Loss-Making DraftKings Inc. (NASDAQ:DKNG) Expected To Breakeven In The Medium-Term

Loss-Making DraftKings Inc. (NASDAQ:DKNG) Expected To Breakeven In The Medium-Term

One thing we would like to bring into light with DraftKings is its relatively high level of debt. Generally, the rule of thumb is debt shouldn't exceed 40% of your equity, which in DraftKings' case is 97%. Note that a higher debt obligation increases the risk in investing in the loss-making company.

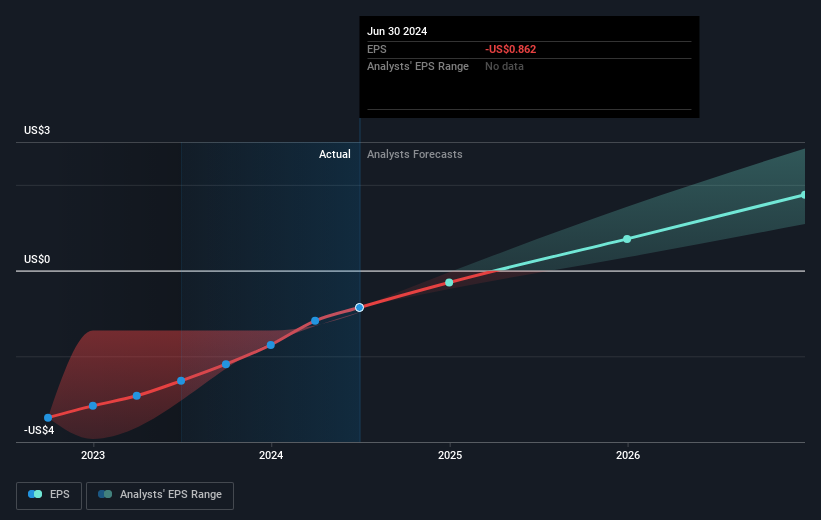

One thing we would like to bring into light with DraftKings is its relatively high level of debt. Generally, the rule of thumb is debt shouldn't exceed 40% of your equity, which in DraftKings' case is 97%. Note that a higher debt obligation increases the risk in investing in the loss-making company. With the business potentially at an important milestone, we thought we'd take a closer look at DraftKings Inc.'s (NASDAQ:DKNG) future prospects. DraftKings Inc. operates as a digital sports entertainment and gaming company in the United States and internationally. The US$18b market-cap company posted a loss in its most recent financial year of US$802m and a latest trailing-twelve-month loss of US$406m shrinking the gap between loss and breakeven. The most pressing concern for investors is DraftKings' path to profitability – when will it breakeven? Below we will provide a high-level summary of the industry analysts' expectations for the company.

考慮到公司有可能迎來重要的里程碑,我們認爲值得更近一步地了解納斯達克(draftkings)公司(NASDAQ:DKNG)未來的前景。納斯達克(draftkings)公司是一家在美國和國際上經營數字體育娛樂和arvr遊戲業務的公司,市值爲180億美元。該公司在最近一個財政年度虧損了80200萬美元,在最近12個月的最新虧損爲40600萬美元,縮小了虧損與盈虧平衡之間的差距。投資者最着急的問題是納斯達克(draftkings)公司實現盈利的路徑——它何時會盈虧平衡?接下來,我們將簡要概述分析師對該公司的預期。

Consensus from 34 of the American Hospitality analysts is that DraftKings is on the verge of breakeven. They expect the company to post a final loss in 2024, before turning a profit of US$369m in 2025. So, the company is predicted to breakeven just over a year from today. In order to meet this breakeven date, we calculated the rate at which the company must grow year-on-year. It turns out an average annual growth rate of 62% is expected, which signals high confidence from analysts. Should the business grow at a slower rate, it will become profitable at a later date than expected.

34位美國酒店行業分析師的共識是,納斯達克(draftkings)正處在盈虧平衡的邊緣。他們預計該公司將在2024年實現最終虧損,然後在2025年實現3,6900萬美元的利潤。因此,預測該公司將在今後一年多的時間內實現盈虧平衡。爲了達到這一盈虧平衡日期,我們計算了該公司必須實現年增長率。結果表明,分析師對其有很高的信心,預計其年平均增長率爲62%。如果業務增長速度較慢,它將在預期之後的日期實現盈利。

Underlying developments driving DraftKings' growth isn't the focus of this broad overview, but, bear in mind that typically a high forecast growth rate is not unusual for a company that is currently undergoing an investment period.

推動納斯達克(draftkings)增長的基本發展並不是這份廣泛概述的重點,但請注意,對於目前處於投資期的公司,高預測增長率並不飛凡。

One thing we would like to bring into light with DraftKings is its relatively high level of debt. Generally, the rule of thumb is debt shouldn't exceed 40% of your equity, which in DraftKings' case is 97%. Note that a higher debt obligation increases the risk in investing in the loss-making company.

我們想要提醒關注的一點是,納斯達克(draftkings)相對較高的債務水平。一般來說,準則是債務不應超過您的股本的40%,而納斯達克(draftkings)的情況是97%。請注意,更高的債務義務將增加投資這家虧損公司的風險。

Next Steps:

下一步:

This article is not intended to be a comprehensive analysis on DraftKings, so if you are interested in understanding the company at a deeper level, take a look at DraftKings' company page on Simply Wall St. We've also put together a list of pertinent aspects you should further research:

本文不旨在對納斯達克(draftkings)進行全面分析,所以如果您有興趣深入了解該公司,請查看Simply Wall St上納斯達克(draftkings)公司頁面。我們還列出了一些您應該進一步研究的相關方面。

- Valuation: What is DraftKings worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether DraftKings is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on DraftKings's board and the CEO's background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

- 估值: DraftKings今天價值多少?未來增長潛力已經反映在股價中了嗎?我們免費研究報告中的內在價值信息圖表可以幫助您直觀地看出DraftKings目前是否被市場定價錯誤。

- 管理團隊: 一支經驗豐富的管理團隊掌舵增加了我們對業務的信心 - 看看誰在DraftKings的董事會和CEO的背景。

- 其他高表現的股票:是否有其他表現更好的股票並具有經過驗證的歷史記錄?查看這裏的免費列表。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。