Investors Shouldn't Be Too Comfortable With Cimpress' (NASDAQ:CMPR) Earnings

Investors Shouldn't Be Too Comfortable With Cimpress' (NASDAQ:CMPR) Earnings

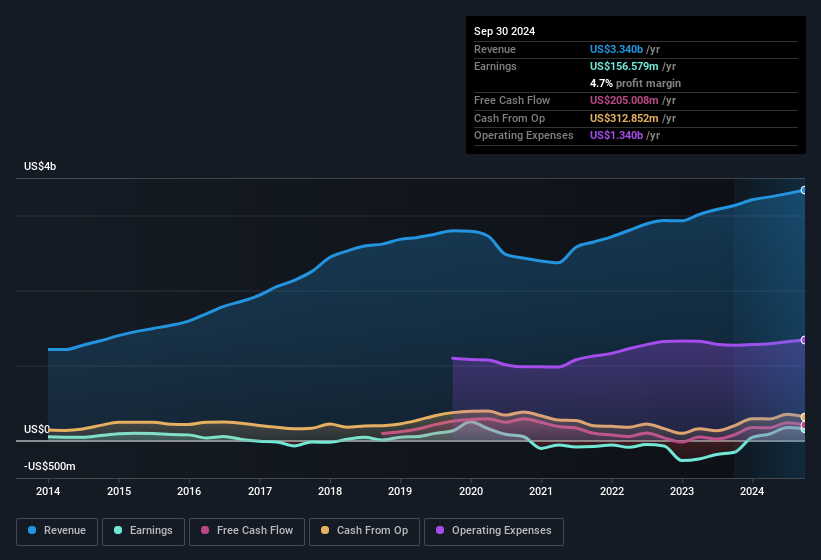

As we have already discussed Cimpress reported that it received a tax benefit, rather than paying tax, in the last year. Given that sort of benefit is not recurring, a focus on the statutory profit might make the company seem better than it really is. Therefore, it seems possible to us that Cimpress' true underlying earnings power is actually less than its statutory profit. The good news is that it earned a profit in the last twelve months, despite its previous loss. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, Cimpress has

As we have already discussed Cimpress reported that it received a tax benefit, rather than paying tax, in the last year. Given that sort of benefit is not recurring, a focus on the statutory profit might make the company seem better than it really is. Therefore, it seems possible to us that Cimpress' true underlying earnings power is actually less than its statutory profit. The good news is that it earned a profit in the last twelve months, despite its previous loss. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, Cimpress has Cimpress plc's (NASDAQ:CMPR) robust earnings report didn't manage to move the market for its stock. Our analysis suggests that this might be because shareholders have noticed some concerning underlying factors.

Cimpress股份有限公司(纳斯达克:CMPR)强劲的季度财报未能推动其股票市场。我们的分析表明,这可能是因为股东们注意到一些令人担忧的潜在因素。

An Unusual Tax Situation

一种不寻常的税务情况

We can see that Cimpress received a tax benefit of US$48m. This is of course a bit out of the ordinary, given it is more common for companies to be paying tax than receiving tax benefits! The receipt of a tax benefit is obviously a good thing, on its own. And given that it lost money last year, it seems possible that the benefit is evidence that it now expects to find value in its past tax losses. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. So while we think it's great to receive a tax benefit, it does tend to imply an increased risk that the statutory profit overstates the sustainable earnings power of the business.

我们可以看到Cimpress获得了税收优惠,金额为4800万美元。这当然有点不同寻常,通常公司缴税而非获得税收优惠!获得税收优惠显然是一件好事。考虑到去年它亏损,现在获得税收优惠可能意味着它预计能够从过去的税收亏损中找到价值。然而,事实细节在于,这类优惠仅在被确认的那一年产生影响,并且通常是一次性的。在税收优惠不会重复的情况下,我们预计其法定利润水平将下降,至少在没有强劲增长的情况下。因此,虽然我们认为获得税收优惠是一件好事,但这可能意味着法定利润过多地反映了业务的可持续盈利能力。

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

这可能会让您想知道分析师对未来盈利能力的预测。幸运的是,您可以单击此处查看基于其估计的未来盈利能力的互动图表。

Our Take On Cimpress' Profit Performance

我们对Cimpress的盈利表现的看法

As we have already discussed Cimpress reported that it received a tax benefit, rather than paying tax, in the last year. Given that sort of benefit is not recurring, a focus on the statutory profit might make the company seem better than it really is. Therefore, it seems possible to us that Cimpress' true underlying earnings power is actually less than its statutory profit. The good news is that it earned a profit in the last twelve months, despite its previous loss. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, Cimpress has 2 warning signs (and 1 which is potentially serious) we think you should know about.

正如我们已经讨论过的,cimpress报告称,去年获得了税收优惠,而不是支付税款。考虑到这种收益并不是重复出现的,专注于法定利润可能会让公司看起来比实际情况好。因此,我们认为cimpress真正的基本盈利能力实际上可能低于其法定利润。好消息是,尽管之前亏损,它在过去十二个月里盈利了。归根结底,如果您想要正确地了解这家公司,重要的是要考虑比以上因素更多的因素。鉴于这一点,如果您想对该公司进行更多分析,了解涉及的风险就显得至关重要。例如,我们认为cimpress有2个警示信号(其中1个可能是严重的),您应该了解。

This note has only looked at a single factor that sheds light on the nature of Cimpress' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

这份说明只关注了揭示cimpress盈利性质的单一因素。但如果您能够集中注意力在细枝末节上,总是会有更多发现。例如,许多人认为高净资产回报率是良好业务经济的指标,而另一些人喜欢“跟着资金走”,寻找内部人士在买入的股票。虽然这可能需要您做一些调查,但您可能会发现这个免费的拥有高净资产回报率的公司收藏或者这个拥有重要内部持股的股票清单,会对您有所帮助。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧吗?请直接与我们联系。或者,发送电子邮件至editorial-team @ simplywallst.com。

Simply Wall St的这篇文章是一般性质的。我们仅基于历史数据和分析师预测提供评论,使用公正的方法,我们的文章并非意在提供财务建议。这并不构成买入或卖出任何股票的建议,并且不考虑您的目标或财务状况。我们旨在为您带来基于基础数据驱动的长期聚焦分析。请注意,我们的分析可能未考虑最新的价格敏感公司公告或定性材料。Simply Wall St对提及的任何股票都没有持仓。

译文内容由第三方软件翻译。