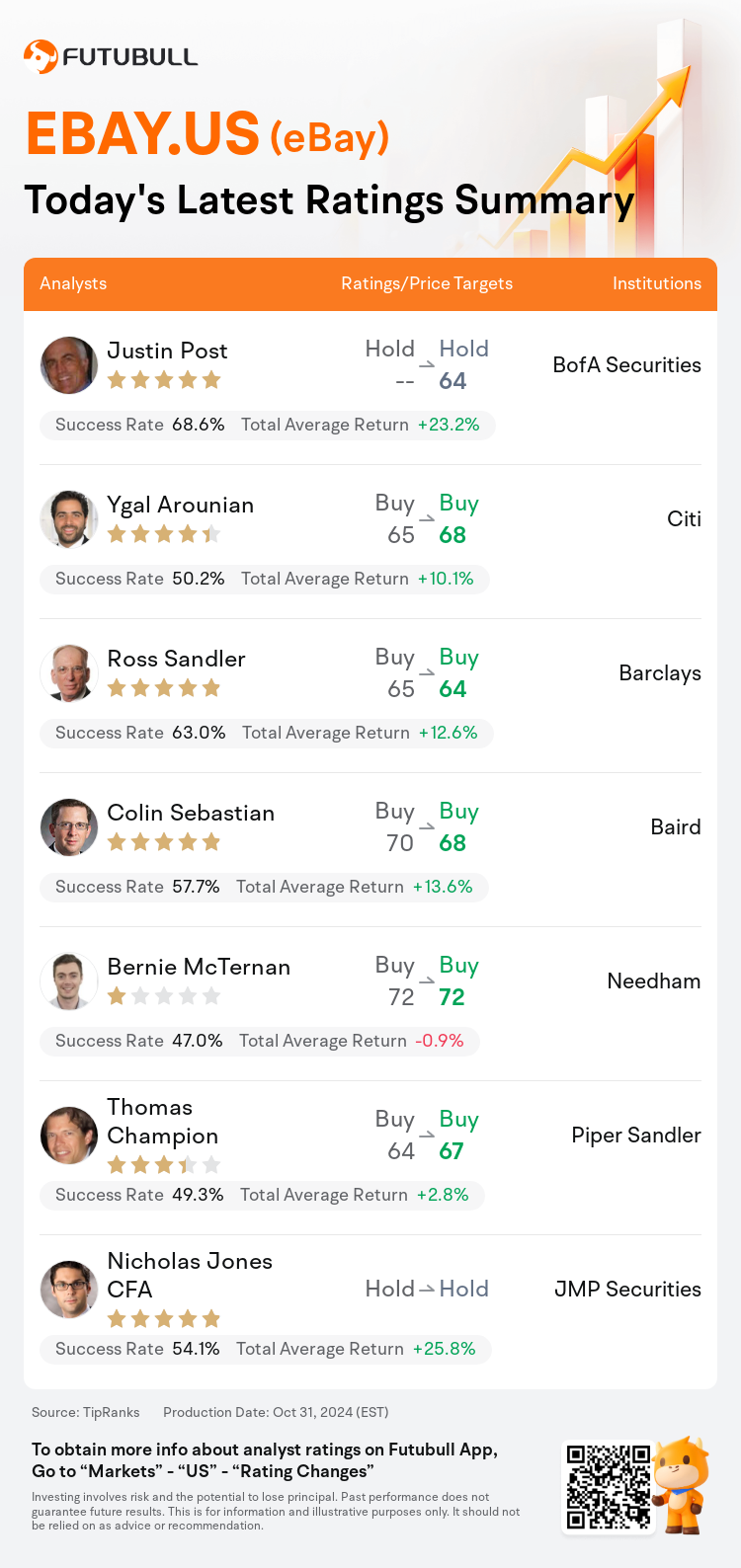

On Oct 31, major Wall Street analysts update their ratings for $eBay (EBAY.US)$, with price targets ranging from $64 to $72.

BofA Securities analyst Justin Post maintains with a hold rating, and sets the target price at $64.

