Here's Why We Think Hamilton Insurance Group (NYSE:HG) Might Deserve Your Attention Today

Here's Why We Think Hamilton Insurance Group (NYSE:HG) Might Deserve Your Attention Today

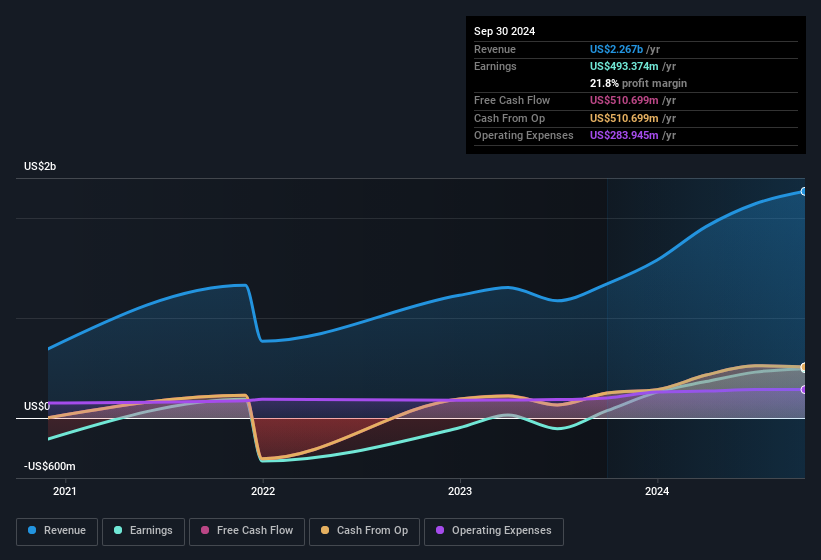

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Not all of Hamilton Insurance Group's revenue this year is revenue

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Not all of Hamilton Insurance Group's revenue this year is revenue The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

對於一些投機者來說,投資一家可能逆轉其命運的公司的興奮情緒是一個巨大的吸引力,因此即使是沒有營業收入、沒有利潤並且一直表現不佳的公司也可以找到投資者。但現實情況是,當一家公司每年虧損足夠長時間時,投資者通常會承擔這些損失的一部分。虧損的公司可以像資本海綿一樣吸收資金,因此投資者應該謹慎,不要把好錢投向壞錢後面。

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Hamilton Insurance Group (NYSE:HG). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

儘管處於科技股藍天投資時代,許多投資者仍然採用更傳統的策略;購買像漢密爾頓保險集團這樣盈利的公司的股份(紐交所:HG)。雖然這並不一定意味着它被低估,但企業的盈利足以值得一定程度的讚賞 - 尤其是如果它正在增長。

Hamilton Insurance Group's Improving Profits

漢密爾頓保險集團盈利能力提升

Investors and investment funds chase profits, and that means share prices tend rise with positive earnings per share (EPS) outcomes. So for many budding investors, improving EPS is considered a good sign. It's an outstanding feat for Hamilton Insurance Group to have grown EPS from US$0.70 to US$4.87 in just one year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future. But the key is discerning whether something profound has changed, or if this is a just a one-off boost.

投資者和投資基金追逐利潤,這意味着隨着盈利每股收益(EPS)結果的積極增長,股價往往會上漲。因此,對許多新手投資者來說,提高EPS被視爲一個好跡象。漢密爾頓保險集團在短短一年內,將EPS從0.70美元增長到4.87美元,這是一項出色的成就。雖然很難以這種速度維持增長,但這對公司未來的前景是一個好兆頭。但關鍵在於判斷是否發生了重大變化,或者這只是一次性的提振。

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Not all of Hamilton Insurance Group's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers used in this article might not be the best representation of the underlying business. Hamilton Insurance Group shareholders can take confidence from the fact that EBIT margins are up from 11% to 30%, and revenue is growing. Ticking those two boxes is a good sign of growth, in our book.

