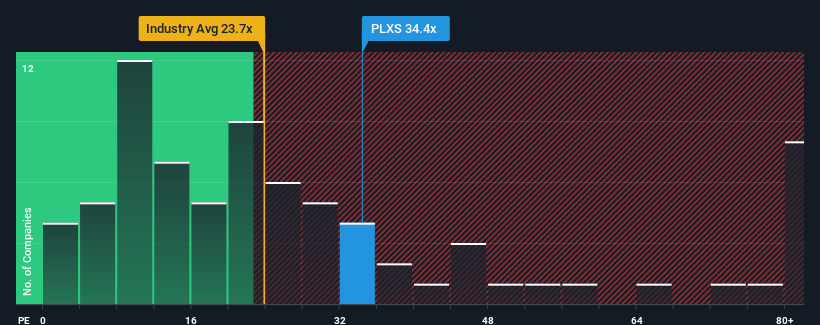

With a price-to-earnings (or "P/E") ratio of 34.4x Plexus Corp. (NASDAQ:PLXS) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 17x and even P/E's lower than 10x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings that are retreating more than the market's of late, Plexus has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

NasdaqGS:PLXS Price to Earnings Ratio vs Industry October 28th 2024 Want the full picture on analyst estimates for the company? Then our free report on Plexus will help you uncover what's on the horizon.

How Is Plexus' Growth Trending?

In order to justify its P/E ratio, Plexus would need to produce outstanding growth well in excess of the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, earnings from three years ago have also fallen 16% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 50% as estimated by the six analysts watching the company. With the market only predicted to deliver 15%, the company is positioned for a stronger earnings result.

With this information, we can see why Plexus is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Plexus' P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Plexus' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Plexus you should know about.

If you're unsure about the strength of Plexus' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, earnings from three years ago have also fallen 16% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. As a result, earnings from three years ago have also fallen 16% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

首先回顧一下,去年公司的每股收益增長並不令人興奮,因爲它出現了令人失望的下降19%。因此,三年前的收益總體也下降了16%。很遺憾,我們不得不承認公司在這段時間內並未在增長收益方面做得很好。

首先回顧一下,去年公司的每股收益增長並不令人興奮,因爲它出現了令人失望的下降19%。因此,三年前的收益總體也下降了16%。很遺憾,我們不得不承認公司在這段時間內並未在增長收益方面做得很好。