Citi analyst Ygal Arounian maintains with a buy rating, and adjusts the target price from $65 to $68.

Barclays analyst Ross Sandler maintains with a buy rating, and adjusts the target price from $65 to $64.

Barclays analyst Ross Sandler maintains with a buy rating, and adjusts the target price from $65 to $64.

Baird analyst Colin Sebastian maintains with a buy rating, and adjusts the target price from $70 to $68.

Needham analyst Bernie McTernan maintains with a buy rating, and maintains the target price at $72.

Furthermore, according to the comprehensive report, the opinions of $eBay (EBAY.US)$'s main analysts recently are as follows:

After examining eBay's Q3 results, which were largely consistent with expectations, it's anticipated that the Q4 Gross Merchandise Volume will align with current market projections.

eBay's third-quarter results surpassed expectations, although the guidance for the fourth quarter presented a mixed outlook, largely due to a strategic investment in the UK. The focus on consumer-to-consumer commerce is expected to temporarily affect revenue and take rate, yet it is anticipated to stabilize by early 2025, and could ultimately contribute positively to gross merchandise volume and revenue.

Subsequent to the quarterly report and subsequent guidance, projections for Q4 and 2025 Gross Merchandise Volume (GMV) have been modestly increased. However, there has been a slight reduction in the revenue and non-GAAP EPS estimates, now set at $10.6 billion and $5.21, down from previous estimates of $10.7 billion and $5.28, respectively. This adjustment is due to potential headwinds in monetization, as noted by the analyst.

The company's reported revenue and earnings aligned closely with expectations, yet the guidance for Q4 fell short of the consensus. Despite this, the perception of the company's value proposition remains consistent, with its shares appearing attractively priced. Furthermore, share buybacks are anticipated to offer investors a degree of protection against this transitory setback.

It is anticipated that the shares will experience a decrease in value as a result of the fourth-quarter revenue guidance. This expectation is based on the transition to a 'no-fee' model for consumer-to-consumer transactions in the UK, as well as concerns related to the U.S. election and a reduced timeframe for shopping.

Here are the latest investment ratings and price targets for $eBay (EBAY.US)$ from 7 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

