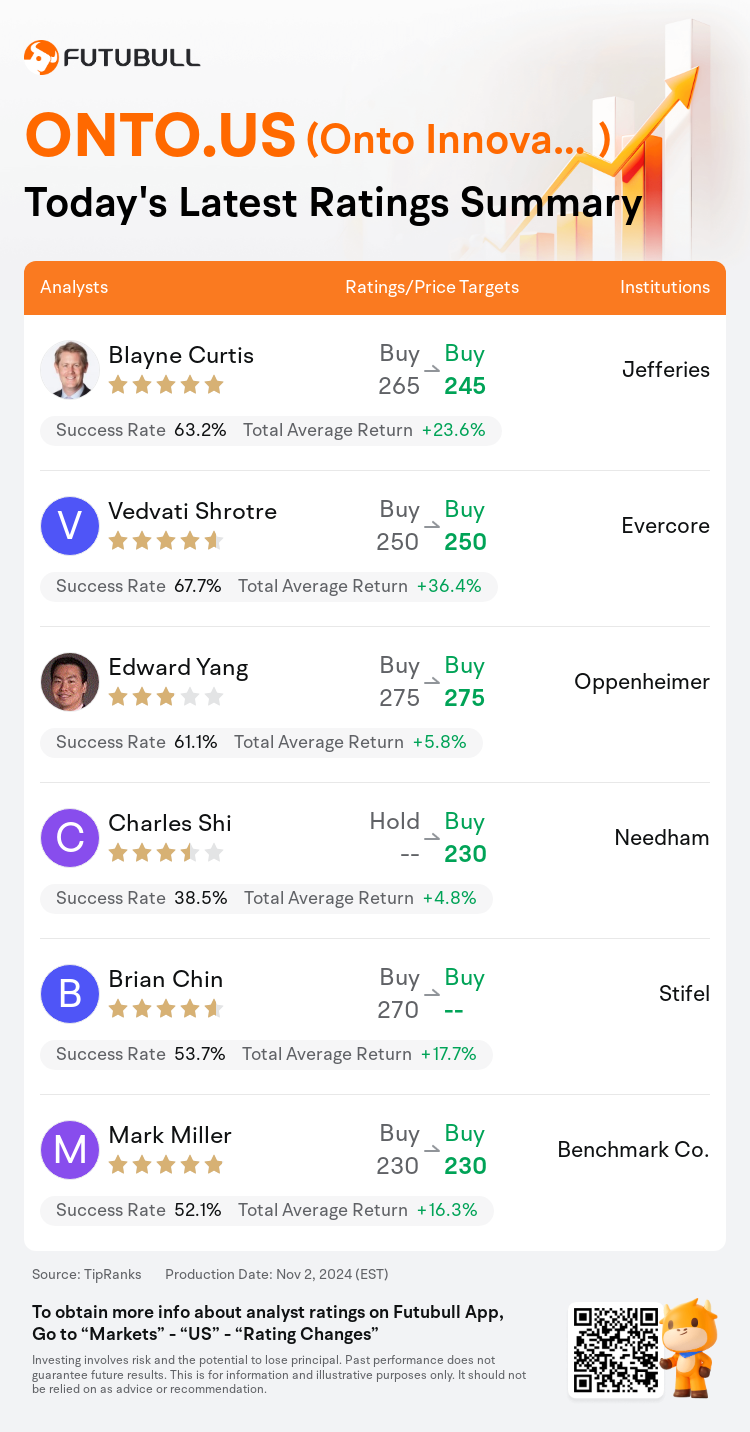

On Nov 02, major Wall Street analysts update their ratings for $Onto Innovation (ONTO.US)$, with price targets ranging from $230 to $275.

Jefferies analyst Blayne Curtis maintains with a buy rating, and adjusts the target price from $265 to $245.

Evercore analyst Vedvati Shrotre maintains with a buy rating, and maintains the target price at $250.

Oppenheimer analyst Edward Yang maintains with a buy rating, and maintains the target price at $275.

Oppenheimer analyst Edward Yang maintains with a buy rating, and maintains the target price at $275.

Needham analyst Charles Shi upgrades to a buy rating, and sets the target price at $230.

Stifel analyst Brian Chin maintains with a buy rating.

Furthermore, according to the comprehensive report, the opinions of $Onto Innovation (ONTO.US)$'s main analysts recently are as follows:

The ongoing hiatus in HBM persists, yet the fortification provided by the robustness in advanced DRAM and Power Semiconductors assists in counterbalancing the ongoing postponement. It is posited that a resurgence to vigorous growth is likely to be merely a question of time.

Onto Innovation's Q3 revenue growth matched expectations, fueled by robust demand for Dragonfly, a resurgence in Advanced Nodes, and unprecedented power semiconductor performance. This was balanced by a $10M deferral in orders for JetStep Lithography. Despite increasing visibility in CoWos, Onto is cautiously not incorporating comparable incremental high bandwidth memory revenue, according to the analyst.

Onto Innovation's Q3 results modestly exceeded expectations, and the quarter might have shown a more significant outperformance if it were not for a shortfall in lithography shipments, as mentioned by an analyst. Looking ahead to 2025, the company's management expresses the greatest optimism for DRAM, with advanced logic and AI packaging also being areas of positive expectations.

