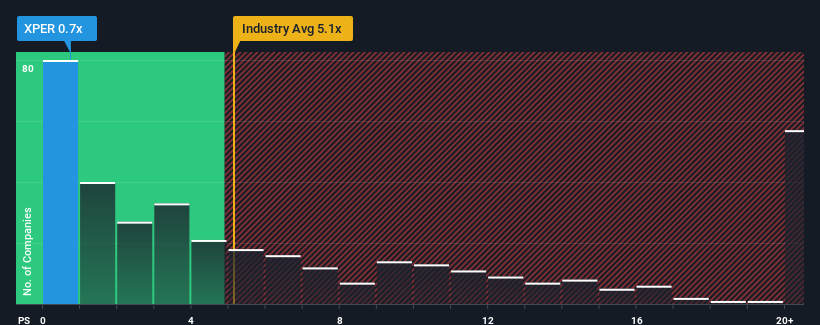

You may think that with a price-to-sales (or "P/S") ratio of 0.7x Xperi Inc. (NYSE:XPER) is definitely a stock worth checking out, seeing as almost half of all the Software companies in the United States have P/S ratios greater than 5.3x and even P/S above 13x aren't out of the ordinary. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

NYSE:XPER Price to Sales Ratio vs Industry November 13th 2024

What Does Xperi's Recent Performance Look Like?

While the industry has experienced revenue growth lately, Xperi's revenue has gone into reverse gear, which is not great. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

Want the full picture on analyst estimates for the company? Then our free report on Xperi will help you uncover what's on the horizon.

Do Revenue Forecasts Match The Low P/S Ratio?

Xperi's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 2.1%. At least revenue has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 0.3% over the next year. That's shaping up to be materially lower than the 25% growth forecast for the broader industry.

With this in consideration, its clear as to why Xperi's P/S is falling short industry peers. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Xperi's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As expected, our analysis of Xperi's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

You always need to take note of risks, for example - Xperi has 2 warning signs we think you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 2.1%. At least revenue has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 2.1%. At least revenue has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

首先回顧一下,去年公司的營業收入增長並不讓人興奮,錄得令人失望的2.1%的下滑。至少由於之前時期的增長,營業收入在整體上沒有完全倒退,相比三年前好一些。因此,我們看來公司在這段時間內在營業收入的增長上表現不一。

首先回顧一下,去年公司的營業收入增長並不讓人興奮,錄得令人失望的2.1%的下滑。至少由於之前時期的增長,營業收入在整體上沒有完全倒退,相比三年前好一些。因此,我們看來公司在這段時間內在營業收入的增長上表現不一。