Despite an already strong run, RadNet, Inc. (NASDAQ:RDNT) shares have been powering on, with a gain of 26% in the last thirty days. The annual gain comes to 200% following the latest surge, making investors sit up and take notice.

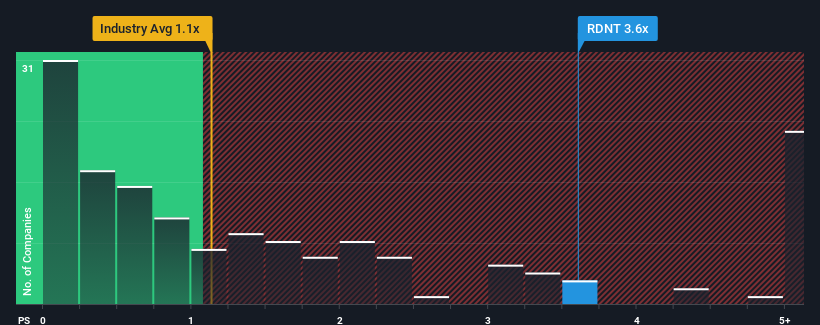

After such a large jump in price, when almost half of the companies in the United States' Healthcare industry have price-to-sales ratios (or "P/S") below 1.2x, you may consider RadNet as a stock not worth researching with its 3.6x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

NasdaqGM:RDNT Price to Sales Ratio vs Industry November 12th 2024

How RadNet Has Been Performing

RadNet certainly has been doing a good job lately as it's been growing revenue more than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on RadNet will help you uncover what's on the horizon.

Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, RadNet would need to produce outstanding growth that's well in excess of the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 12%. Pleasingly, revenue has also lifted 37% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 7.3% during the coming year according to the five analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 7.5%, which is not materially different.

With this in consideration, we find it intriguing that RadNet's P/S is higher than its industry peers. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

The strong share price surge has lead to RadNet's P/S soaring as well. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Analysts are forecasting RadNet's revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. A positive change is needed in order to justify the current price-to-sales ratio.

Before you take the next step, you should know about the 2 warning signs for RadNet that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In order to justify its P/S ratio, RadNet would need to produce outstanding growth that's well in excess of the industry.

In order to justify its P/S ratio, RadNet would need to produce outstanding growth that's well in excess of the industry.

爲了證明其市銷率,radnet需要實現遠遠超過行業的出色增長。

爲了證明其市銷率,radnet需要實現遠遠超過行業的出色增長。