(图片来源:中原证券)

(图片来源:中原证券)半導體的反彈之勢難道就要戛然而止了?

多日強勢拉升的半導體板塊遭遇「狙擊」?

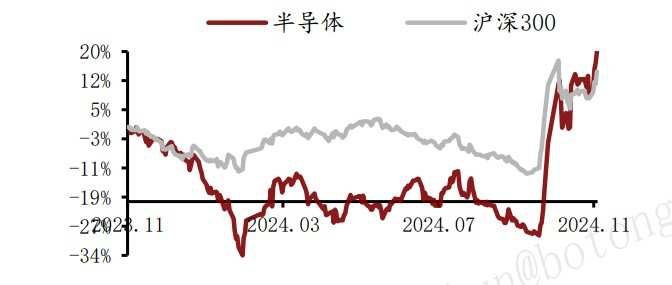

近期以來,半導體連續強勢拉升的表現無異於當下二級市場的一大討論熱點。就拿港股市場的半導體板塊而言,該板塊分別於10月4日、10月7日、10月18日、11月5日錄得30.18%、20.83%、15.44%、6.25%的漲幅,這對於在2023年底至2024年初跌入「谷底」的半導體板塊而言,不亞於一場明顯的底部反轉喜訊。

(圖片來源:中原證券)

(圖片來源:中原證券)

然而,好景不長。伴隨着今日(11月12日)大盤的回落調整,港股的半導體板塊也顯露了明顯的跌勢——11月12日港股收盤,該板塊大跌7.42%,跌幅靠前,板塊內概念股近乎全數轉跌,康特隆(01912)大跌11.51%領跌,中芯國際(00981)、上海復旦(01385)則均跌超7%。

從消息面來看,據路透,美國商務部致函台積電,要求從11日開始停止向中國大陸客戶供應7納米及更先進工藝的AI芯片。這一出口限制措施主要針對用於人工智能加速器以及圖形處理單元(GPU)的芯片。消息人士稱台積電通知受影響客戶,將從11日起暫停相關芯片發貨。

這一次半導體的反彈之勢難道就要戛然而止了嗎?

國產芯片加速替代的「多重邏輯」

客觀來說,特朗普上臺後,國內半導體行業恐將迎來一次「機遇與挑戰並存」的發展機遇。

挑戰在於,在特朗普上一次執政時期,便一直熱衷於用貿易限制和制裁手段遏制中國的技術進步。這次特朗普再次當選,很可能會延續這種強硬的對華政策,此前就已經提到要對中國進口產品加徵60%-100%的關稅。如若進一步加大對中國半導體產業的制裁力度,將給中國半導體企業帶來更大的挑戰。

不過,對於國產芯片替代而言,這將「機遇大於挑戰」。因爲,這或將推動國產芯片替代加速,迎來新的一輪上升週期。而穿透當下國內半導體的發展趨勢來看,主要有以下多重增長邏輯,具體如下:

一是,從國產替代的角度來看,隨着特朗普上臺後,美國或將進一步加大對華的科技限制,從而刺激中國半導體自主可控的發展。

衆所周知,在AI和GPU領域,製程技術的先進程度直接關係到產品的性能,進而導致成本增加和產品上市時間延長,在設備和代工雙重受限的背景下,中國大陸半導體設備廠商急需加大高端設備的研發以支持本土先進製程產能的擴建,實現半導體產業鏈的國產化。

不論是對國內芯片設計企業限制先進製程的代工,還是審查並收緊半導體材料、設備的對華出口,均有助於加速國產替代進度,有望催生半導體設備、製造、先進封裝、芯片定製服務全產業鏈的國產替代投資機遇。

其中,海通證券指出,隨着外部影響升級,預計先進製程流片將更加嚴格,中國本土建設先進工藝產線阻力有所增加,但相關規則無法抵消海外芯片廠商在中國的真實需求。中國芯片產業鏈除了個別環節仍然需要時間攻克,整體基本已經趨於完善,預計半導體等關鍵領域國產替代趨勢依舊會延續。

二是,從政策助力角度來看,半導體是當前國家政策大力支持的首要發展行業,在當前全球形勢複雜多變的背景下,推動半導體行業國產自主可控是最確定的發展趨勢之一。

今年5月24日,國家集成電路大基金三期成立,註冊資本達3440億元,超出一二期資本總和。大基金三期的成立標誌着中國半導體產業即將邁入一個新的發展階段。與前兩期相比,三期的投資規模更大,預計將重點投資於先進晶圓製造、關鍵設備和零部件等環節,加速推動上游設備材料的國產替代。這一舉措將有助於解決國內半導體產業在關鍵技術領域的「卡脖子」問題,提升產業鏈的自主可控能力。

大基金三期的註冊資本3440億元,預計將撬動超過1萬億的半導體領域投資額,顯示出國家對半導體產業的強大支持力度。這一規模的投資不僅能夠爲半導體產業提供充足的資金支持,還將吸引更多的社會資本投入到半導體產業中,形成良好的投資氛圍。

