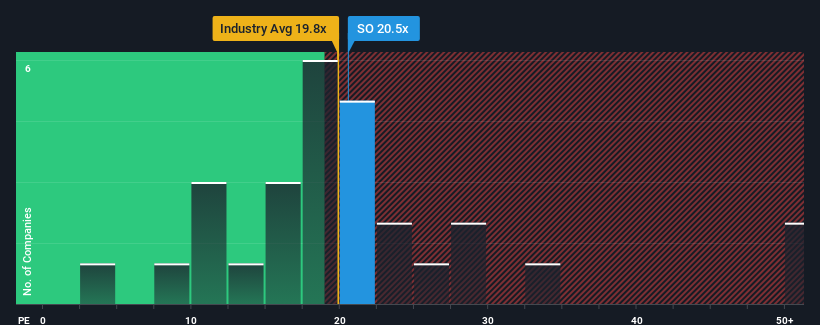

With a price-to-earnings (or "P/E") ratio of 20.5x The Southern Company (NYSE:SO) may be sending bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 10x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Southern has been doing quite well of late. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. If not, then existing shareholders might be a little nervous about the viability of the share price.

NYSE:SO Price to Earnings Ratio vs Industry November 3rd 2024 Want the full picture on analyst estimates for the company? Then our free report on Southern will help you uncover what's on the horizon.

Is There Enough Growth For Southern?

In order to justify its P/E ratio, Southern would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 55% last year. The strong recent performance means it was also able to grow EPS by 52% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 3.3% each year during the coming three years according to the analysts following the company. Meanwhile, the rest of the market is forecast to expand by 11% each year, which is noticeably more attractive.

With this information, we find it concerning that Southern is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From Southern's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Southern currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You need to take note of risks, for example - Southern has 3 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company grew earnings per share by an impressive 55% last year. The strong recent performance means it was also able to grow EPS by 52% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Taking a look back first, we see that the company grew earnings per share by an impressive 55% last year. The strong recent performance means it was also able to grow EPS by 52% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

首先回顧一下,我們發現該公司去年每股收益增長了驚人的55%。近期強勁的表現意味着在過去三年中總體上也能夠將每股收益增加了52%。因此,股東們可能對這些中期的盈利增長率感到滿意。

首先回顧一下,我們發現該公司去年每股收益增長了驚人的55%。近期強勁的表現意味着在過去三年中總體上也能夠將每股收益增加了52%。因此,股東們可能對這些中期的盈利增長率感到滿意。