After-hours trading of airbnb (ABNB) was exciting, as the current performance exceeded expectations following the announcement of Q3 financial report, leading to an initial surge of over 9%. However, due to lower guidance than expected, it gave back all the gains and slightly declined.

Performance

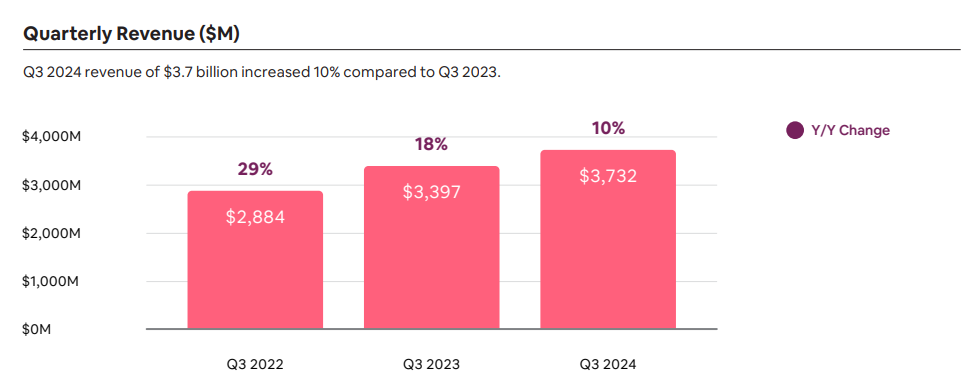

Total revenue: $3.7 billion, a 10% year-on-year increase, slightly exceeding expectations.

Net income: $1.4 billion, with an EPS of $2.13, slightly lower than the market's expected $2.16.

EBITDA profit: $1.958 billion, surpassing the expected $1.86 billion.

EBITDA profit: $1.958 billion, surpassing the expected $1.86 billion.Total booking amount: reached $20.1 billion, a 10% year-on-year increase, exceeding the market's expected $19.8 billion.

Number of booked nights and experiences: a total of 0.1228 billion times, an 8% year-on-year increase.

Free cash flow: $1.1 billion, reflecting the company's strong cash generation capability.

![big]()

Performance Analysis

International Market Growth: The company has shown strong performance in the international market, with continued leadership in the Asia-Pacific and Latin America regions.

In the Asia-Pacific region, booking volume increased by 19% year-on-year, maintaining the growth rate from the second quarter, mainly driven by cross-border travel, with a 23% year-on-year increase in booking volume. The business recovery in the Asia-Pacific region has been gradual, particularly encouraged by the recovery of outbound business from China.

Booking volume in Latin America increased by 15% year-on-year, showing a slight slowdown from the 17% growth rate in the second quarter. However, travel within the region continues to show strong momentum, with a 21% year-on-year increase in domestic night bookings in the third quarter.

Short-term rental demand is rising: With the recovery of travel activities, short-term rental demand has significantly increased, especially on the eve of the holiday season.

Application usage increase: Booking through the mobile application accounts for 58% of total bookings, an 18% year-on-year increase, demonstrating the improvement in user experience and the effectiveness of technological investments.

![big]()

Company Guidance

Overall, the company's guidance for Q4 performance is below market expectations.

Revenue: Expected to be $2.39 billion to $2.44 billion, with median below market consensus of $2.42 billion.

Lodging and experience booking volume: Expected to grow by over 8.5%, slightly exceeding market expectations of 7.7% growth.

EBITDA: The adjusted EBITDA profit margin for the full year is expected to be 35.5%, with the company originally expecting at least 35%.

Due to the company's expectation of higher nights and experience bookings in the fourth quarter compared to the third quarter, holiday season demand remains strong.