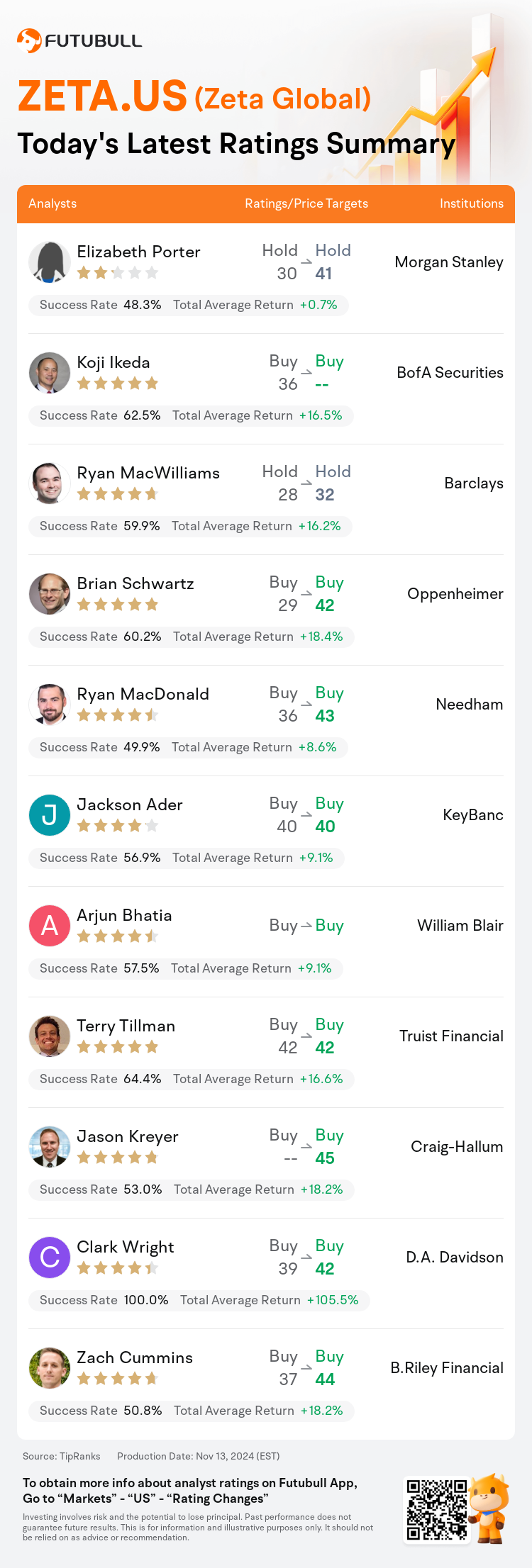

On Nov 13, major Wall Street analysts update their ratings for $Zeta Global (ZETA.US)$, with price targets ranging from $32 to $45.

Morgan Stanley analyst Elizabeth Porter maintains with a hold rating, and adjusts the target price from $30 to $41.

BofA Securities analyst Koji Ikeda maintains with a buy rating.

Barclays analyst Ryan MacWilliams maintains with a hold rating, and adjusts the target price from $28 to $32.

Barclays analyst Ryan MacWilliams maintains with a hold rating, and adjusts the target price from $28 to $32.

Oppenheimer analyst Brian Schwartz maintains with a buy rating, and adjusts the target price from $29 to $42.

Needham analyst Ryan MacDonald maintains with a buy rating, and adjusts the target price from $36 to $43.

Furthermore, according to the comprehensive report, the opinions of $Zeta Global (ZETA.US)$'s main analysts recently are as follows:

Zeta Global's Q3 revenue surpassed the initial projections by 12%, or by 5.5% when political spending is excluded. Additionally, Q4 revenue saw an increase over the initial guidance by 11%, or by 2% when excluding political spending and mergers and acquisitions. The preliminary outlook for FY25 indicates that the combination of political headwinds and M&A tailwinds could lead to mid-20s percentage growth, which may not meet expectations considering the stock's significant rise over the past three months.

The company's underlying revenue growth maintained a consistent trajectory with the previous quarter. The discussion surrounding revenue projections for 2025 focuses on the potential for customer retention in the advocacy segment and opportunities for expansion in agency services.

The company has posted a strong quarter, notching its first instance of achieving the Rule of 60 and, when excluding political revenue, another successive Rule of 50 period. Observations indicate that the forecast for FY25 suggests organic growth will persist over 20% when political revenue is discounted, laying a robust groundwork comparable to the initial projections for FY24.

Zeta Global has demonstrated another quarter of solid fundamental performance, marked by significant growth in revenue, EBITDA, and ARPU for Q3. Despite the challenging appearance of the 2025 revenue guidance, the company is still anticipated to achieve an organic growth rate in the low 20% range when adjusted for the reduced political spending impact. Furthermore, the company's execution continues to impress, and the acquisition of LiveIntent is seen as a positive shift in the company's narrative.

