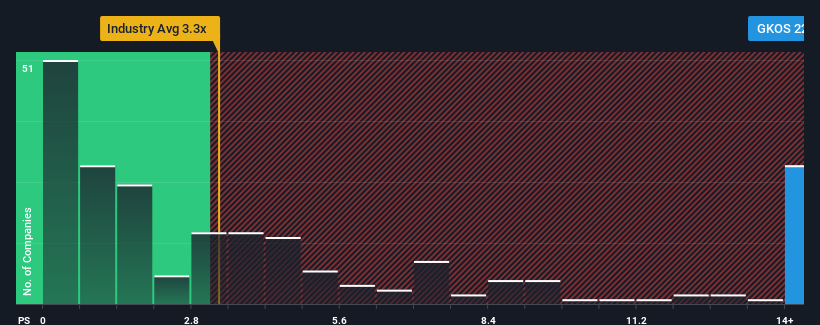

With a price-to-sales (or "P/S") ratio of 22.1x Glaukos Corporation (NYSE:GKOS) may be sending very bearish signals at the moment, given that almost half of all the Medical Equipment companies in the United States have P/S ratios under 3.4x and even P/S lower than 1.2x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

NYSE:GKOS Price to Sales Ratio vs Industry October 30th 2024

What Does Glaukos' Recent Performance Look Like?

Recent times have been advantageous for Glaukos as its revenues have been rising faster than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Glaukos.

Is There Enough Revenue Growth Forecasted For Glaukos?

The only time you'd be truly comfortable seeing a P/S as steep as Glaukos' is when the company's growth is on track to outshine the industry decidedly.

If we review the last year of revenue growth, the company posted a terrific increase of 15%. Revenue has also lifted 20% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Turning to the outlook, the next three years should generate growth of 24% per annum as estimated by the analysts watching the company. With the industry only predicted to deliver 9.3% per year, the company is positioned for a stronger revenue result.

With this information, we can see why Glaukos is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Glaukos' P/S?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Glaukos' analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Glaukos you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of revenue growth, the company posted a terrific increase of 15%. Revenue has also lifted 20% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

If we review the last year of revenue growth, the company posted a terrific increase of 15%. Revenue has also lifted 20% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

回顧過去一年的營業收入增長,該公司實現了驚人的15%增長。三年前的總營收也增長了20%,主要得益於過去12個月的增長。因此,可以說最近公司的營收增長是可觀的。

回顧過去一年的營業收入增長,該公司實現了驚人的15%增長。三年前的總營收也增長了20%,主要得益於過去12個月的增長。因此,可以說最近公司的營收增長是可觀的。