Here's Why We Think Trinity Industries (NYSE:TRN) Might Deserve Your Attention Today

Here's Why We Think Trinity Industries (NYSE:TRN) Might Deserve Your Attention Today

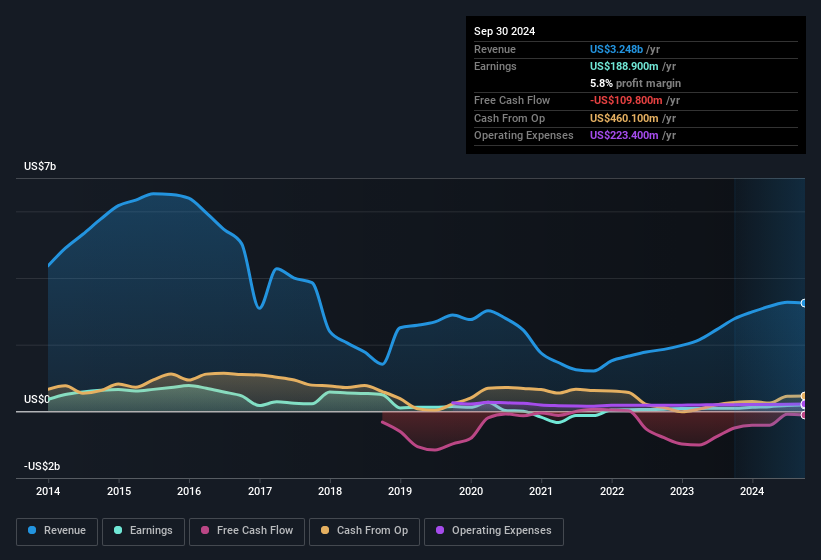

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Trinity Industries shareholders can take confidence from the fact that EBIT margins are up from 9.6% to 14%, and revenue is growing. Both of which are great metrics to check off for potential growth.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Trinity Industries shareholders can take confidence from the fact that EBIT margins are up from 9.6% to 14%, and revenue is growing. Both of which are great metrics to check off for potential growth. For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

对于初学者来说,买一个向投资者讲述好故事的公司似乎是一个好主意(也是一个令人兴奋的前景),即使它目前缺少营业收入和利润的记录。不幸的是,这些高风险投资往往很少有可能产生回报,许多投资者付出代价来学习他们的教训。亏损的公司可以像吸取资本的海绵一样 - 所以投资者应谨慎,不要把好钱投进去。

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Trinity Industries (NYSE:TRN). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

如果这种公司不符合你的风格,你喜欢创造营业收入甚至盈利的公司,那么你可能会对trinity industries(纽交所:TRN)感兴趣。虽然利润并非是投资时唯一的衡量标准,但值得注意的是那些能够稳定产生利润的企业。

How Fast Is Trinity Industries Growing Its Earnings Per Share?

trinity industries的每股收益增长速度有多快?

Trinity Industries has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. So it would be better to isolate the growth rate over the last year for our analysis. Impressively, Trinity Industries' EPS catapulted from US$1.10 to US$2.30, over the last year. Year on year growth of 109% is certainly a sight to behold.

trinity industries在过去三年中每股收益大幅增长。以至于这三年增长率并不是对该公司未来的公平评估。因此,最好将我们的分析重点放在过去一年的增长率上。令人印象深刻的是,trinity industries的每股收益从1.10美元飙升至2.30美元。年增长率达到109%,确实令人瞩目。

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Trinity Industries shareholders can take confidence from the fact that EBIT margins are up from 9.6% to 14%, and revenue is growing. Both of which are great metrics to check off for potential growth.

确认公司增长的一种方法是查看其营业收入和利息、税前利润(EBIT)利润率的变化。trinity industries的股东可以放心,因为EBIT利润率从9.6%上升至14%,且营业收入增长。这两点都是用于检验潜在增长的重要指标。

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

在下面的图表中,您可以看到公司的盈利和营业收入随时间的增长情况。要查看实际数字,请单击图表。

While profitability drives the upside, prudent investors always check the balance sheet, too.

