Revenue Miss: Everest Group, Ltd. Fell 9.6% Short Of Analyst Revenue Estimates And Analysts Have Been Revising Their Models

Revenue Miss: Everest Group, Ltd. Fell 9.6% Short Of Analyst Revenue Estimates And Analysts Have Been Revising Their Models

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Everest Group's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 6.1% growth on an annualised basis. This is compared to a historical growth rate of 14% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 5.3% annually. So it's pretty clear that, while Everest Group's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

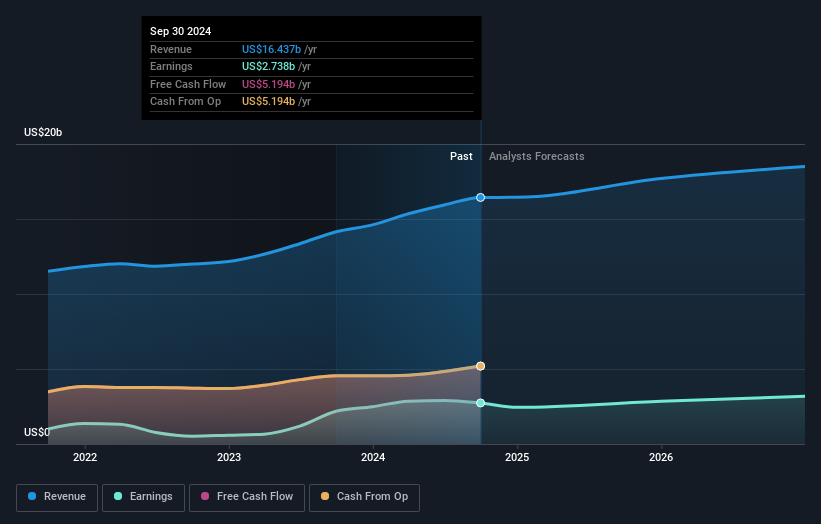

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Everest Group's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 6.1% growth on an annualised basis. This is compared to a historical growth rate of 14% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 5.3% annually. So it's pretty clear that, while Everest Group's revenue growth is expected to slow, it's expected to grow roughly in line with the industry. Everest Group, Ltd. (NYSE:EG) last week reported its latest third-quarter results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. Results look mixed - while revenue fell marginally short of analyst estimates at US$3.8b, statutory earnings were in line with expectations, at US$11.80 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

珠穆朗瑪峯集團有限公司(紐約證券交易所代碼:EG)上週公佈了其最新的第三季度業績,這是投資者深入研究業務表現是否符合預期的好時機。業績好壞參半——雖然收入略低於分析師預期的38億美元,但法定收益符合預期,爲每股11.80美元。分析師通常會在每份收益報告中更新他們的預測,我們可以從他們的估計中判斷他們對公司的看法是否發生了變化,或者是否有任何新的問題需要注意。我們認爲,讀者會發現分析師對明年最新(法定)業績後的預測很有趣。

Taking into account the latest results, the current consensus from Everest Group's six analysts is for revenues of US$17.7b in 2025. This would reflect an okay 7.7% increase on its revenue over the past 12 months. Per-share earnings are expected to increase 3.1% to US$65.66. In the lead-up to this report, the analysts had been modelling revenues of US$18.6b and earnings per share (EPS) of US$67.58 in 2025. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a minor downgrade to earnings per share estimates.

考慮到最新業績,珠穆朗瑪峯集團的六位分析師目前的共識是,2025年收入爲177億美元。這將反映出其在過去12個月中收入增長了7.7%。每股收益預計將增長3.1%,至65.66美元。在本報告發布之前,分析師一直在模擬2025年收入爲186億美元,每股收益(EPS)爲67.58美元。很明顯,在最新業績公佈後,悲觀情緒已經抬頭,導致收入前景疲軟,每股收益預期略有下調。

The analysts made no major changes to their price target of US$432, suggesting the downgrades are not expected to have a long-term impact on Everest Group's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Everest Group analyst has a price target of US$517 per share, while the most pessimistic values it at US$383. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Everest Group shareholders.

分析師沒有對432美元的目標股價做出重大調整,這表明下調評級預計不會對珠穆朗瑪峯集團的估值產生長期影響。但是,這並不是我們可以從這些數據中得出的唯一結論,因爲一些投資者在評估分析師目標股價時也喜歡考慮估計值的差異。最樂觀的珠穆朗瑪峯集團分析師將目標股價定爲每股517美元,而最悲觀的分析師則將其估值爲383美元。分析師對該業務的看法肯定各不相同,但我們認爲,估計的分歧還不夠廣泛,不足以表明珠穆朗瑪峯集團股東可能會有極端的結果。

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Everest Group's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 6.1% growth on an annualised basis. This is compared to a historical growth rate of 14% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 5.3% annually. So it's pretty clear that, while Everest Group's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

現在從大局來看,我們理解這些預測的方法之一是了解它們與過去的業績和行業增長估計相比如何。很明顯,預計珠穆朗瑪峯集團的收入增長將大幅放緩,預計到2025年底的收入按年計算將增長6.1%。相比之下,過去五年的歷史增長率爲14%。將其與業內其他有分析師報道的公司並列,預計這些公司的收入(總計)每年將增長5.3%。因此,很明顯,儘管珠穆朗瑪峯集團的收入增長預計將放緩,但預計其增長將與行業大致持平。

The Bottom Line

底線

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Sadly, they also downgraded their revenue forecasts, but the business is still expected to grow at roughly the same rate as the industry itself. The consensus price target held steady at US$432, with the latest estimates not enough to have an impact on their price targets.

要了解的最重要的一點是,分析師下調了每股收益的預期,這表明公佈這些業績後,市場情緒明顯下降。遺憾的是,他們還下調了收入預期,但預計該業務的增長速度仍將與該行業本身大致相同。共識目標股價穩定在432美元,最新估計不足以對其目標價格產生影響。

With that in mind, we wouldn't be too quick to come to a conclusion on Everest Group. Long-term earnings power is much more important than next year's profits. We have forecasts for Everest Group going out to 2026, and you can see them free on our platform here.

考慮到這一點,我們不會很快就珠穆朗瑪峯集團得出結論。長期盈利能力比明年的利潤重要得多。我們對珠穆朗瑪峯集團的預測將持續到2026年,你可以在我們的平台上免費查看。

You can also see our analysis of Everest Group's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

您還可以看到我們對珠穆朗瑪峯集團董事會和首席執行官薪酬和經驗的分析,以及公司內部人士是否一直在購買股票。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎?直接聯繫我們。或者,發送電子郵件給編輯組(網址爲)simplywallst.com。

Simply Wall St 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

譯文內容由第三人軟體翻譯。