Here are the latest investment ratings and price targets for $Onto Innovation (ONTO.US)$ from 6 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

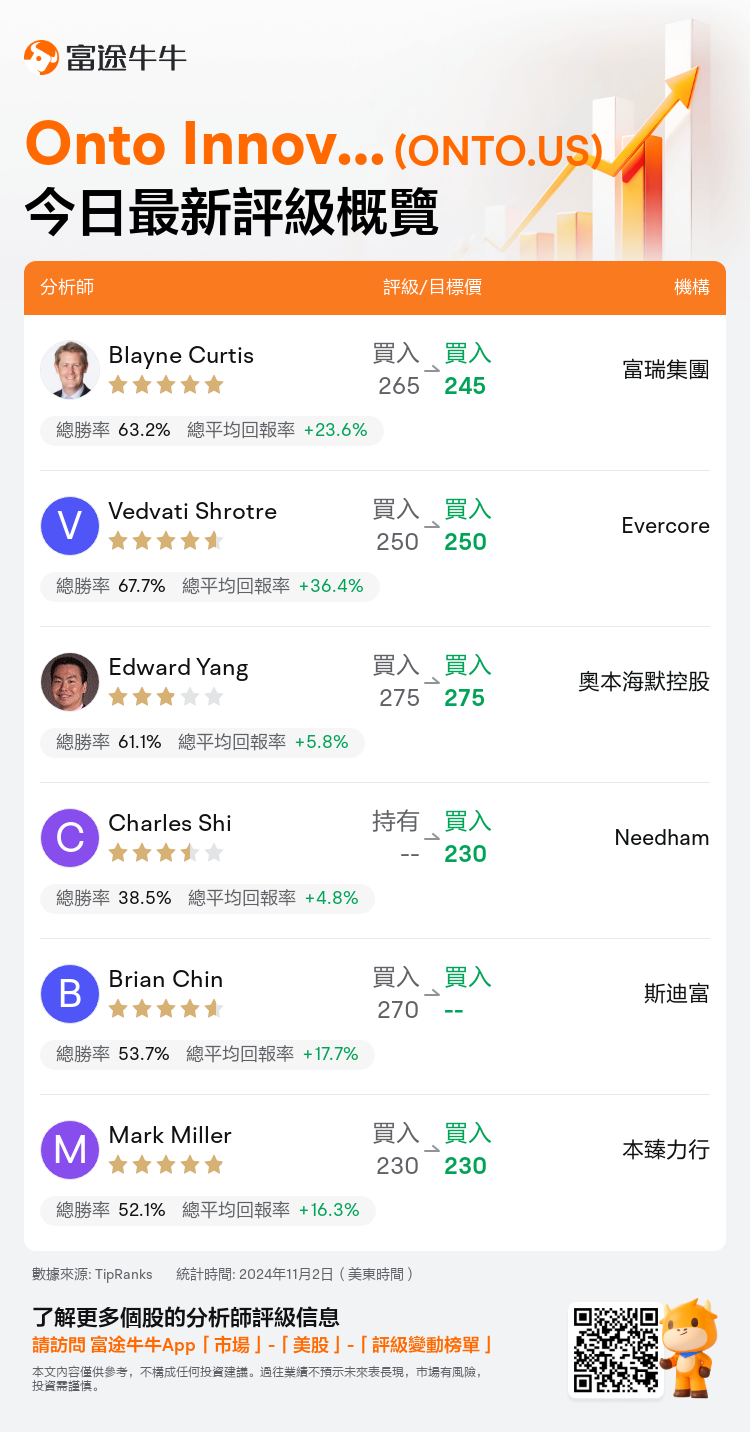

美東時間11月2日,多家華爾街大行更新了$Onto Innovation (ONTO.US)$的評級,目標價介於230美元至275美元。

富瑞集團分析師Blayne Curtis維持買入評級,並將目標價從265美元下調至245美元。

Evercore分析師Vedvati Shrotre維持買入評級,維持目標價250美元。

奧本海默控股分析師Edward Yang維持買入評級,維持目標價275美元。

奧本海默控股分析師Edward Yang維持買入評級,維持目標價275美元。

Needham分析師Charles Shi上調至買入評級,目標價230美元。

斯迪富分析師Brian Chin維持買入評級。

此外,綜合報道,$Onto Innovation (ONTO.US)$近期主要分析師觀點如下:

在半導體半導體的持續停頓下,先進的DRAM和功率半導體的穩固性提供對抗持續推遲的支撐。有人認爲,重新回到強勁增長很可能只是時間問題。

Onto Innovation的Q3營業收入增長符合預期,得益於對Dragonfly的強勁需求,先進節點的復甦以及前所未有的功率半導體性能。這被JetStep光刻機訂單推遲1000萬美元所抵消。儘管CoWo的透明度增加,但根據分析師的說法,Onto謹慎地沒有納入相當數量的高帶寬存儲器營業收入。

Onto Innovation的Q3業績略微超過預期,如果不是由一位分析師提出的光刻機出貨量不足,本季度可能會表現更好。展望2025年,該公司管理層表示最爲樂觀的是DRAM,而先進邏輯和人工智能封裝也是正面預期領域。

以下爲今日6位分析師對$Onto Innovation (ONTO.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。