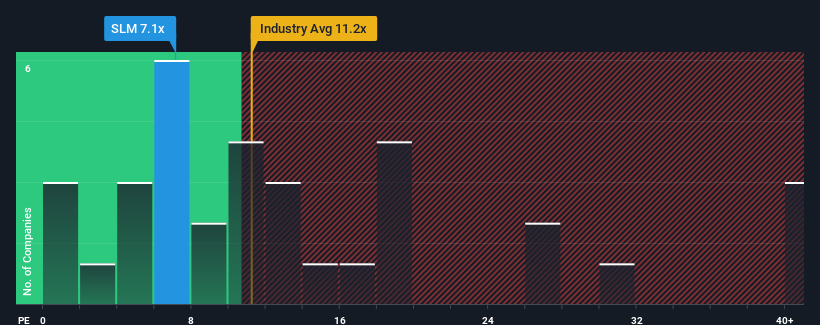

With a price-to-earnings (or "P/E") ratio of 7.1x SLM Corporation (NASDAQ:SLM) may be sending very bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 19x and even P/E's higher than 34x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

SLM certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NasdaqGS:SLM Price to Earnings Ratio vs Industry November 4th 2024 Want the full picture on analyst estimates for the company? Then our free report on SLM will help you uncover what's on the horizon.

How Is SLM's Growth Trending?

In order to justify its P/E ratio, SLM would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered an exceptional 118% gain to the company's bottom line. Still, incredibly EPS has fallen 20% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 0.6% as estimated by the eight analysts watching the company. Meanwhile, the broader market is forecast to expand by 15%, which paints a poor picture.

With this information, we are not surprised that SLM is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that SLM maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 4 warning signs for SLM you should be aware of, and 3 of them are concerning.

If you're unsure about the strength of SLM's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered an exceptional 118% gain to the company's bottom line. Still, incredibly EPS has fallen 20% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Retrospectively, the last year delivered an exceptional 118% gain to the company's bottom line. Still, incredibly EPS has fallen 20% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

回顧過去一年,公司底線異常增長了118%。然而,令人難以置信的是,每股收益從三年前開始總共下降了20%,這令人相當失望。相應地,股東們可能對中期盈利增長率感到悲觀。

回顧過去一年,公司底線異常增長了118%。然而,令人難以置信的是,每股收益從三年前開始總共下降了20%,這令人相當失望。相應地,股東們可能對中期盈利增長率感到悲觀。