Telephone and Data Systems, Inc. (NYSE:TDS) shares have continued their recent momentum with a 41% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 82% in the last year.

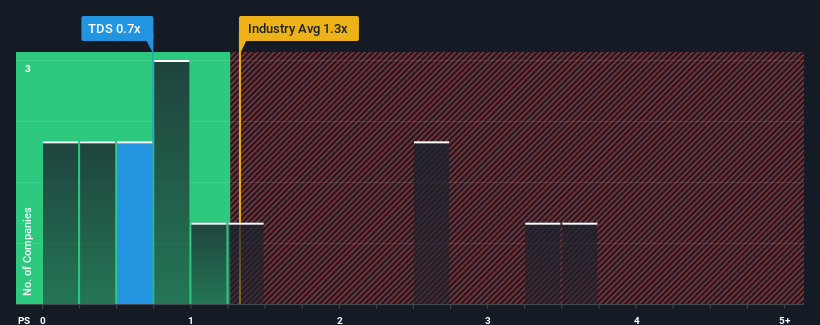

Although its price has surged higher, it's still not a stretch to say that Telephone and Data Systems' price-to-sales (or "P/S") ratio of 0.7x right now seems quite "middle-of-the-road" compared to the Wireless Telecom industry in the United States, where the median P/S ratio is around 0.8x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

NYSE:TDS Price to Sales Ratio vs Industry November 12th 2024

How Telephone and Data Systems Has Been Performing

Telephone and Data Systems could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Telephone and Data Systems.

Is There Some Revenue Growth Forecasted For Telephone and Data Systems?

The only time you'd be comfortable seeing a P/S like Telephone and Data Systems' is when the company's growth is tracking the industry closely.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 3.2%. This means it has also seen a slide in revenue over the longer-term as revenue is down 5.6% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 4.0% as estimated by the dual analysts watching the company. That's not great when the rest of the industry is expected to grow by 4.5%.

In light of this, it's somewhat alarming that Telephone and Data Systems' P/S sits in line with the majority of other companies. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

The Key Takeaway

Telephone and Data Systems appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our check of Telephone and Data Systems' analyst forecasts revealed that its outlook for shrinking revenue isn't bringing down its P/S as much as we would have predicted. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If we consider the revenue outlook, the P/S seems to indicate that potential investors may be paying a premium for the stock.

Plus, you should also learn about this 1 warning sign we've spotted with Telephone and Data Systems.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The only time you'd be comfortable seeing a P/S like Telephone and Data Systems' is when the company's growth is tracking the industry closely.

The only time you'd be comfortable seeing a P/S like Telephone and Data Systems' is when the company's growth is tracking the industry closely.

唯一讓你放心接受像電話和數據系統這樣的市銷率的時候,是當公司的增長與行業板塊密切跟蹤。

唯一讓你放心接受像電話和數據系統這樣的市銷率的時候,是當公司的增長與行業板塊密切跟蹤。