Return Trends At Alamo Group (NYSE:ALG) Aren't Appealing

Return Trends At Alamo Group (NYSE:ALG) Aren't Appealing

0.14 = US$175m ÷ (US$1.5b - US$212m)

0.14 = US$175m ÷ (US$1.5b - US$212m) What trends should we look for it we want to identify stocks that can multiply in value over the long term? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. That's why when we briefly looked at Alamo Group's (NYSE:ALG) ROCE trend, we were pretty happy with what we saw.

如果我們想要找出在長期內能夠增值的股票,我們應該關注什麼趨勢?除其他因素外,我們希望看到兩點;首先,資本運作回報率(ROCE)不斷增長,其次,公司資本運作金額擴大。如果你看到這一點,通常意味着這是一家業務模式優秀並具有豐富盈利再投資機會的公司。這就是爲什麼當我們簡要查看阿拉莫集團(紐交所:ALG)的ROCE趨勢時,我們對所看到的感到非常滿意。

What Is Return On Capital Employed (ROCE)?

我們對 Enphase Energy 的資本僱用回報率的看法:正如我們上面看到的,Enphase Energy 的資本回報率沒有提高,但它正在重新投資於業務。投資者必須認爲未來會有更好的前景,因爲股票表現良好,使持股五年以上的股東獲得了 690% 的收益。最終,如果基本趨勢持續存在,我們不會對它成爲一隻多頭股持有期很久很有信心。

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Alamo Group:

只是爲了澄清,如果您不確定,ROCE是用來評估公司在其業務中投資資本所獲得的稅前收入比率的指標。分析師使用這個公式計算阿拉莫集團的ROCE:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

資產僱用回報率(ROCE)是指企業利潤,即企業稅前利潤除以企業投入的總資本(負債加股權)。如果ROCE高於企業財務成本的承受能力,那麼企業就會創造出更多的價值。

0.14 = US$175m ÷ (US$1.5b - US$212m) (Based on the trailing twelve months to September 2024).

0.14 = 17500萬美元 ÷ (15億美元 - 2.12億美元)(基於截至2024年9月的過去十二個月)。

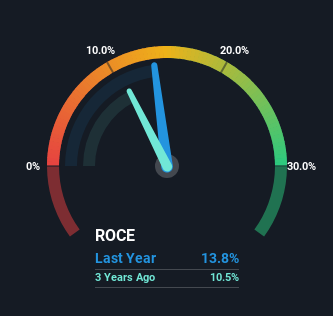

So, Alamo Group has an ROCE of 14%. That's a relatively normal return on capital, and it's around the 13% generated by the Machinery industry.

因此,阿拉莫集團的ROCE爲14%。這是一個相對正常的資本回報率,大約是機械行業產生的13%。

Above you can see how the current ROCE for Alamo Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Alamo Group for free.

上面您可以看到阿拉莫集團當前的ROCE與之前的資本回報率相比,但過去能告訴您的並不多。如果您願意,可以免費查看覆蓋阿拉莫集團的分析師的預測。

How Are Returns Trending?

綜合上述,Cimpress非常有效地提高了其資本利用率所產生的回報。考慮到股票過去五年保持穩定,如果其他指標也不錯,則可能存在機會。因此,進一步研究這家公司並確定這些趨勢是否會持續是合理的。

While the current returns on capital are decent, they haven't changed much. The company has employed 72% more capital in the last five years, and the returns on that capital have remained stable at 14%. 14% is a pretty standard return, and it provides some comfort knowing that Alamo Group has consistently earned this amount. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

雖然目前的資本回報率還不錯,但變化不大。公司在過去五年中投入的資本增加了72%,而該資本的回報率仍穩定在14%。14%是一個相當標準的回報率,知道阿拉莫集團一直能穩定獲得這個金額,會讓人感到一些安慰。長時間內,這樣的回報可能不會特別激動人心,但是具備連續性後,可能會在股價回報方面產生回報。

In Conclusion...

最後,同等資本下回報率較低的趨勢通常不是我們關注創業板股票的最佳信號。由於這些發展進行良好,因此投資者不太可能表現友好。自五年前以來,該股下跌了32%。除非這些指標朝着更積極的軌跡轉變,否則我們將繼續尋找其他股票。

The main thing to remember is that Alamo Group has proven its ability to continually reinvest at respectable rates of return. And the stock has followed suit returning a meaningful 79% to shareholders over the last five years. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

最重要的是記住,阿拉莫集團已經證明了其能夠持續以可觀的回報率再投資。而股票也隨之而來,在過去五年中對股東回報了有意義的79%。因此,即使股票可能比以前更加"昂貴",但我們認爲強勁的基本面支持進一步研究這隻股票。

While Alamo Group doesn't shine too bright in this respect, it's still worth seeing if the company is trading at attractive prices. You can find that out with our FREE intrinsic value estimation for ALG on our platform.

雖然在這方面阿拉莫集團表現得不是太亮眼,但仍值得看看公司是否以有吸引力的價格交易。您可以在我們的平台上免費查看ALG的內在價值估算。

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Hao Tian International Construction Investment Group確實存在一些風險,我們已經發現了一條警示標誌,你可能會感興趣。對於那些喜歡投資於實力雄厚的公司的人,可以查看這個由財務狀況強大、股本回報率高的公司組成的免費列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。