On Nov 06, major Wall Street analysts update their ratings for $Marqeta (MQ.US)$, with price targets ranging from $7 to $7.

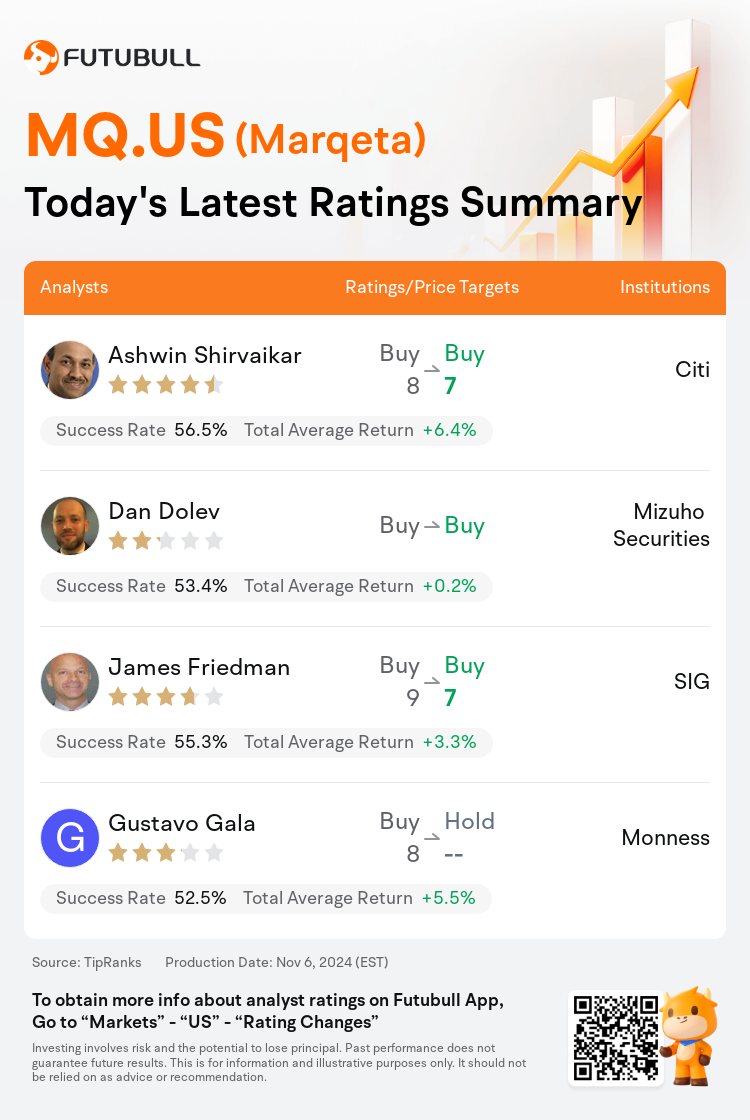

Citi analyst Ashwin Shirvaikar maintains with a buy rating, and adjusts the target price from $8 to $7.

Mizuho Securities analyst Dan Dolev maintains with a buy rating.

SIG analyst James Friedman maintains with a buy rating, and adjusts the target price from $9 to $7.

SIG analyst James Friedman maintains with a buy rating, and adjusts the target price from $9 to $7.

Monness analyst Gustavo Gala downgrades to a hold rating.

Furthermore, according to the comprehensive report, the opinions of $Marqeta (MQ.US)$'s main analysts recently are as follows:

Marqeta reported mixed results for Q3 and reduced its growth forecast for Q4 and fiscal year 2025, primarily due to extended onboarding periods stemming from increased regulatory examination and the associated risk appetites of sponsor banks. Estimates have been adjusted in light of these developments.

Marqeta's recent performance has been underwhelming post the renewal event with Block. This has led to the anticipation that the company's valuation might align more closely with its cash value following after-hours trading. Despite this, it is anticipated that Marqeta will have to demonstrate its capabilities into 2025 due to recent challenges in execution.

Marqeta's recent performance indicated a modest shortfall in Q3 gross profit growth, although it exceeded expectations for adjusted EBITDA due to stringent operational discipline. Nonetheless, the company significantly reduced its forecast, attributing this revision to increased oversight from the banking sector, which has postponed the onboarding of new clients, and a reduction in value-added services from current clients. Additionally, it was observed that several of Marqeta's advanced fintech clients have chosen to internalize parts of their program management and banking relationships.

Marqeta's third-quarter performance was notably below expectations, marking a challenging period in its brief tenure on the public market. The unexpected shift in the regulatory landscape led to a considerable revision of guidance and introduced uncertainty for the year 2025. Despite reduced projections, the outlook for Marqeta's extended-term path remains positive.

The Q3 earnings report for Marqeta was overshadowed by a significant reduction in the revenue and gross profit forecast for fiscal 2024, alongside a preliminary forecast for fiscal 2025 growth that is anticipated to be considerably under both the company's and analysts' previous estimates. The expected materially lower growth rate for fiscal 2025 is due to a combination of external factors and added challenges stemming from customer in-sourcing. The perspective shared is that it is not necessary to hold a bullish stance on the stock until the regulatory and implementation challenges, as well as the business model issues, are addressed.

Here are the latest investment ratings and price targets for $Marqeta (MQ.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間11月6日,多家華爾街大行更新了$Marqeta (MQ.US)$的評級,目標價介於7美元至7美元。

花旗分析師Ashwin Shirvaikar維持買入評級,並將目標價從8美元下調至7美元。

瑞穗證券分析師Dan Dolev維持買入評級。

海納國際分析師James Friedman維持買入評級,並將目標價從9美元下調至7美元。

海納國際分析師James Friedman維持買入評級,並將目標價從9美元下調至7美元。

Monness分析師Gustavo Gala下調至持有評級。

此外,綜合報道,$Marqeta (MQ.US)$近期主要分析師觀點如下:

Marqeta報告了Q3的混合業績,並將其Q4和2025財年的增長預期下調,主要是由於監管審查期的延長以及贊助銀行的相關風險偏好。在這些發展的背景下,估算已經進行了調整。

Marqeta最近的表現在與Block的續約事件之後表現不佳。這導致人們預計,公司的估值可能在盤後交易後更接近其現金價值。儘管如此,預計Marqeta將不得不展示其能力,由於最近在執行方面遇到的挑戰,預計到2025年。

Marqeta最近的表現表明Q3的毛利潤增長略有不足,儘管由於嚴格的運營紀律,它超出了對調整後EBITDA的預期。儘管如此,公司顯著降低了其預測,將這一修訂歸因於來自銀行板塊的監督加強,這推遲了新客戶的入職,並減少了當前客戶提供的增值服務。此外,觀察到Marqeta的一些先進金融科技客戶選擇內部化其部分程序管理和銀行關係。

Marqeta的第三季度表現明顯低於預期,標誌着在公開市場短暫任期中的一個充滿挑戰的時期。監管形勢的意外變化導致對指導的重大修訂,併爲2025年引入不確定性。儘管降低了預測,但對於Marqeta的長期路徑,展望仍然是積極的。

Marqeta的Q3收益報告被財年2024年的營業收入和毛利潤預測大幅減少所掩蓋,同時對預計的財年2025年增長提出了初步預測,預計將明顯低於公司和分析師以前的估計。由於外部因素和來自客戶內部源的附加挑戰,預計2025財年增長速度會大大降低。分享的觀點是,在處理監管和執行方面的挑戰以及業務模式問題之前,不必對該股採取看好態度。

以下爲今日4位分析師對$Marqeta (MQ.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。