Zymeworks Inc. (NASDAQ:ZYME) Analysts Just Slashed Next Year's Revenue Estimates By 16%

Zymeworks Inc. (NASDAQ:ZYME) Analysts Just Slashed Next Year's Revenue Estimates By 16%

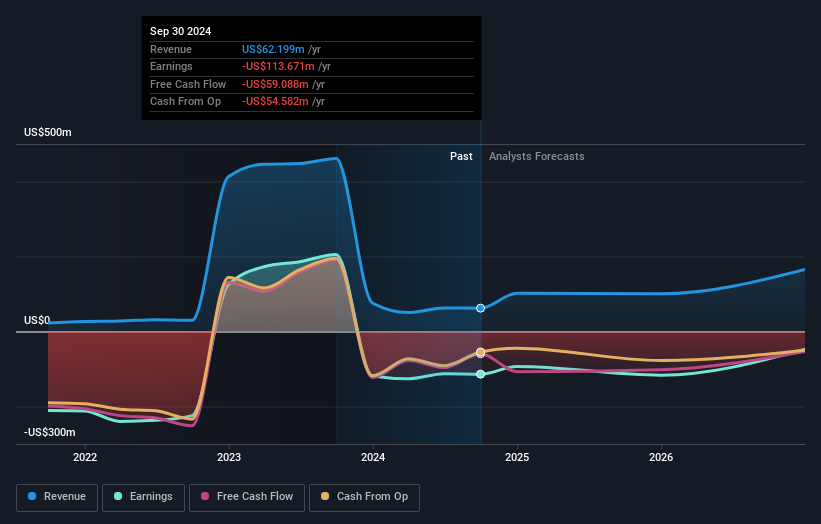

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Zymeworks' rate of growth is expected to accelerate meaningfully, with the forecast 47% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 38% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 21% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Zymeworks to grow faster than the wider industry.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Zymeworks' rate of growth is expected to accelerate meaningfully, with the forecast 47% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 38% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 21% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Zymeworks to grow faster than the wider industry. The analysts covering Zymeworks Inc. (NASDAQ:ZYME) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for next year. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic. Bidders are definitely seeing a different story, with the stock price of US$16.77 reflecting a 22% rise in the past week. It will be interesting to see if the downgrade has an impact on buying demand for the company's shares.

覆盖Zymeworks Inc. (纳斯达克:ZYME) 的分析师今天向股东们传递了一剂负面消息,对明年的法定预测进行了重大修订。他们对营业收入的预估有相当严格的下调,或许是对之前预测过于乐观的一种隐含承认。竞标人显然看到了不同的情况,美元16.77的股价反映了过去一周上涨了22%。看看这次下调是否对公司股票的购买需求产生影响,将会非常有趣。

After the downgrade, the seven analysts covering Zymeworks are now predicting revenues of US$101m in 2025. If met, this would reflect a substantial 62% improvement in sales compared to the last 12 months. Prior to the latest estimates, the analysts were forecasting revenues of US$120m in 2025. The consensus view seems to have become more pessimistic on Zymeworks, noting the measurable cut to revenue estimates in this update.

在下调之后,对Zymeworks进行覆盖的七位分析师现在预测2025年的营业收入为10,100万美元。如果达到这一水平,将反映出销售额较过去12个月实现了大幅增长的62%。在最新的预估之前,分析师们预测2025年的营业收入为12,000万美元。共识观点似乎对Zymeworks变得更为悲观,特别注意了这次更新中对营业收入预估的显著下调。

The consensus price target rose 9.0% to US$15.15, with the analysts clearly more optimistic about Zymeworks' prospects following this update.

共识目标价上涨了9.0%,达到15.15美元,分析师们显然对Zymeworks的前景更为乐观。

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Zymeworks' rate of growth is expected to accelerate meaningfully, with the forecast 47% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 38% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 21% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Zymeworks to grow faster than the wider industry.

当然,审视这些预测的另一种方式就是将其与行业本身放在一个背景下进行考量。从最新的预估中可以明显看出,Zymeworks的增长速度预计会加速,预计到2025年年底年化营收增长率将达到47%,明显快于过去五年38%的历史增长率。相比之下,我们的数据显示,其他类似行业(有分析师覆盖)的公司预计其营业收入每年增长21%。很显然,虽然增长前景比最近的过去更为光明,但分析师们也期待Zymeworks增长速度超过更广泛行业的增长速度。

The Bottom Line

最重要的事情是分析师增加了它对下一年每股亏损的估计。令人欣慰的是,营收预测未发生重大变化,业务仍有望比整个行业增长更快。共识价格目标稳定在28.50美元,最新估计不足以对价格目标产生影响。

The most important thing to take away is that analysts cut their revenue estimates for next year. They're also forecasting more rapid revenue growth than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Zymeworks after today.

最重要的一点是,分析师们调低了明年的营业收入预期。他们还预测营业收入增速将比整个市场更快。价格目标也有所增加,表明预测中蕴含的乐观情绪比之前更多。通常情况下,一次下调会引发连锁反应,特别是当行业处于衰退时。因此,如果市场在今天之后变得更加谨慎,对Zymeworks感到意外也就不足为奇。

Unanswered questions? At least one of Zymeworks' seven analysts has provided estimates out to 2026, which can be seen for free on our platform here.

有未解决的问题吗?至少有一名Zymeworks的七名分析师提供了截至2026年的预测,可以在我们的平台上免费查看。

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

当然,看到公司管理层投入大量资金投资股票的情况与分析师是否对其评级下调一样有用。因此,您还可以搜索此处的高内部所有权股票的免费列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。