鑑於上,不難看出,在政策持續支持+外部環境驅動國產替代加速推進下,國內半導體設備及零部件、半導體材料、AI算力芯片等方向均有望延續較高增速。

行業週期反轉驅動業績強勢復甦

在消費電子需求低迷、產能集中釋放、高規格產品仍待驗證等因素的影響下,半導體行業於2022年至2023年遭遇低谷期已然是不爭的事實。

然而,伴隨着半導體在2024上半年出現補庫存需求,這一行業已經逐步走出低谷,迎來週期反轉。

以數據爲實。

據SIA數據,24年9月全球半導體行業銷售額達到553億美元,同比+23.2%,環比+4.1%。全球半導體市場在24Q3繼續增長,季度銷售額增長速度爲2016年以來的最大增速,9月份的銷售額達到了市場有史以來最高的月度總銷售額,這得益於美洲地區同比增長46.3%。

從地區來看,9月份日本(5.3%)、亞太地區/所有其他(4.5%)、美洲(4.1%)、歐洲(4.0%)和中國(3.6%)的月度銷售額均有所增長。

半導體行業的週期反轉,顯然也體現在相關公司的業績表現上。

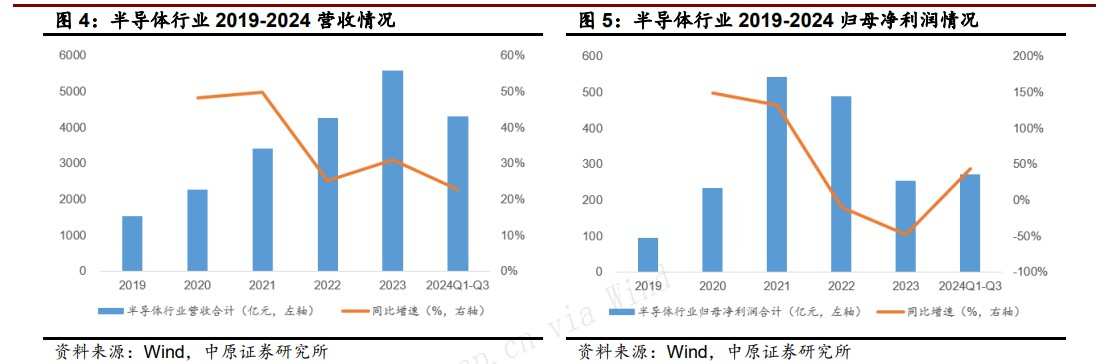

據相關研報披露,隨着庫存的去化,以及下游需求回暖,2024 年前三季度半導體行業(中信)營業收入爲4296.41 億元,同比增長 22.57%,歸母淨利潤爲 272.11 億元,同比增長 42.91%。

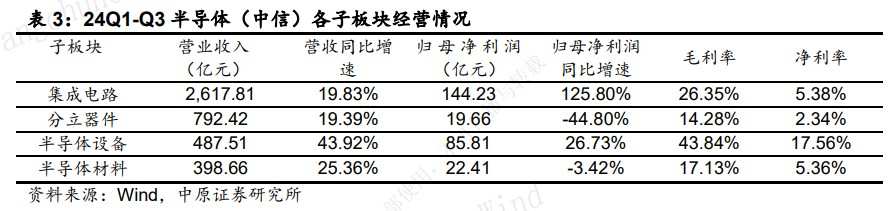

細化來看,同期,集成電路、分立器件、半導體設備和半導體材料板塊營收分別同比增長 19.83%、 19.39%、43.92%、25.36%;集成電 路、分立器件、半導體設備和半導體材料板塊歸母淨利潤分別同比增長 125.80%、-44.80%、26.73%、- 3.42%。

而透過「晶圓代工雙雄」中芯國際(00981,688981.SH)、華虹半導體(01347,688347.SH)第三季度的業績來看,亦可以窺出此次行業的反轉之勢。

據業績數據披露,2024年第三季度,中芯國際營收156.1億元,同比增長32.5%,環比上升14%,且單季度營收首次突破20億美元,創歷史新高。同時,第三季度淨利潤達到10.6億元,同比增長超56%。華虹半導體也同樣利潤大增,期內該公司營收5.3億美元,同比下滑7.4%,環比增長10%;歸屬母公司淨利潤達4480萬美元,扭虧爲盈同比增長2倍以上,環比大增超過5倍。

更值得關注的是,兩大代工巨頭的產能利用率今年開始都在穩步提升。第三季度,中芯國際產能利用率達到90.4%,去年同期只有77.1%。華虹半導體產能利用率進一步提升到105.3%,去年三季度爲86.8%。作爲衡量工廠生產能力是否得到充分利用的一項關鍵指標,產能利用率直接決定晶圓代工廠的盈利水平。伴隨着產能利用率的大幅提升,這兩家公司的盈利水平也隨之大幅提升。

綜上來看,半導體行業的週期反轉顯然傳導到到了估值和業績上的提升。根據華福證券進一步預計,隨着外部限制不斷升級,國產替代催化投資機遇,本土設備企業有望延續高景氣,相關設備廠商有望擴大份額,預計2025年國產化率將達50%。這也意味着,半導體短期的震盪不足以影響國產半導體行業的中長期發展上行。