Earnings Report: Zwsoft Co.,Ltd. Missed Revenue Estimates By 7.1%

Earnings Report: Zwsoft Co.,Ltd. Missed Revenue Estimates By 7.1%

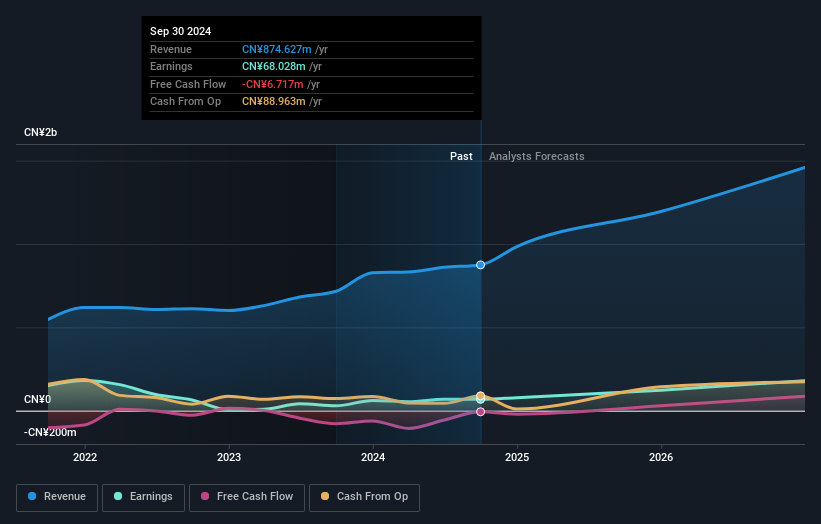

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that ZwsoftLtd's rate of growth is expected to accelerate meaningfully, with the forecast 28% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 17% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 19% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect ZwsoftLtd to grow faster than the wider industry.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that ZwsoftLtd's rate of growth is expected to accelerate meaningfully, with the forecast 28% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 17% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 19% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect ZwsoftLtd to grow faster than the wider industry. It's been a good week for Zwsoft Co.,Ltd. (SHSE:688083) shareholders, because the company has just released its latest quarterly results, and the shares gained 2.0% to CN¥93.50. Results look mixed - while revenue fell marginally short of analyst estimates at CN¥204m, statutory earnings were in line with expectations, at CN¥0.51 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

对于中望软件股份有限公司(SHSE:688083)的股东来说,本周过得不错,因为公司刚刚发布了最新的季度业绩,股票涨幅为2.0%,报收人民币93.50元。 业绩看起来褒贬不一-营业收入略低于分析师预期的人民币20400万,但法定盈利与预期一致,为每股人民币0.51元。 分析师通常会在每份盈利报告后更新他们的预测,我们可以从他们的估计中判断他们对公司的看法是否有改变,或者是否有任何需要注意的新问题。考虑到这一点,我们已经搜集了最新的法定预测,以了解分析师对明年的预期。

Taking into account the latest results, the most recent consensus for ZwsoftLtd from 15 analysts is for revenues of CN¥1.19b in 2025. If met, it would imply a sizeable 37% increase on its revenue over the past 12 months. Before this earnings report, the analysts had been forecasting revenues of CN¥1.20b and earnings per share (EPS) of CN¥0.98 in 2025. So we can see that while the consensus made no real change to its revenue estimates, it also no longer provides an earnings per share estimate. This suggests that revenues are what the market is focusing on after the latest results.

考虑到最新的结果,来自15名分析师的最新一致意见是中望软件在2025年的营业收入将达到人民币11.9亿。 如果达到,将意味着其过去12个月的营业收入将大幅增长37%。 在本次盈利报告之前,分析师预测2025年的营业收入为12亿元,每股盈利(EPS)为0.98元。 因此,我们可以看到,虽然一致意见对其营业收入预估没有真正变化,但也不再提供每股盈利预估。这表明市场在关注最新业绩后更注重营业收入。

The average price target rose 8.9% to CN¥84.40, with the analysts clearly having become more optimistic about ZwsoftLtd'sprospects following these results. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on ZwsoftLtd, with the most bullish analyst valuing it at CN¥127 and the most bearish at CN¥55.00 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

平均目标价上涨8.9%,至人民币84.40元,分析师在这些结果发布后明显对中望软件的前景更加乐观。 此外,查看分析师预测的区间也很有启发性,以评估离群意见与平均值有多大差异。 对于中望软件,分析师对其存在一些不同的看法,最看好的分析师将其价值定为人民币127元,而最看淡的为55.00元。 注意分析师目标价格的巨大差距?这对我们意味着公司的基础业务可能存在相当广泛的可能性场景。

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that ZwsoftLtd's rate of growth is expected to accelerate meaningfully, with the forecast 28% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 17% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 19% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect ZwsoftLtd to grow faster than the wider industry.

现在放眼更宏观的视角,我们理解这些预测的一种方法是将其与过去业绩和行业增长预估进行比较。 从最新预测中可以明显看出,中望软件的增长速度预计会明显加快,预计到2025年底,每年增长28%的营业收入增长速度明显快于过去五年17%的历史增长率。 相比之下,我们的数据表明,同一行业(有分析师覆盖)的其他公司预计每年营业收入增长19%。 看来,尽管增长前景比最近更为乐观,但分析师也预期中望软件的增长速度将快于整个行业。

The Bottom Line

最重要的事情是分析师增加了它对下一年每股亏损的估计。令人欣慰的是,营收预测未发生重大变化,业务仍有望比整个行业增长更快。共识价格目标稳定在28.50美元,最新估计不足以对价格目标产生影响。

The clear take away from these updates is that the analysts made no change to their revenue estimates for next year, with the business apparently performing in line with their models. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

从这些更新中可以清楚地看出,分析师对明年的营业收入预估没有进行任何更改,业务显然与他们的模型表现一致。令人高兴的是,营收预测没有发生重大变化,业务仍预计增长速度将快于整个行业。我们注意到价格目标的升级,暗示分析师认为业务的内在价值可能会随时间改喀速的。

We have estimates for ZwsoftLtd from its 15 analysts out to 2026, and you can see them free on our platform here.

我们有截至2026年15位分析师对中望软件的估算,您可以在我们的平台上免费查看。

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for ZwsoftLtd that you should be aware of.

不要忘记可能仍然存在风险。例如,我们已经确定好了中望软件存在2个警示信号,您应该注意。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对本文有任何反馈?对内容有任何疑虑?请直接与我们联系。或者,发送电子邮件至editorial-team@simplywallst.com。

这篇文章是Simply Wall St的一般性文章。我们根据历史数据和分析师预测提供评论,只使用公正的方法论,我们的文章并不意味着提供任何金融建议。文章不构成买卖任何股票的建议,也不考虑您的目标或您的财务状况。我们的目标是带给您基本数据驱动的长期关注分析。请注意,我们的分析可能不考虑最新的价格敏感公司公告或定性材料。Simply Wall St没有任何股票头寸。

译文内容由第三方软件翻译。