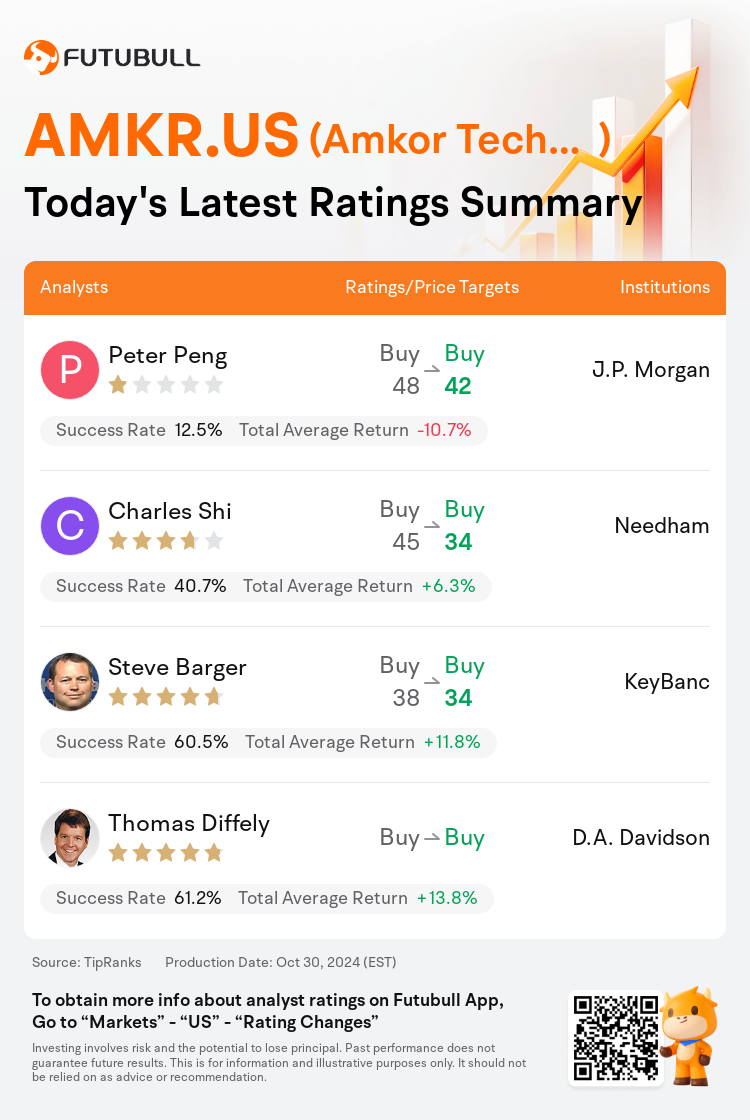

On Oct 30, major Wall Street analysts update their ratings for $Amkor Technology (AMKR.US)$, with price targets ranging from $34 to $42.

J.P. Morgan analyst Peter Peng maintains with a buy rating, and adjusts the target price from $48 to $42.

Needham analyst Charles Shi maintains with a buy rating, and adjusts the target price from $45 to $34.

KeyBanc analyst Steve Barger maintains with a buy rating, and adjusts the target price from $38 to $34.

KeyBanc analyst Steve Barger maintains with a buy rating, and adjusts the target price from $38 to $34.

D.A. Davidson analyst Thomas Diffely maintains with a buy rating.

Furthermore, according to the comprehensive report, the opinions of $Amkor Technology (AMKR.US)$'s main analysts recently are as follows:

Initially adopting a cautious stance, it became evident that Amkor Technology's guidance for the December quarter fell short of both the analyst's and broader market projections. This shortfall was attributed to factors such as seasonality, accounting for the majority, and device transition, cited as a partial cause. Concerns were raised about a potential reduction in market share with one of its key clients. Subsequent to these revelations, projections were significantly lowered.

Amkor Technology reported marginally improved results for the September quarter, driven by an uptick in seasonal smartphone demand and sustained momentum in artificial intelligence packaging. However, this was set against a backdrop of subdued demand in the automotive and industrial sectors. Expectations for the forward estimates have been moderated, with a more favorable outlook anticipated for 2025.

Amkor Technology's third-quarter results were strong, yet the forecast for the fourth quarter was significantly reduced, suggesting an estimated 11% quarter-over-quarter decrease in overall revenue and a 23% quarter-over-quarter reduction in Communications revenue. This decline is considerably steeper than the single-digit drops typically observed in the fourth quarter. The primary cause of the weaker outlook for Amkor is believed to be a decrease in demand for high-end smartphones and an under-allocation of orders for 2024 models. Nevertheless, it is anticipated that the strength in Computing revenue will persist into the fourth quarter.

Amkor Technology reported a modest underperformance in Q3 earnings but provided guidance for Q4 that was significantly lower than expected, leading to a notable decline in share price after hours. This subdued outlook is mainly attributed to reduced activity in the Communications end market, with Amkor pointing out an atypical smartphone production schedule.

