There's been a notable change in appetite for TPI Composites, Inc. (NASDAQ:TPIC) shares in the week since its third-quarter report, with the stock down 18% to US$2.82. Revenues of US$381m beat expectations by a respectable 5.9%, although statutory losses per share increased. TPI Composites lost US$0.84, which was 484% more than what the analysts had included in their models. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

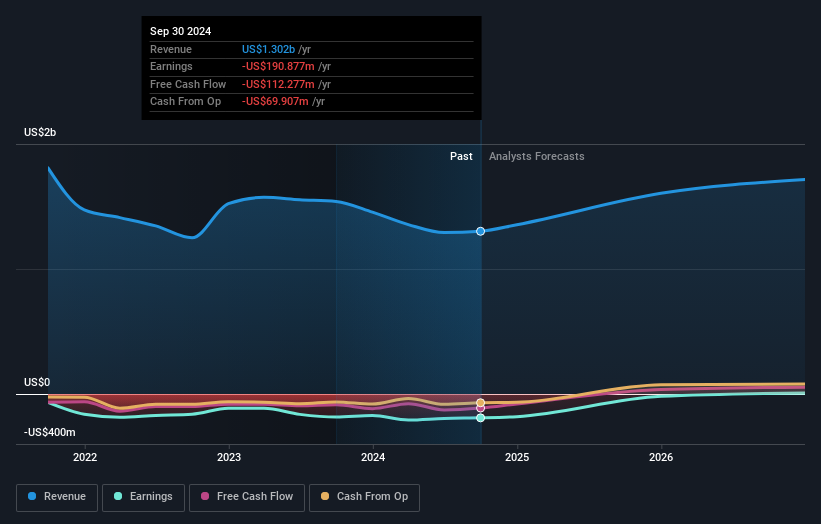

Taking into account the latest results, the consensus forecast from TPI Composites' twelve analysts is for revenues of US$1.61b in 2025. This reflects a huge 23% improvement in revenue compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 88% to US$0.50. Before this latest report, the consensus had been expecting revenues of US$1.64b and US$0.44 per share in losses. So it's pretty clear the analysts have mixed opinions on TPI Composites even after this update; although they reconfirmed their revenue numbers, it came at the cost of a considerable increase in per-share losses.

The consensus price target fell 11% to US$4.58per share, with the analysts clearly concerned by ballooning losses. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on TPI Composites, with the most bullish analyst valuing it at US$8.00 and the most bearish at US$2.75 per share. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing stands out from these estimates, which is that TPI Composites is forecast to grow faster in the future than it has in the past, with revenues expected to display 18% annualised growth until the end of 2025. If achieved, this would be a much better result than the 1.5% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 8.6% annually. So it looks like TPI Composites is expected to grow faster than its competitors, at least for a while.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing stands out from these estimates, which is that TPI Composites is forecast to grow faster in the future than it has in the past, with revenues expected to display 18% annualised growth until the end of 2025. If achieved, this would be a much better result than the 1.5% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 8.6% annually. So it looks like TPI Composites is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that in mind, we wouldn't be too quick to come to a conclusion on TPI Composites. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple TPI Composites analysts - going out to 2026, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 3 warning signs for TPI Composites (1 shouldn't be ignored!) that you should be aware of.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.