg Moskowitz maintains with a buy rating.

Baird analyst Shrenik Kothari maintains with a buy rating, and maintains the target price at $355.

Furthermore, according to the comprehensive report, the opinions of $CyberArk (CYBR.US)$'s main analysts recently are as follows:

The company surpassed Q3 expectations for net new annual recurring revenue and increased its fiscal 2024 free cash flow projections.

CyberArk delivered 'another strong quarter' with performance surpassing expectations in Q3 ARR, revenue, and profitability. Despite the announcement of CFO Josh Siegel's departure at year-end, the anticipated smooth transition to the experienced SVP of IR and Finance, Erica Smith, keeps confidence intact. The company is expected to continue securing a widening customer base and capitalize on several long-term favorable trends.

The firm's assessment of CyberArk reflects a positive outlook after a noteworthy Q3 ARR performance and an optimistic Q4 organic projection. The analysis suggests there is additional potential and a beneficial competitive landscape in Privileged Access Management (PAM), and sees competitive advantages in secrets management with the recent Hashi acquisition. Moreover, there are prospects for enhancing security measures atop current SSO/MFA solutions. The firm anticipates that CyberArk could enhance Venafi's growth by utilizing its expanded go-to-market resources, coupled with industry momentum for TLS certificate management. Nonetheless, there remain concerns over the total addressable market (TAM) for certificate management, the synergies with Conjur, and the emerging competition from entities such as ServiceNow, public cloud providers, and others.

Post-market trading saw CyberArk's stock dip by around 1% despite the company reporting solid results. Following the completion of the Venafi acquisition, it is believed that the company is positioned to sustain low-20s Annual Recurring Revenue growth and a free cash flow margin that surpasses the Rule of 40.

CyberArk's third-quarter results were seen as robust amidst what has been described as a rather average earnings season in the security software sector. The company not only achieved its upside target but also raised its guidance organically. Analysts have expressed optimism regarding the company's discussions on workforce identity, secrets management, and the prospects of enhancing Venafi's growth in the upcoming year. It was noted that the organic projections for 2025 remain largely unaltered.

Here are the latest investment ratings and price targets for $CyberArk (CYBR.US)$ from 15 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

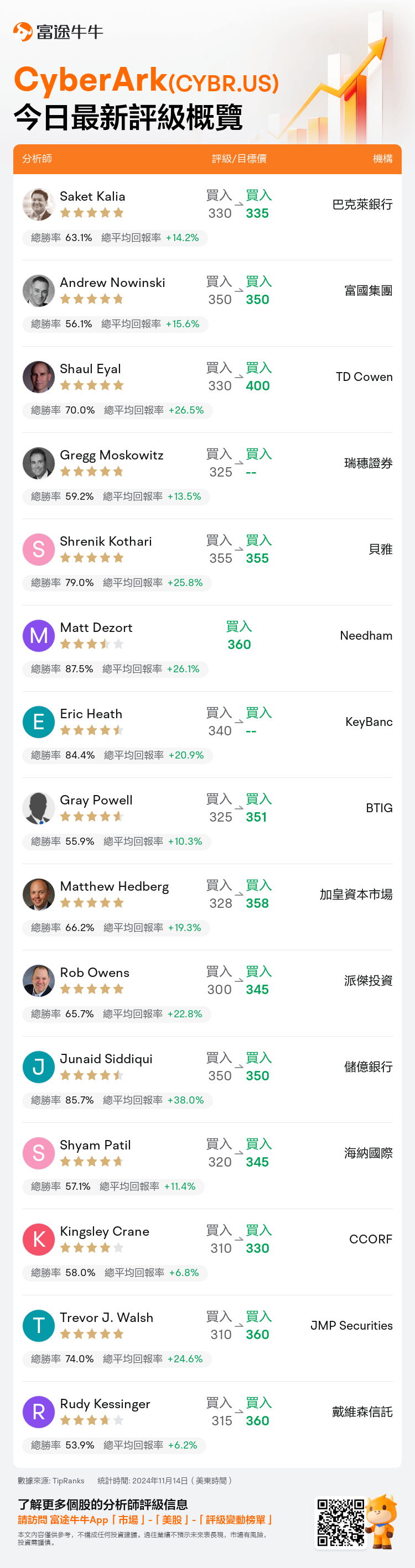

美東時間11月14日,多家華爾街大行更新了$CyberArk (CYBR.US)$的評級,目標價介於330美元至400美元。

巴克萊銀行分析師Saket Kalia維持買入評級,並將目標價從330美元上調至335美元。

富國集團分析師Andrew Nowinski維持買入評級,維持目標價350美元。

TD Cowen分析師Shaul Eyal維持買入評級,並將目標價從330美元上調至400美元。

TD Cowen分析師Shaul Eyal維持買入評級,並將目標價從330美元上調至400美元。

瑞穗證券分析師Gregg Moskowitz維持買入評級。

貝雅分析師Shrenik Kothari維持買入評級,維持目標價355美元。

此外,綜合報道,$CyberArk (CYBR.US)$近期主要分析師觀點如下:

該公司超出了第三季度對淨新年度經常性收入的預期,並提高了其2024財年的自由現金流預測。

CyberArk在第三季度的表現超出了預期,ARR、營業收入和盈利能力表現強勁。儘管首席財務官喬希·西格爾宣佈將在年底離開,但預計經驗豐富的IR和財務高級副總裁Erica Smith將順利過渡,保持了投資者的信心。預計該公司將繼續擴大客戶基礎,利用幾大長期有利趨勢。

該公司對CyberArk的評估在經歷了一個顯著的第三季度ARR表現和一個樂觀的第四季度有機投影后反映出積極的前景。分析表明,在特權訪問管理(PAM)領域還存在着額外的潛力和有利的競爭格局,並且在最近進行的Hashi收購中,具有祕密管理的競爭優勢。此外,在當前SSO/MFA解決方案的基礎上加強安全措施的前景也很好。公司預計CyberArk可以通過利用其擴展的營銷資源,結合TLS證書管理行業的動力,提升Venafi的增長。然而,對於證書管理的總可尋市場(TAM)、與Conjur的協同效應,並且來自ServiceNow、公共雲服務提供商等實體的新競爭仍存在擔憂。

美股盤後交易中,雖然該公司報告了紮實的業績,但CyberArk的股價下跌了約1%。在完成Venafi收購後,人們相信該公司定位於維持20%左右的年度經常性收入增長和超過「40規則」的自由現金流利潤率。

儘管在安全軟件行業被描述爲相當平均的盈利季節中,CyberArk的第三季度業績被認爲是強勁的。該公司不僅實現了上限目標,還自主提高了指導。分析師們對公司在關於員工身份、祕密管理以及在未來一年內提升Venafi增長前景方面的討論表示樂觀。有人指出,到2025年的有機投影基本上保持不變。

以下爲今日15位分析師對$CyberArk (CYBR.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。