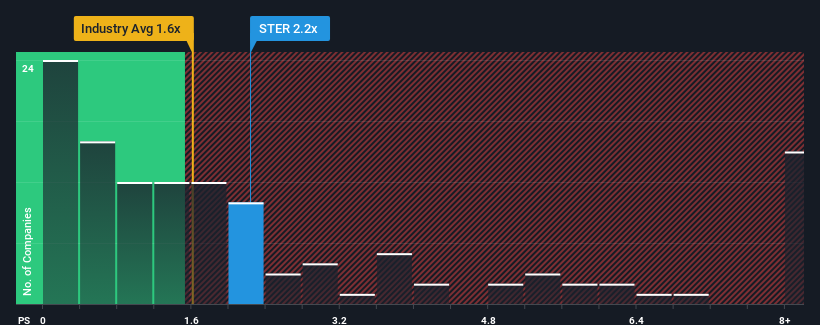

When close to half the companies in the Professional Services industry in the United States have price-to-sales ratios (or "P/S") below 1.6x, you may consider Sterling Check Corp. (NASDAQ:STER) as a stock to potentially avoid with its 2.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

NasdaqGS:STER Price to Sales Ratio vs Industry October 30th 2024

How Has Sterling Check Performed Recently?

While the industry has experienced revenue growth lately, Sterling Check's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to recover substantially, which has kept the P/S from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Sterling Check's future stacks up against the industry? In that case, our free report is a great place to start.

Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Sterling Check would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Although pleasingly revenue has lifted 35% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, shareholders will be pleased, but also have some questions to ponder about the last 12 months.

Turning to the outlook, the next year should generate growth of 7.9% as estimated by the nine analysts watching the company. With the industry predicted to deliver 6.6% growth , the company is positioned for a comparable revenue result.

With this in consideration, we find it intriguing that Sterling Check's P/S is higher than its industry peers. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/S falls to levels more in line with the growth outlook.

The Bottom Line On Sterling Check's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Analysts are forecasting Sterling Check's revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. The fact that the revenue figures aren't setting the world alight has us doubtful that the company's elevated P/S can be sustainable for the long term. A positive change is needed in order to justify the current price-to-sales ratio.

You should always think about risks. Case in point, we've spotted 1 warning sign for Sterling Check you should be aware of.

If you're unsure about the strength of Sterling Check's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Although pleasingly revenue has lifted 35% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, shareholders will be pleased, but also have some questions to ponder about the last 12 months.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Although pleasingly revenue has lifted 35% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, shareholders will be pleased, but also have some questions to ponder about the last 12 months.

首先回顧一下,我們發現公司過去一年基本沒有營業收入增長。儘管令人高興的是,總體上營業收入比三年前增長了35%,儘管過去12個月的收入。因此,股東們會感到高興,但也會對過去12個月有一些疑問需要考慮。

首先回顧一下,我們發現公司過去一年基本沒有營業收入增長。儘管令人高興的是,總體上營業收入比三年前增長了35%,儘管過去12個月的收入。因此,股東們會感到高興,但也會對過去12個月有一些疑問需要考慮。