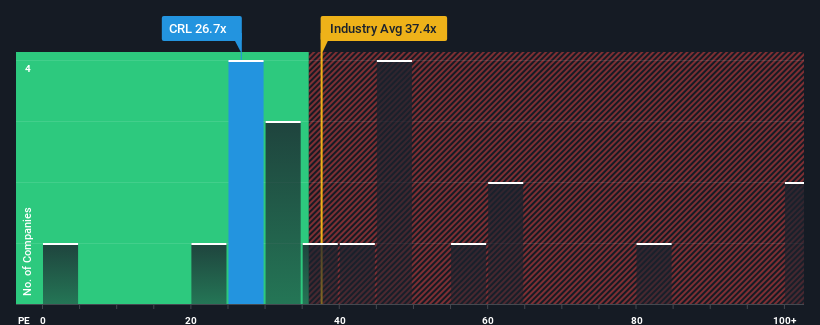

With a price-to-earnings (or "P/E") ratio of 26.7x Charles River Laboratories International, Inc. (NYSE:CRL) may be sending bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 19x and even P/E's lower than 11x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Charles River Laboratories International could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:CRL Price to Earnings Ratio vs Industry November 11th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Charles River Laboratories International.

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Charles River Laboratories International's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 14%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next three years should generate growth of 7.0% per year as estimated by the analysts watching the company. That's shaping up to be materially lower than the 10% per annum growth forecast for the broader market.

With this information, we find it concerning that Charles River Laboratories International is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

What We Can Learn From Charles River Laboratories International's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Charles River Laboratories International's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Charles River Laboratories International you should know about.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 14%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 14%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

如果我們回顧去年的收益,令人沮喪的是公司的利潤下降了14%。不幸的是,這讓它回到了三年前幾乎沒有整體EPS增長的起點。因此,股東們可能不會對不穩定的中期增長率感到滿意。

如果我們回顧去年的收益,令人沮喪的是公司的利潤下降了14%。不幸的是,這讓它回到了三年前幾乎沒有整體EPS增長的起點。因此,股東們可能不會對不穩定的中期增長率感到滿意。