The Garmin Ltd. (NYSE:GRMN) share price has done very well over the last month, posting an excellent gain of 27%. The last 30 days bring the annual gain to a very sharp 82%.

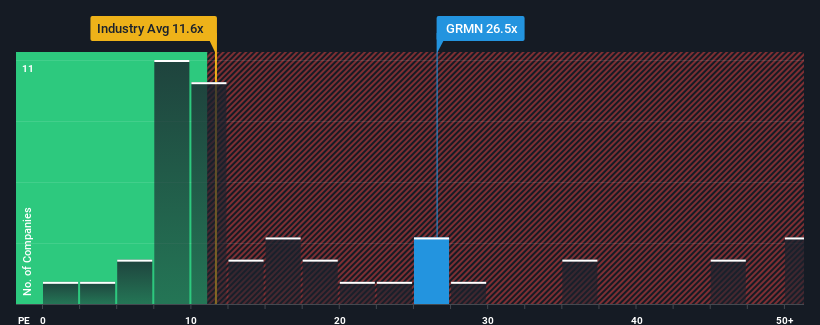

Since its price has surged higher, Garmin's price-to-earnings (or "P/E") ratio of 26.5x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 11x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Garmin certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:GRMN Price to Earnings Ratio vs Industry November 7th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Garmin.

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Garmin's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 46% last year. Pleasingly, EPS has also lifted 34% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 4.7% each year during the coming three years according to the eight analysts following the company. Meanwhile, the rest of the market is forecast to expand by 11% each year, which is noticeably more attractive.

With this information, we find it concerning that Garmin is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Key Takeaway

Garmin shares have received a push in the right direction, but its P/E is elevated too. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Garmin currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Garmin you should know about.

Of course, you might also be able to find a better stock than Garmin. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should outperform the market for P/E ratios like Garmin's to be considered reasonable.

There's an inherent assumption that a company should outperform the market for P/E ratios like Garmin's to be considered reasonable.

有一個固有的假設,即一家公司的市盈率應該表現優於市場才能被認爲合理。

有一個固有的假設,即一家公司的市盈率應該表現優於市場才能被認爲合理。