Here are the latest investment ratings and price targets for $Zeta Global (ZETA.US)$ from 11 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

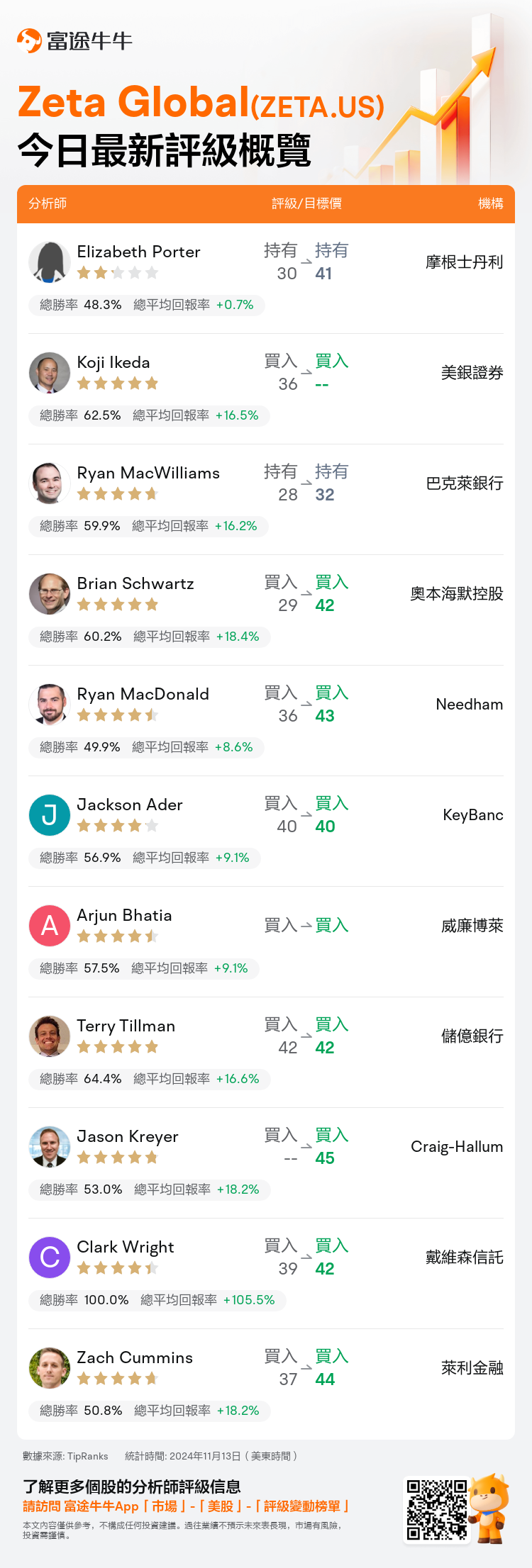

美東時間11月13日,多家華爾街大行更新了$Zeta Global (ZETA.US)$的評級,目標價介於32美元至45美元。

摩根士丹利分析師Elizabeth Porter維持持有評級,並將目標價從30美元上調至41美元。

美銀證券分析師Koji Ikeda維持買入評級。

巴克萊銀行分析師Ryan MacWilliams維持持有評級,並將目標價從28美元上調至32美元。

巴克萊銀行分析師Ryan MacWilliams維持持有評級,並將目標價從28美元上調至32美元。

奧本海默控股分析師Brian Schwartz維持買入評級,並將目標價從29美元上調至42美元。

Needham分析師Ryan MacDonald維持買入評級,並將目標價從36美元上調至43美元。

此外,綜合報道,$Zeta Global (ZETA.US)$近期主要分析師觀點如下:

Zeta Global的第三季度營業收入超過了最初的預期,提升了12%,或者在排除政治支出的情況下提升了5.5%。此外,第四季度營業收入較最初的指導增長了11%,或者在排除政治支出和併購的情況下增長了2%。對FY25的初步展望顯示,政治逆風和併購正風的組合可能導致中間20%的增長,鑑於公司股價在過去三個月內顯著上漲,這可能不符合預期。

公司的基礎營收增長保持了與上一季度一致的軌跡。關於2025年營收預測的討論集中在倡導領域客戶保留的潛力以及在代理服務拓展方面的機會。

公司發佈了強勁的季度業績,第一次實現了60規則,並在排除政治收入時,又連續實現了50規則的週期。觀察顯示,對FY25的預測表明,當政治收入被排除時,有機增長將持續超過20%,爲FY24的初步預測奠定了堅實的基礎。

Zeta Global展示了又一個季度的強勁基本表現,以第三季度營業收入、EBITDA和ARPU的顯著增長爲標誌。儘管2025年營收指導看起來具有挑戰性,但公司預計在考慮到減少政治支出影響的情況下,仍將實現低20%範圍內的有機增長率。此外,公司的執行繼續令人印象深刻,LiveIntent的收購被視爲公司敘事的積極轉變。

以下爲今日11位分析師對$Zeta Global (ZETA.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。