Here are the latest investment ratings and price targets for $Amkor Technology (AMKR.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

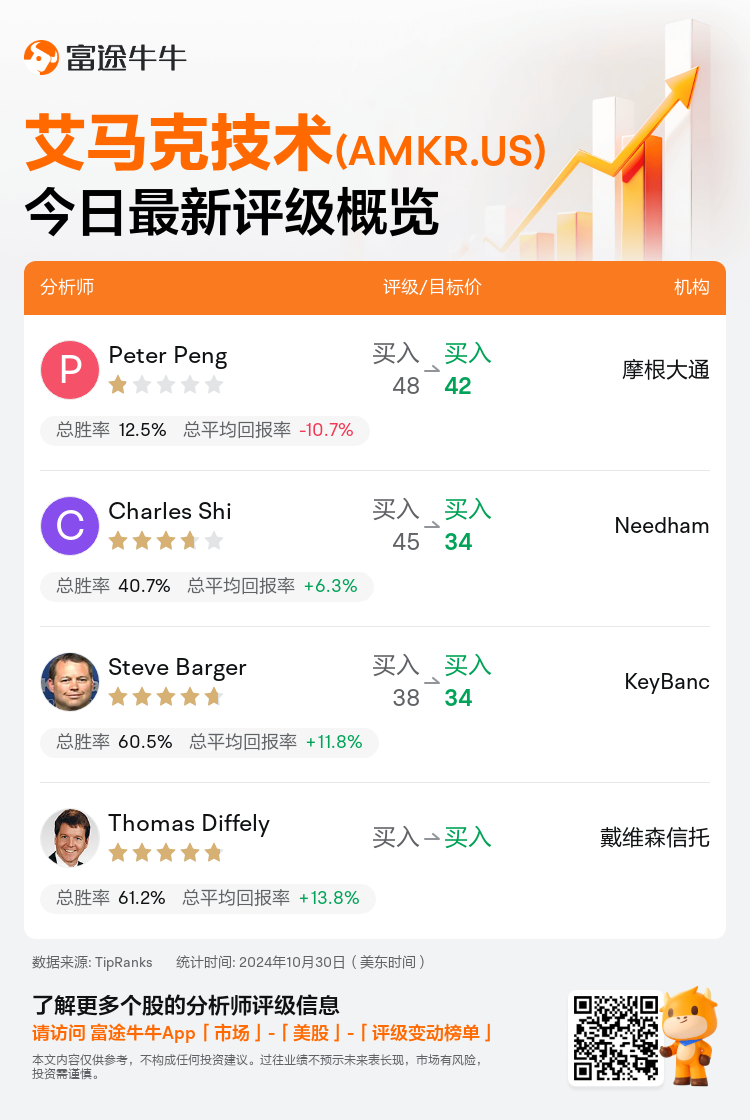

美东时间10月30日,多家华尔街大行更新了$艾马克技术 (AMKR.US)$的评级,目标价介于34美元至42美元。

摩根大通分析师Peter Peng维持买入评级,并将目标价从48美元下调至42美元。

Needham分析师Charles Shi维持买入评级,并将目标价从45美元下调至34美元。

KeyBanc分析师Steve Barger维持买入评级,并将目标价从38美元下调至34美元。

KeyBanc分析师Steve Barger维持买入评级,并将目标价从38美元下调至34美元。

戴维森信托分析师Thomas Diffely维持买入评级。

此外,综合报道,$艾马克技术 (AMKR.US)$近期主要分析师观点如下:

最初采取谨慎立场后,显而易见,艾马克技术对12月季度的指引不仅落后于分析师和更广泛市场的预期。这一不足被归因于诸如季节性等因素,其中以会计为主,并举部分过渡设备为部分原因。有关可能减少与其关键客户之一的市场份额的担忧也随之而来。在这些揭示之后,预测被明显降低。

艾马克技术报告显示,由于季节性智能手机需求增长和人工智能封装领域的持续推动,2021年9月季度结果略有改善。然而,这与汽车和工业领域需求不振的背景形成鲜明对比。对未来预期已有所调整,预计2025年展望更为乐观。

艾马克技术第三季度业绩强劲,但第四季度的预测大幅下调,预示着整体营业收入环比下降11%,通信-半导体营收环比减少23%。这种下降比第四季度通常观察到的个位数降幅更为显著。艾马克的业绩预期更弱的主要原因被认为是高端智能手机需求下降以及对2024年机型订单的分配不足。然而,预计计算业务收入的强劲增长将持续到第四季度。

艾马克技术报告显示,第三季度收益略显不足,但对第四季度的指引大幅低于预期,导致盘后股价显著下降。这种疲软的前景主要归因于通信-半导体终端市场活动减少,艾马克指出了手机生产计划的异常性。

以下为今日4位分析师对$艾马克技术 (AMKR.US)$的最新投资评级及目标价:

提示:

TipRanks为独立第三方,提供金融分析师的分析数据,并计算分析师推荐的平均回报率和胜率。提供的信息并非投资建议,仅供参考。本文不对评级数据和报告的完整性与准确性做出认可、声明或保证。

TipRanks提供每位分析师的星级,分析师星级代表分析师所有推荐的过往表现,通过分析师的总胜率和平均回报率综合计算得出,星星越多,则该分析师过往表现越优异,最高为5颗星。

分析师总胜率为近一年分析师的评级成功次数占总评级次数的比率。评级的成功与否,取决于TipRanks的虚拟投资组合是否从该股票中产生正回报。

总平均回报率为基于分析师的初始评级创建虚拟投资组合,并根据评级变化对组合进行调整,在近一年中该投资组合所获得的回报率。