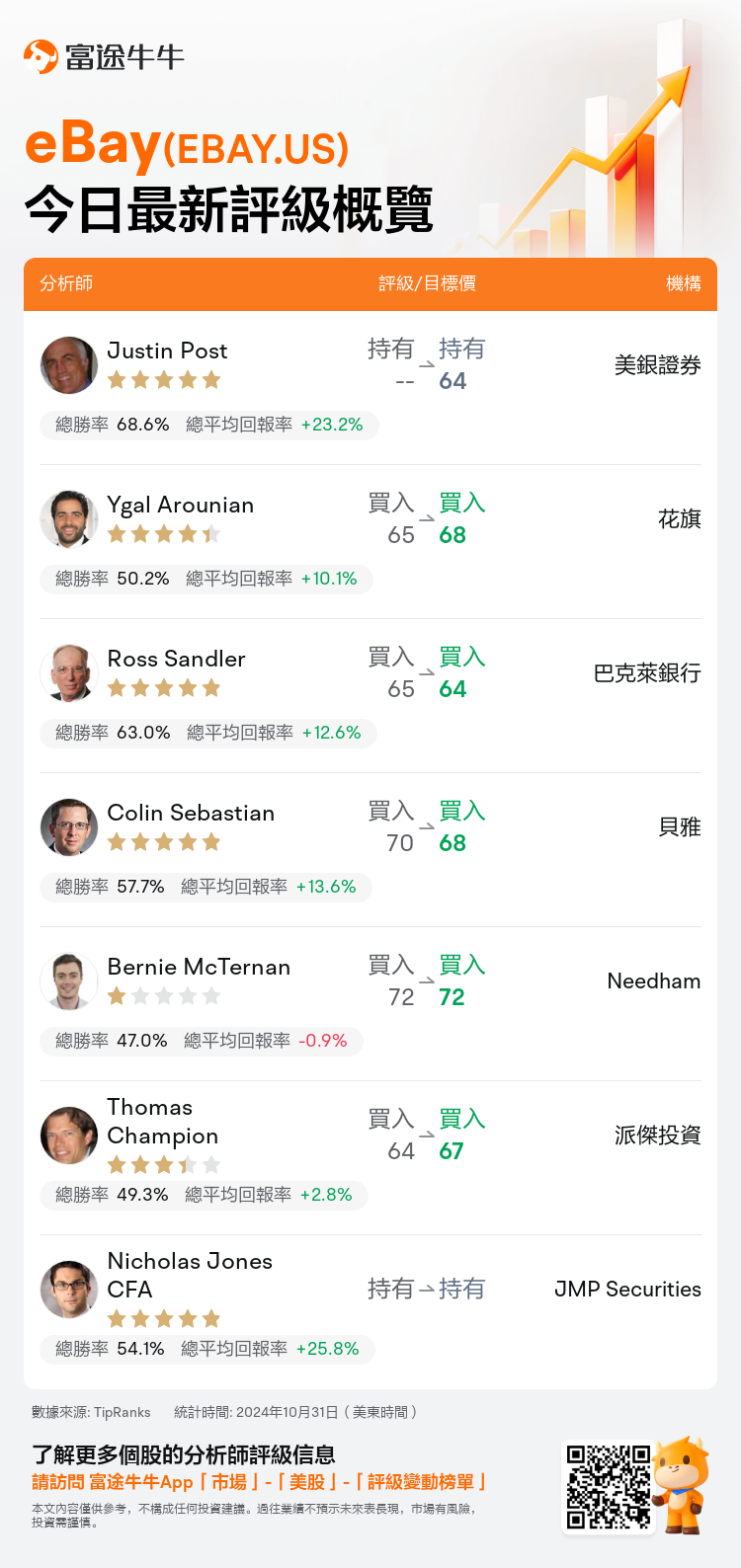

美東時間10月31日,多家華爾街大行更新了$eBay (EBAY.US)$的評級,目標價介於64美元至72美元。

美銀證券分析師Justin Post維持持有評級,目標價64美元。

花旗分析師Ygal Arounian維持買入評級,並將目標價從65美元上調至68美元。

巴克萊銀行分析師Ross Sandler維持買入評級,並將目標價從65美元下調至64美元。

巴克萊銀行分析師Ross Sandler維持買入評級,並將目標價從65美元下調至64美元。

貝雅分析師Colin Sebastian維持買入評級,並將目標價從70美元下調至68美元。

Needham分析師Bernie McTernan維持買入評級,維持目標價72美元。

此外,綜合報道,$eBay (EBAY.US)$近期主要分析師觀點如下:

經過對ebay第三季度業績的檢查,結果基本符合預期,預計第四季度的總成交量將與當前市場預期一致。

ebay第三季度業績超出預期,儘管第四季度的指引呈現出複合的前景,主要是由於在英國的戰略投資。重點放在消費者對消費者的商業交易上,預計會暫時影響營業收入和成交量,但預計到2025年初會穩定下來,最終有望對總成交量和營業收入產生積極影響。

在季度報告和後續指引公佈後,預計第四季度和2025年總成交量(GMV)的預測略有增加。然而,營業收入和非GAAP每股收益的估算略有下降,目前分別設定爲106億美元和5.21美元,低於之前的107億美元和5.28美元的估算。這一調整是由於分析師指出的變現可能面臨的阻力。

該公司報告的營業收入和盈利與預期基本一致,但第四季度的指引低於共識。儘管如此,對公司價值主張的看法保持一致,其股價似乎具有吸引力。此外,股票回購有望爲投資者提供一定程度的保護,以對抗這一暫時的挫折。

預計由於第四季度營業收入指引,股票將出現下跌。這一預期基於英國消費者到消費者交易轉向「無費用」模式,以及與美國選舉有關的擔憂和購物時間縮短。

以下爲今日7位分析師對$eBay (EBAY.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。