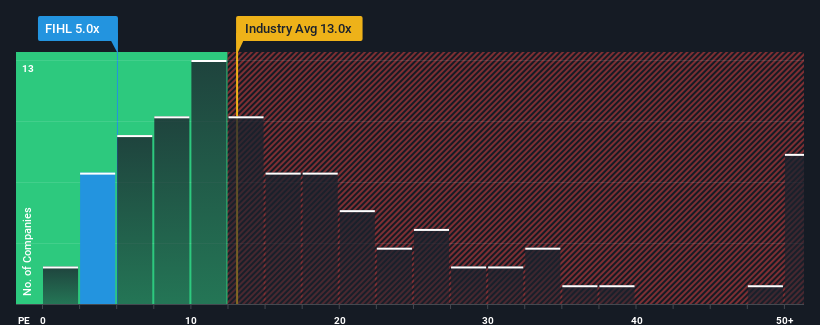

With a price-to-earnings (or "P/E") ratio of 5x Fidelis Insurance Holdings Limited (NYSE:FIHL) may be sending very bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 20x and even P/E's higher than 36x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Fidelis Insurance Holdings could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

NYSE:FIHL Price to Earnings Ratio vs Industry November 14th 2024 Keen to find out how analysts think Fidelis Insurance Holdings' future stacks up against the industry? In that case, our free report is a great place to start.

How Is Fidelis Insurance Holdings' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as depressed as Fidelis Insurance Holdings' is when the company's growth is on track to lag the market decidedly.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 74%. Even so, admirably EPS has lifted 1,044% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 20% as estimated by the five analysts watching the company. That's not great when the rest of the market is expected to grow by 15%.

In light of this, it's understandable that Fidelis Insurance Holdings' P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Fidelis Insurance Holdings' P/E?

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Fidelis Insurance Holdings' analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Fidelis Insurance Holdings that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 74%. Even so, admirably EPS has lifted 1,044% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 74%. Even so, admirably EPS has lifted 1,044% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

首先回顧一下,公司去年每股收益增長不值得興奮,因爲其大幅下降了74%。儘管如此,令人欽佩的是,從三年前算起,每股收益總體上已經增長了1,044%,儘管過去12個月的情況。因此,雖然他們本來希望能讓增長持續下去,股東們可能更願意看到中期收益增長率。

首先回顧一下,公司去年每股收益增長不值得興奮,因爲其大幅下降了74%。儘管如此,令人欽佩的是,從三年前算起,每股收益總體上已經增長了1,044%,儘管過去12個月的情況。因此,雖然他們本來希望能讓增長持續下去,股東們可能更願意看到中期收益增長率。