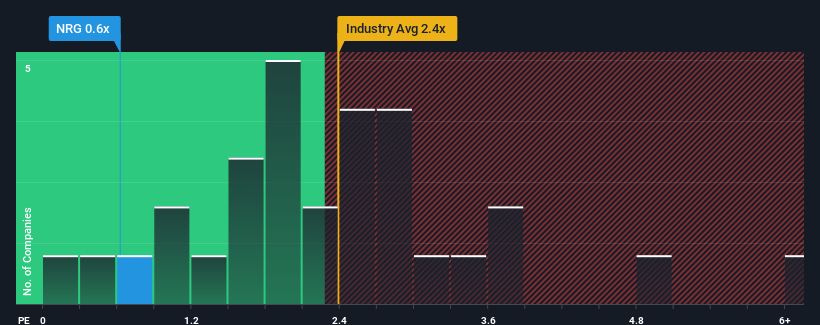

When close to half the companies operating in the Electric Utilities industry in the United States have price-to-sales ratios (or "P/S") above 2.4x, you may consider NRG Energy, Inc. (NYSE:NRG) as an attractive investment with its 0.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

NYSE:NRG Price to Sales Ratio vs Industry November 3rd 2024

What Does NRG Energy's Recent Performance Look Like?

NRG Energy has been struggling lately as its revenue has declined faster than most other companies. Perhaps the market isn't expecting future revenue performance to improve, which has kept the P/S suppressed. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. Or at the very least, you'd be hoping the revenue slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Keen to find out how analysts think NRG Energy's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

There's an inherent assumption that a company should underperform the industry for P/S ratios like NRG Energy's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 5.2%. Even so, admirably revenue has lifted 59% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the five analysts covering the company suggest revenue should grow by 4.0% each year over the next three years. With the industry predicted to deliver 4.9% growth per year, the company is positioned for a comparable revenue result.

In light of this, it's peculiar that NRG Energy's P/S sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

What We Can Learn From NRG Energy's P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of NRG Energy's revealed that its P/S remains low despite analyst forecasts of revenue growth matching the wider industry. Despite average revenue growth estimates, there could be some unobserved threats keeping the P/S low. It appears some are indeed anticipating revenue instability, because these conditions should normally provide more support to the share price.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for NRG Energy (2 make us uncomfortable) you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 5.2%. Even so, admirably revenue has lifted 59% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 5.2%. Even so, admirably revenue has lifted 59% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

首先回顧一下,該公司去年的營業收入增長並不令人興奮,因爲它錄得了令人失望的下降5.2%。即便如此,令人欽佩的是,儘管過去12個月有些波折,但總體來看,營業收入比三年前增長了59%。因此,我們可以開始確認該公司在那段時間內通常做得非常好,儘管在發展過程中曾遇到一些波折。

首先回顧一下,該公司去年的營業收入增長並不令人興奮,因爲它錄得了令人失望的下降5.2%。即便如此,令人欽佩的是,儘管過去12個月有些波折,但總體來看,營業收入比三年前增長了59%。因此,我們可以開始確認該公司在那段時間內通常做得非常好,儘管在發展過程中曾遇到一些波折。