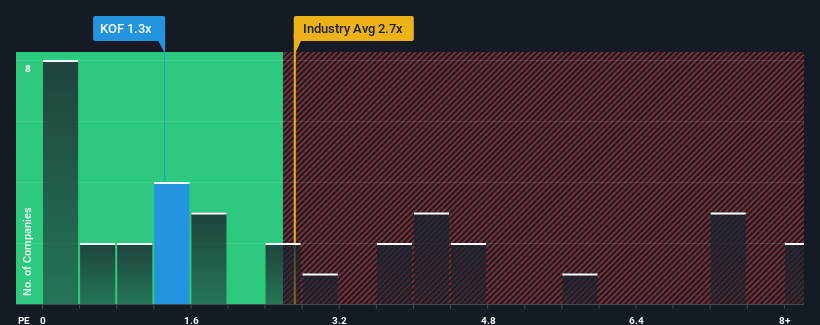

Coca-Cola FEMSA, S.A.B. de C.V.'s (NYSE:KOF) price-to-sales (or "P/S") ratio of 1.3x might make it look like a buy right now compared to the Beverage industry in the United States, where around half of the companies have P/S ratios above 2.7x and even P/S above 5x are quite common. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

NYSE:KOF Price to Sales Ratio vs Industry November 12th 2024

How Coca-Cola FEMSA. de Has Been Performing

With revenue growth that's superior to most other companies of late, Coca-Cola FEMSA. de has been doing relatively well. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Coca-Cola FEMSA. de.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

The only time you'd be truly comfortable seeing a P/S as low as Coca-Cola FEMSA. de's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 11% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 41% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 8.1% per annum over the next three years. With the industry only predicted to deliver 4.6% per year, the company is positioned for a stronger revenue result.

With this information, we find it odd that Coca-Cola FEMSA. de is trading at a P/S lower than the industry. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From Coca-Cola FEMSA. de's P/S?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Coca-Cola FEMSA. de's analyst forecasts revealed that its superior revenue outlook isn't contributing to its P/S anywhere near as much as we would have predicted. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Coca-Cola FEMSA. de with six simple checks on some of these key factors.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

可口可乐凡萨瓶装(Coca-Cola FEMSA, S.A.b. de C.V.)的市销率为1.3倍,与美国饮料行业相比,目前可能看起来是一个买入时机,因为大约一半的公司市销率超过2.7倍,甚至有市销率超过5倍的公司很常见。然而,市销率可能之所以低是有原因的,需要进一步调查来判断是否合理。

Retrospectively, the last year delivered a decent 11% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 41% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Retrospectively, the last year delivered a decent 11% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 41% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

回顾过去一年,公司的营业收入增长了可观的11%。在此之前的一段出色时期,收入总额在过去三年内增长了41%。因此,可以说公司最近的营业收入增速对公司来说非常出色。

回顾过去一年,公司的营业收入增长了可观的11%。在此之前的一段出色时期,收入总额在过去三年内增长了41%。因此,可以说公司最近的营业收入增速对公司来说非常出色。