檢查公司增長的一種方法是觀察其營業收入和利息稅前利潤(EBIT)利潤率的變化。今年漢密爾頓保險集團的營業收入並非全部來自業務收入,因此請記住,本文中使用的收入和利潤率數字可能不是對基礎業務的最佳代表。漢密爾頓保險集團的股東可以從EBIt利潤率從11%上升到30%以及營業收入增長中獲得信心。在我們看來,當這兩方面都達標時,這是增長的一個好跡象。

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

在下面的圖表中,您可以看到該公司隨着時間的推移如何增長收入和收益。單擊圖表以查看確切的數字。

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Hamilton Insurance Group's future profits.

你不會把注意力放在後視鏡上開車,所以你可能更感興趣這份免費報告,顯示分析師對漢密爾頓保險集團未來利潤的預測。

Are Hamilton Insurance Group Insiders Aligned With All Shareholders?

漢密爾頓保險集團內部人與所有股東保持一致嗎?

It's pleasing to see company leaders with putting their money on the line, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. Hamilton Insurance Group followers will find comfort in knowing that insiders have a significant amount of capital that aligns their best interests with the wider shareholder group. Indeed, they hold US$48m worth of its stock. That's a lot of money, and no small incentive to work hard. Despite being just 2.7% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

看到公司領導人把他們的錢置於一條線上是令人高興的,這增加了經營者和真正股東之間激勵機制的一致性。漢密爾頓保險集團的追隨者們會放心,因爲他們知道內部人擁有大量資本,與更廣泛的股東群體的最佳利益保持一致。他們持有價值4800萬美元的股票。這是一大筆錢,也是一個努力工作的巨大激勵。儘管僅佔公司的2.7%,但這筆投資的價值足以表明內部人在這個創業公司上有很大的賭注。

Does Hamilton Insurance Group Deserve A Spot On Your Watchlist?

漢密爾頓保險集團值得加入您的自選名單嗎?

Hamilton Insurance Group's earnings per share growth have been climbing higher at an appreciable rate. This level of EPS growth does wonders for attracting investment, and the large insider investment in the company is just the cherry on top. At times fast EPS growth is a sign the business has reached an inflection point, so there's a potential opportunity to be had here. Based on the sum of its parts, we definitely think its worth watching Hamilton Insurance Group very closely. You should always think about risks though. Case in point, we've spotted 1 warning sign for Hamilton Insurance Group you should be aware of.

漢密爾頓保險集團的每股收益增長速度一直在以可觀的速度攀升。這種EPS增速對吸引投資產生了奇妙的作用,而公司內部的大規模投資只是錦上添花。有時候,快速的EPS增長是業務已經到達拐點的跡象,因此這裏可能存在機會。基於其各部分的總和,我們確實認爲值得密切關注漢密爾頓保險集團。但您始終要考慮到風險。以此爲例,我們發現了漢密爾頓保險集團的1個警示信號,您應該注意。

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a tailored list of companies which have demonstrated growth backed by significant insider holdings.

總是有可能買入未增長收益並且內部人員不買入股票的股票表現良好。但是對於那些認爲這些重要指數的人,我們鼓勵您查看具有這些功能的公司。您可以訪問定製列表,其中列出了已經展示出增長並得到內幕人員認可的公司。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文討論的內部交易是指在相關司法管轄區中報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接與我們聯繫。或者,發送電子郵件至editorial-team @ simplywallst.com。

Simply Wall St的這篇文章是一般性質的。我們僅基於歷史數據和分析師預測提供評論,使用公正的方法,我們的文章並非意在提供財務建議。這並不構成買入或賣出任何股票的建議,並且不考慮您的目標或財務狀況。我們旨在爲您帶來基於基礎數據驅動的長期聚焦分析。請注意,我們的分析可能未考慮最新的價格敏感公司公告或定性材料。Simply Wall St對提及的任何股票都沒有持倉。

譯文內容由第三人軟體翻譯。