Despite an already strong run, Incyte Corporation (NASDAQ:INCY) shares have been powering on, with a gain of 25% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 57% in the last year.

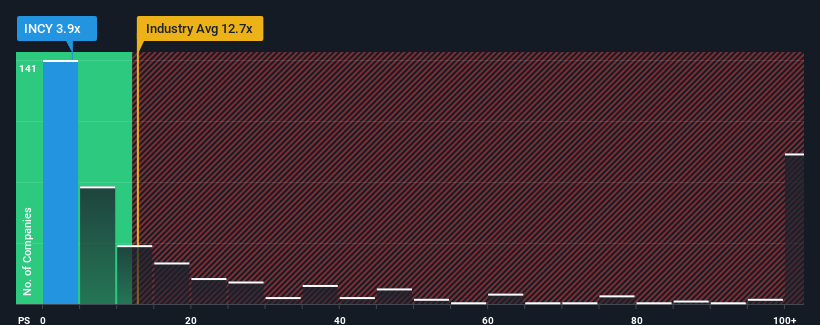

Although its price has surged higher, Incyte may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 3.9x, since almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 12.7x and even P/S higher than 72x are not unusual. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

NasdaqGS:INCY Price to Sales Ratio vs Industry November 8th 2024

What Does Incyte's Recent Performance Look Like?

Recent times haven't been great for Incyte as its revenue has been rising slower than most other companies. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Incyte will help you uncover what's on the horizon.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Incyte would need to produce anemic growth that's substantially trailing the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 13%. The latest three year period has also seen an excellent 40% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 10% per annum during the coming three years according to the analysts following the company. With the industry predicted to deliver 120% growth per year, the company is positioned for a weaker revenue result.

With this information, we can see why Incyte is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Incyte's recent share price jump still sees fails to bring its P/S alongside the industry median. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As expected, our analysis of Incyte's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. The company will need a change of fortune to justify the P/S rising higher in the future.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Incyte, and understanding them should be part of your investment process.

If you're unsure about the strength of Incyte's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In order to justify its P/S ratio, Incyte would need to produce anemic growth that's substantially trailing the industry.

In order to justify its P/S ratio, Incyte would need to produce anemic growth that's substantially trailing the industry.

爲了證明其市銷率,因塞特需要產生營業收入增長不足行業水平的低迷增長。

爲了證明其市銷率,因塞特需要產生營業收入增長不足行業水平的低迷增長。