尽管利润带来上行动能,但审慎投资者也应检查资产负债表。

Are Trinity Industries Insiders Aligned With All Shareholders?

trinity industries的内部人员是否与所有股东保持一致?

It's a necessity that company leaders act in the best interest of shareholders and so insider investment always comes as a reassurance to the market. So it is good to see that Trinity Industries insiders have a significant amount of capital invested in the stock. Indeed, they hold US$40m worth of its stock. This considerable investment should help drive long-term value in the business. Even though that's only about 1.5% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

公司领导人以股东的最大利益行事是必要的,因此内部人员的投资总是对市场来说一种安心。所以看到trinity industries的内部人员投资了大量资金进入股票是件好事。实际上,他们持有价值4000万美元的股票。这种可观的投资应该有助于推动业务的长期价值。尽管这只占公司的约1.5%,但足以表明公司领导人与普通股东之间的一致性。

It's good to see that insiders are invested in the company, but are remuneration levels reasonable? Well, based on the CEO pay, you'd argue that they are indeed. For companies with market capitalisations between US$2.0b and US$6.4b, like Trinity Industries, the median CEO pay is around US$6.7m.

看到内部人员投资公司是件好事,但薪酬水平合理吗?基于CEO的薪酬,可以说确实合理。对于像trinity industries这样市值在20亿美元至64亿美元之间的公司,CEO的中位数薪酬大约是670万美元左右。

Trinity Industries' CEO took home a total compensation package worth US$5.7m in the year leading up to December 2023. That seems pretty reasonable, especially given it's below the median for similar sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

在2023年12月前一年,trinity industries的CEO获得了价值570万美元的总薪酬包。这看起来相当合理,尤其是考虑到它低于类似规模公司的中位数。CEO薪酬水平并不是投资者最关注的重要指标,但当薪酬适度时,这确实支持CEO与普通股东之间的增强一致性。通常情况下,合理的薪酬水平证明了良好的决策能力。

Is Trinity Industries Worth Keeping An Eye On?

值得密切关注的trinity industries吗?

Trinity Industries' earnings per share have been soaring, with growth rates sky high. An added bonus for those interested is that management hold a heap of stock and the CEO pay is quite reasonable, illustrating good cash management. The strong EPS improvement suggests the businesses is humming along. Trinity Industries is certainly doing some things right and is well worth investigating. Before you take the next step you should know about the 3 warning signs for Trinity Industries (1 is a bit unpleasant!) that we have uncovered.

trinity industries的每股收益正在飙升,增长速度飞快。 对那些感兴趣的人来说,额外的好处是管理层持有大量股票,CEO的薪酬相当合理,表明了良好的现金管理。 强劲的每股收益改善表明业务正在蓬勃发展。 trinity industries肯定做对了一些事情,值得深入调查。 在您迈出下一步之前,您应该了解一下我们发现的trinity industries的3个警告信号(其中有一个有点令人不愉快!)。

Although Trinity Industries certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with more skin in the game, then check out this handpicked selection of companies that not only boast of strong growth but have strong insider backing.

尽管trinity industries看起来确实不错,但如果内部人士在购买股票,可能会吸引更多投资者的兴趣。 如果您喜欢看到公司参与更多的游戏,那么请查看这些经过精心挑选的公司,它们不仅拥有强劲的增长,而且有强大的内部支持。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

请注意,本文讨论的内部交易是指在相关司法管辖区中报告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有任何反馈?对内容有任何疑虑?请直接与我们联系。或者,发送电子邮件至editorial-team@simplywallst.com。

这篇文章是Simply Wall St的一般性文章。我们根据历史数据和分析师预测提供评论,只使用公正的方法论,我们的文章并不意味着提供任何金融建议。文章不构成买卖任何股票的建议,也不考虑您的目标或您的财务状况。我们的目标是带给您基本数据驱动的长期关注分析。请注意,我们的分析可能不考虑最新的价格敏感公司公告或定性材料。Simply Wall St没有任何股票头寸。

译文内容由第三方软件翻译。