Biodesix, Inc. (NASDAQ:BDSX) shares have had a horrible month, losing 26% after a relatively good period beforehand. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 19% share price drop.

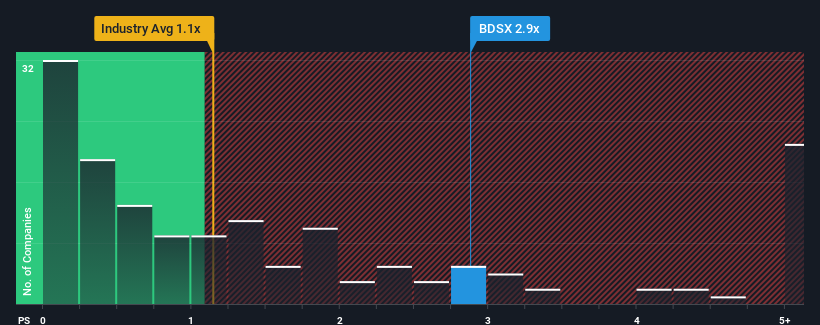

In spite of the heavy fall in price, you could still be forgiven for thinking Biodesix is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.9x, considering almost half the companies in the United States' Healthcare industry have P/S ratios below 1.1x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

NasdaqGM:BDSX Price to Sales Ratio vs Industry November 2nd 2024

What Does Biodesix's Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, Biodesix has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Biodesix will help you uncover what's on the horizon.

What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Biodesix's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 49% gain to the company's top line. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 12% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Turning to the outlook, the next three years should generate growth of 24% per year as estimated by the five analysts watching the company. That's shaping up to be materially higher than the 7.4% each year growth forecast for the broader industry.

With this information, we can see why Biodesix is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Biodesix's P/S?

Despite the recent share price weakness, Biodesix's P/S remains higher than most other companies in the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look into Biodesix shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Biodesix (1 is significant) you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should outperform the industry for P/S ratios like Biodesix's to be considered reasonable.

There's an inherent assumption that a company should outperform the industry for P/S ratios like Biodesix's to be considered reasonable.

公司應該表現優於行業,納斯達克比奧德塞克斯的市銷率才能被認爲是合理的。

公司應該表現優於行業,納斯達克比奧德塞克斯的市銷率才能被認爲是合理的。