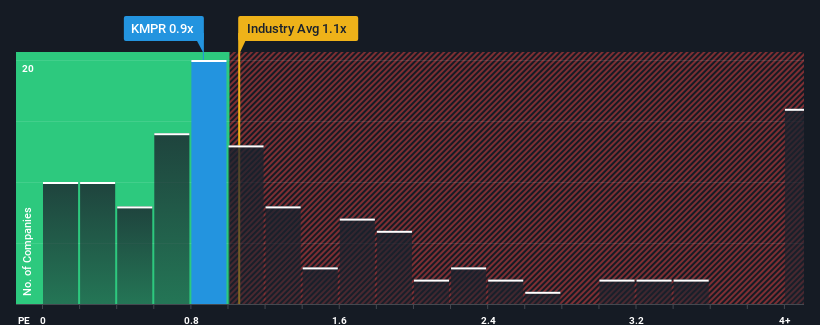

With a median price-to-sales (or "P/S") ratio of close to 1.1x in the Insurance industry in the United States, you could be forgiven for feeling indifferent about Kemper Corporation's (NYSE:KMPR) P/S ratio of 0.9x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

NYSE:KMPR Price to Sales Ratio vs Industry November 4th 2024

What Does Kemper's P/S Mean For Shareholders?

Kemper could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is moderate because investors think this poor revenue performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Keen to find out how analysts think Kemper's future stacks up against the industry? In that case, our free report is a great place to start.

How Is Kemper's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Kemper's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 9.6%. The last three years don't look nice either as the company has shrunk revenue by 19% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 3.5% as estimated by the five analysts watching the company. With the industry predicted to deliver 4.1% growth , the company is positioned for a comparable revenue result.

With this in mind, it makes sense that Kemper's P/S is closely matching its industry peers. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

A Kemper's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Insurance industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Kemper (1 doesn't sit too well with us) you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 9.6%. The last three years don't look nice either as the company has shrunk revenue by 19% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 9.6%. The last three years don't look nice either as the company has shrunk revenue by 19% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

在审查过去一年的财务数据时,我们看到公司的营业收入下降了9.6%。过去三年的情况也不容乐观,公司总体上减少了19%的营业收入。因此,股东们对中期营收增长率感到沮丧。

在审查过去一年的财务数据时,我们看到公司的营业收入下降了9.6%。过去三年的情况也不容乐观,公司总体上减少了19%的营业收入。因此,股东们对中期营收增长率感到沮丧。